Nominally Hedged: You Down With PBC?

Compression, Corporate Structure and The Difficulty of Being a CEO

Compression Earnings and the Leverage Paradox

Q1 2025: When OFS Margin Expansion Meets Contracting Opportunity

Being a CEO is hard. And, as it turns out, fewer and fewer people want the job.

One reason? You’re always selling—especially in public markets.

The modern CEO is part operator, part spokesperson, and mostly a professional capital allocator with a quarterly speaking role. Earnings calls have become roadshows in miniature: thirty minutes to persuade the Street that your stock is different. Better. Buyable.

You drop a few phrases analysts want to hear—“capital discipline,” “FCF generation,” “balanced approach to shareholder returns.” You thank Keith for his softball question. You move on.

In oil & gas, this ritual is especially stylized. Whether you’re running an E&P, a midstream player, or an OFS shop, you’re not selling a growth story. You’re selling a product: income—dividends, buybacks, low leverage ratios, yield stability in an unstable world.

But not all CEOs are playing on the same difficulty setting.

If you’re in oilfield services, the job is harder. You deploy capital up front. Your customers cut budgets by Tuesday. Revenue is booked on spot. Term is rare. And there’s no hedge for what you’re selling.

So you build a narrative.

You name-drop Exxon. You emphasize Permian exposure. You talk about utilization. Because you’re not just selling horsepower—you’re selling credibility. And it works—until the same pitch you use to reassure investors becomes a roadmap for your customers to reprice you.

In short: you’re selling your stock to Wall Street and handing your leverage to customers at the same time.

Compression: Infrastructure With a Lease

Nowhere is this more true than in compression.

Firms like KGS, USAC, and AROC sit in a rare middle ground: they look like infrastructure, act like services, and get priced like both.

Compression isn’t deferrable like frac. It’s required. You want to move gas? Drop pressure? Strip liquids? Run a cryo plant? You need compression. And as GORs rise, bottoms get deeper, and AI demand drives grid-scale power, the industry needs a lot more of it.

The units aren’t mobile assets. They’re 250,000-pound commitments that cost six figures to move. Stickiness is structural. That’s why term is standard: three-, five-, even seven-year contracts for high-horsepower units. You’re not just leasing capacity—you’re leasing optionality.

And that matters. Because in a development world that now looks more like manufacturing, optionality is no longer a luxury. It’s strategy.

Q1 Earnings: Strong Headlines, Fragile Foundations

On paper, Q1 2025 looked good. Utilization remained sky-high. Revenues were up. But dig into the filings, and it starts to look like a market on edge.

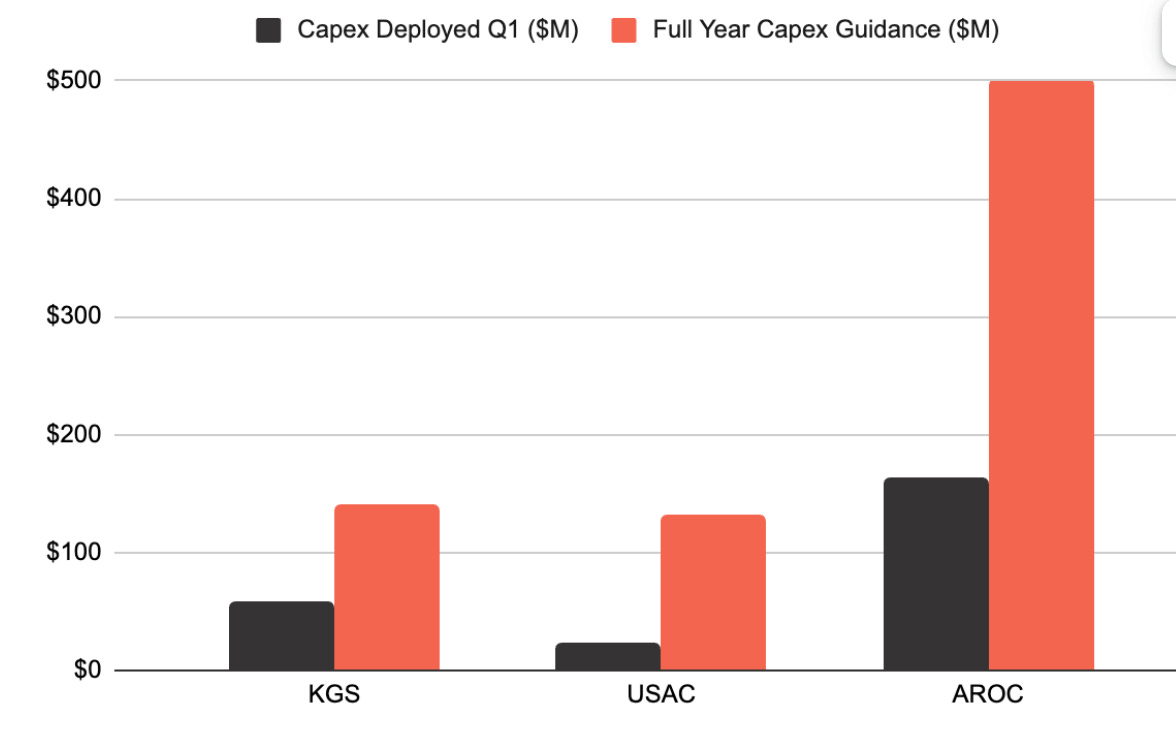

USAC deployed just 17% of its full-year capex in Q1.

KGS cut FY25 guidance by $10M.

AROC burned $87M in free cash integrating NGCSI.

Everyone’s sold out—but no one has the balance sheet to sell more.

The result? A supply squeeze in H2. And that makes now the leverage window.

Mixed Margins, Mixed Messages

USAC’s parts & services margins fell 26% quarter-over-quarter. KGS held steady—but only by halting growth. AROC posted clean earnings—but flagged integration risk.

Meanwhile, USAC’s topline was propped up by a 165% YoY jump in related-party revenue from Energy Transfer. That’s not operational strength—it’s balance sheet choreography.

If you’re an operator, this is your cue to:

Demand pass-through clauses

Unbundle aftermarket services

Tie escalation to real cost indices, not “market vibes”

They hedge their margins. You should hedge your contracts.

The Real Risk Is in H2

All three players are betting on H2 to deliver horsepower, revenue, and returns. But the margin for error is thin:

USAC EPS: –36% QoQ

AROC: FCF-negative

KGS: 3.7x net leverage

This isn’t the quarter to go long. It’s the quarter to build in accountability.

If their capital plan slips, it shouldn’t be your problem. Your contract should say so.

What E&Ps Should Do Next

1.Go Short Term

Think like an NFL GM.

If the vendor’s leverage is declining, don’t sign a five-year deal.

Twelve months. Reassess in Q2 2026. Simple.

2.Pick the Right Partner

Compression portfolios are often inherited through M&A. You end up with three vendors and keep mixing.

Instead, pick one or two:

KGS: Big horsepower, Permian

AROC: EDM, midstream

USAC: Gassy, mid-size, Northeast

Think in systems, not units. Align basin strategy with vendor capability.

3.Build a Credible Insourcing Option

Even if you never bring compression in-house, you should act like you might:

Run the ROI

Price the lease

Call the OEMs

Your vendor shouldn’t assume you’re captive.

They should believe you’ve got a Plan B.

What If an Oil Company Became a PBC?

Now, shift scenes.

Everyone’s talking about OpenAI this week—not because of ChatGPT, but because of governance. The nonprofit went for-profit. Then it went weird. Then it settled on a Public Benefit Corporation (PBC) structure.

Why? Because they wanted to raise capital without compromising mission.

So they wrote the mission into the charter.

And it worked.

Which brings us back to energy. BP tried the mission-first thing in 2020. Net-zero targets. Renewables push. “From IOC to IEC.” It didn’t land. By 2025, Elliott was calling for a full retreat.

But what if BP had locked in the mission structurally?

What if it had become a PBC?

Kickstarter did it. Patagonia did it. Veeva did it.

Even OpenAI, a for-profit built on GPU burn rates, did it.

Why couldn’t an oil company?

The Kalibr Oil Thought Experiment

Imagine: Tier 2 acreage. Non-core basin. Moderate returns.

But you incorporate as a PBC.

Your mission?

“To develop energy resources in support of national security and economic resilience.”

Now you’re still subject to capital discipline. But you have governance that allows you to:

Drill Tier 2 without quarterly panic

Justify development for strategic value

Fend off activists demanding pure-play margin

It’s not ESG window dressing.

It’s mission-backed structure.

Would it be for everyone? No.

Would it be for someone? Maybe.

Delaware vs. Texas: The Incorporation Arbitrage

Of course, this all assumes Delaware plays along.

Spoiler: they probably won’t.

Especially after voiding Elon’s $30B comp package and setting fire to the board’s discretion. The Tesla lawsuit created a new governance climate. One where “purpose over price” won’t fly easily—especially in oil.

Which brings us to Texas.

In May 2025, Governor Greg Abbott signed the Elon Musk Bill, making Texas the new frontier for corporate structure. Less litigation. More board freedom. And yes—PBC incorporation available.

Only one public E&P—Matador—is currently incorporated in Texas.

But with Comstock now dual-listed on the Dallas Stock Exchange, the playbook is emerging.

Texas is open for business.

And maybe—even for Public Benefit Oil.