Relativity, Leverage, Capture: The Three Laws That Turn Oil & Gas Market Intelligence into Outcomes

Nominally Hedged | September 2025: The Don Quixote Problem of Market Intelligence in Oil and Gas

Preface: What This Is (and Isn’t)

This is not our full market-intelligence product. It is a working example of how we build one: a data-driven practice that turns raw information into differentiation and then into money. To keep this illustrative, I am not naming live acquisition targets for Innovex. I will speak in general terms and use placeholders where appropriate. The method is the point.

The Don Quixote Problem of Market Intelligence

Some days, when I decode a Gen-Z phrase from our intern or drop a tight spiral to my seven-year-old QB, I feel young. Reality, like gravity, disagrees. Nothing proves it faster than sending your daughter into that purgatory between childhood and adolescence: fifth grade. In Colorado it comes with a book list. No problem for a bookworm. Stacking titles into the Amazon cart of the company that paid for Jeff Bezos’ wedding, I thought of the first book that hooked me: Don Quixote.

A country gentleman learns the code of chivalry and confuses it with the world. He studies, he prepares, he rides out, he attacks windmills. It is the most precise parable of brilliant vision that never connects with reality.

That is what passes for “market intelligence” in oil and gas. We subscribe to Enverus, Rystad, PowerAdvocate, and a dozen boutique feeds. We benchmark the same inputs, tear down the same cost curves, show the same slides to the same boards. On paper, rigor. In practice, cosplay. If everyone wears the same armor, no one is a knight.

Intelligence is not knowing what everyone knows. It is bending information until it accrues uniquely to you. Framing it, sequencing it, and wielding it in ways your competitors cannot. Otherwise it becomes trivia. Technically correct, strategically inert, economically irrelevant. That is the Don Quixote Problem: a field of windmills that look like giants because we all charged in the same direction.

The cure is not another dashboard. It is treating intelligence like negotiation: a process, not a file share. After a thousand deals on both sides of the table, we have learned that value comes from structure and sequence. It shows up when the other side is seated across from you.

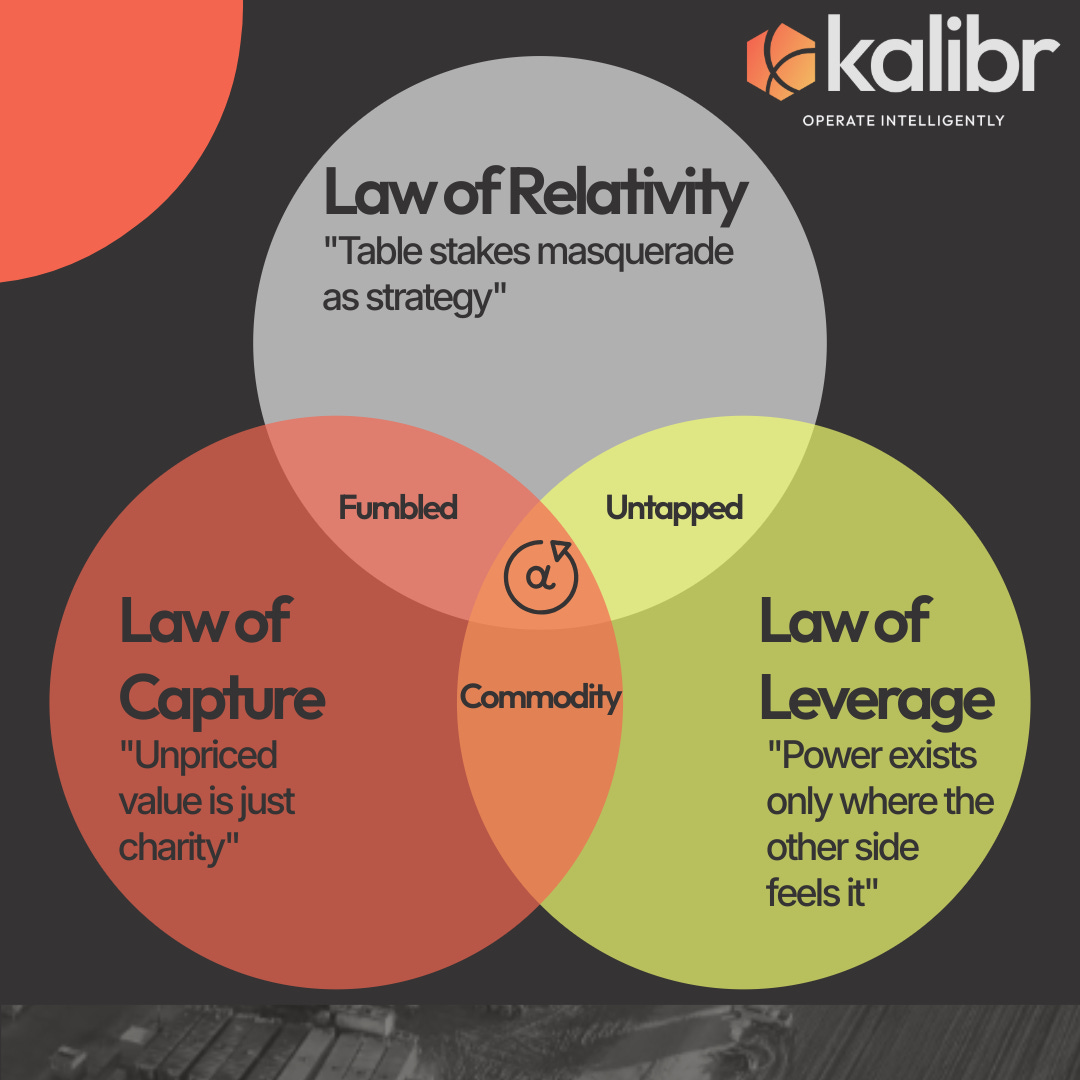

We run everything through three lenses:

Relativity: how you actually differ from peers.

Relevance: which differences your counterparty values.

Capture: how you translate that alignment into terms that lock in value.

Data becomes leverage, leverage becomes outcomes.

To make it concrete, we will use Innovex as a running case and talk about companies “X, Y, Z” rather than live names. The objective is to show the craft: how we quantify differentiation, map it to what the other side needs, and then encode it in a deal structure the market cannot easily copy.

The Law of Relativity: Differentiation That Survives the Side-by-Side

Question: Are you different, or just convinced?

We force “we’re differentiated” to show up in numbers. For Innovex, that means comparing its Citadel and DWS tuck-ins to truly comparable OFS roll-ups since 2019, then grading everyone on one yardstick.

Comparable set. High-margin consumables and rental tools in well construction and completions. “Big-impact, small-ticket” deals where synergy speed is decisive. Enough disclosure to score synergy, margin, ROIC/FCF, or culture execution. That yields PTEN↔NexTier/Ulterra, KLX↔QES, DTI bolt-ons, SLB↔ChampionX, among others. Right cohort for a consumables-led integration machine.

Timeline. Score the first 12–18 months post-close or the freshest quarter. Anchor on the first “clean” quarter where one-offs are disclosed so we are not grading accounting noise.

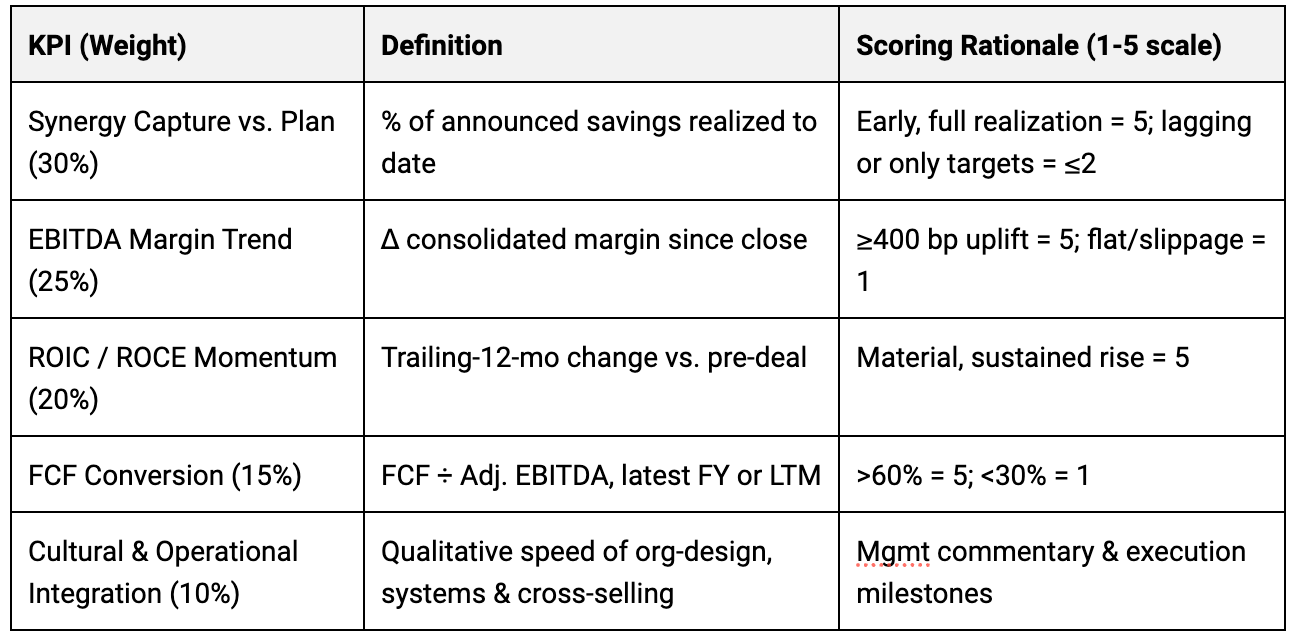

Five KPIs, one card.

Synergy capture vs plan (30%). Percent realized inside 12–18 months. Speed is the tell.

EBITDA margin delta (25%). Mix and operating leverage should show up quickly.

ROIC/ROCE momentum (20%). Direction vs an 8% WACC proxy.

FCF conversion (15%). FCF as a percent of adjusted EBITDA.

Culture/ops integration (10%). Retention, systems cut-over, early cross-sell.

Weights reflect where value actually comes from in consumables roll-ups. Speed and margin drive more than half the score. ROIC governs discipline. Cash confirms it is real. Culture is the canary without letting vibes run the math.

Rubric. A 1–5 scale with half-points:

Synergy: 5 at ≥100% in 12 months, 4 at ≥60% in 12 months or 100% by 18, 3 at 25–59% or target only with milestones, 2 below that, 1 if back-tracked.

Margin: 5 at ≥400 bp, 4 at 200–399, 3 at 50–199, 2 at 0–49, 1 negative.

ROIC: 5 clearly >10% and rising, 4 at 8–10% or a decisive uptrend, 3 at 6–7.9%, 2 below 6%, 1 destructive.

FCF: 5 above 60%, 4 at 45–60%, 3 at 30–44%, 2 at 15–29%, 1 below 15%.

Culture/ops: Green 4, Amber 3, Red 2.

We adjust margin and FCF for disclosed one-offs so we do not punish temporary tariff spikes or reward transitory mix shifts. If ROIC or FCF is not disclosed, we assign a neutral and document assumptions. Silence does not get you a trophy.

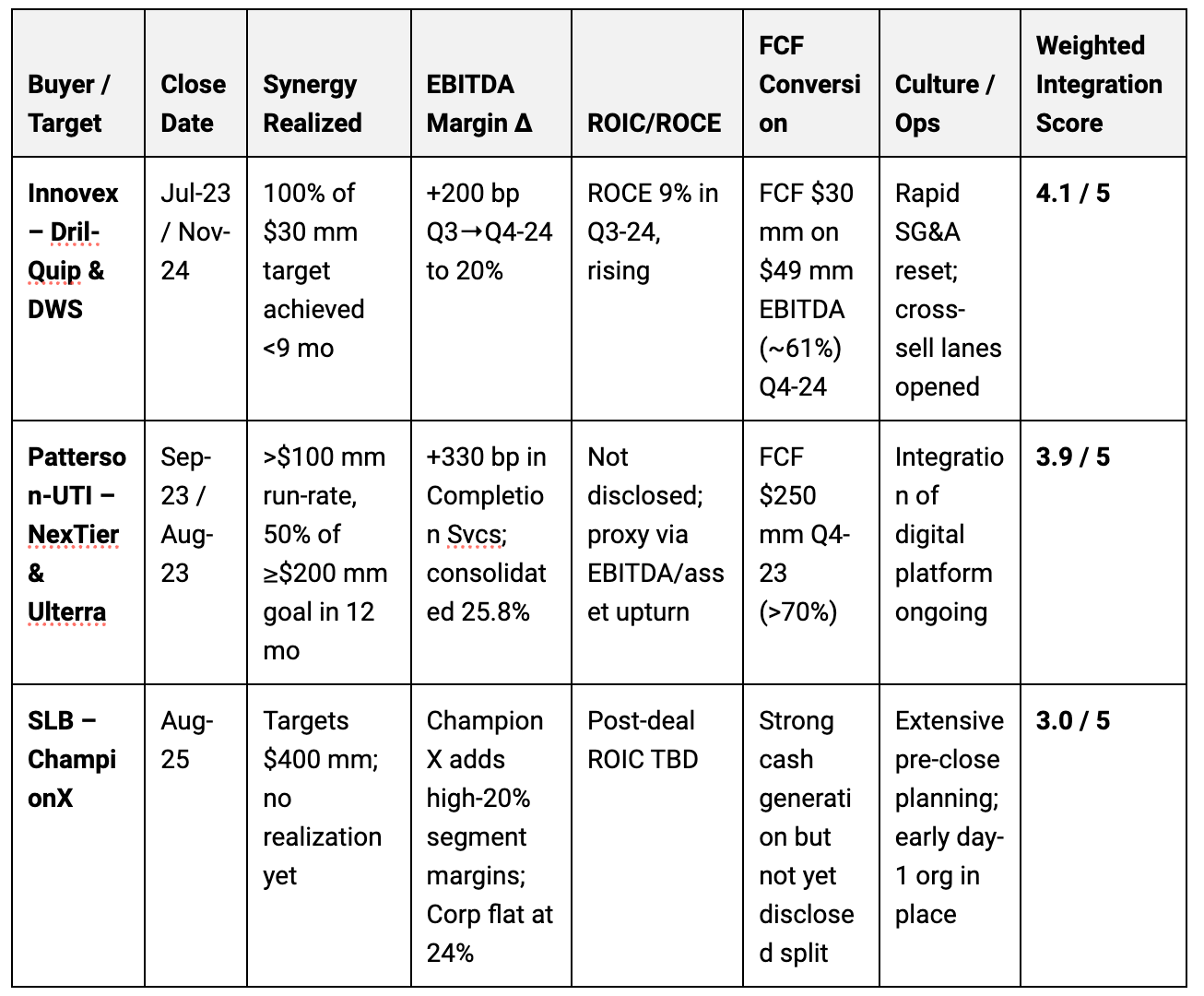

Worked example. Innovex.

Synergy: 100% of the stated target inside roughly nine months → 5.0.

Margin: +200 bp consolidated lift → 4.0.

ROCE: ~9% and rising vs an 8% hurdle → 3.5 pending more quarters.

FCF conversion: 61% → 5.0.

Culture/ops: Green, fast SG&A reset and cross-sell lanes opened → 4.0.

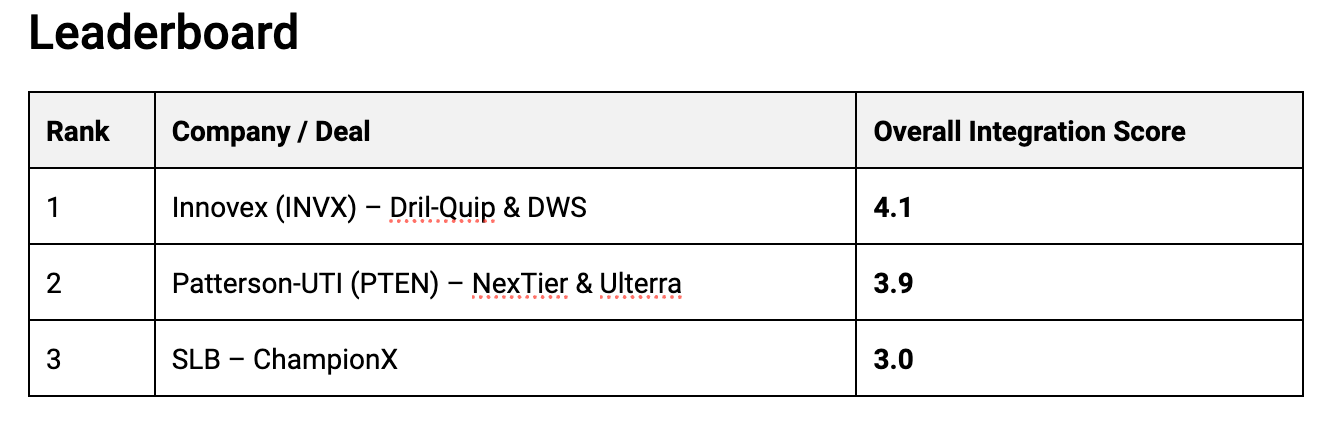

Weighted: 1.50 + 1.00 + 0.70 + 0.75 + 0.40 = 4.35, rounded to 4.3. Even at a stricter neutral ROCE, the composite is 4.1. Either way, Innovex leads on the two things that matter most: speed of capture and cash discipline.

PTEN scores high on margin and scale but realized about half of its ≥$200m synergy run-rate in year one, with less ROIC transparency, so it sits in the high-3s. SLB↔ChampionX is early. Targets are large, realization is not yet visible.

Sensitivity. If SLB books 25% of its $400m target inside 12 months, its synergy score lifts, but the composite still trails because timing and cash carry more weight than size. KLX’s +900 bp margin step is real, but negative FCF and a Red culture flag cap the composite. One gaudy KPI cannot bury structural weakness in this model.

Bottom line. Innovex’s differentiation is not a slide. It is a scorecard: fastest synergy harvest, early margin accretion, capital-light cash generation, and culture that accelerates rather than drags.

Bridge. Being different is not the goal. Being different where the other side feels it is. If you recite the Iliad in Greek at karaoke, the crowd will still ask for Journey. On to leverage.

The Law of Leverage: When Uniqueness Meets the Other Side’s P&L

Differentiation matters when it maps to the counterparty’s problem. We built a six-factor diagnostic to find the situations where speed of integration is not a nice-to-have but a pressure relief valve.

Strategic adjacency ≥50%. Day-one relevance. Familiar customers and channels.

Market concentration ≤25% combined or ΔHHI <100. Timing is leverage. Avoid second requests.

Synergy magnitude ≥10% of target sales. If the pool is not dense, the juice is not worth the squeeze.

Payback ≥1.5x within 36 months. Capital discipline.

Key-leader retention ≥70% on 24-month paper. Talent is the rate limiter.

Capex/sales ≤5%. Capital-light profiles convert synergies to cash.

Public profiles. Company X, Y, Z. Capital-light consumables, overhead-heavy SG&A, trading at 4–8x when Innovex sits low-teens. Every turn of arbitrage is accretion once synergies show up. Depot rationalization, procurement scale, shared back office. Ten percent off SG&A flows to EBITDA. Free cash flow funds integration without tapping debt.

Private equity profiles. The high-leverage window is years six to eight of fund life. Easy levers are gone, bolt-ons unfunded, LPs want liquidity to seed the next vehicle. Not distressed, just motivated. Ideal candidates have been held four years or more, multiples are flat, and there are at least two actionable bolt-ons the sponsor has not financed. All-stock solves GP-LP tensions. LPs get liquid paper, GPs keep upside via rollover. You preserve cash and still print accretion.

The supply is there. Trillions of unrealized value sit in tens of thousands of companies. Hold periods stretch past six years. Continuation vehicles have fatigue. A buyer with a reputation for converting synergies in 100 days sets the terms.

Why speed prices the deal. Earlier EPS accretion, fewer months of dual-running costs, more sellers willing to take your equity because they can believe in the value creation timeline. That is leverage.

Bridge. Leverage without capture is performance art. The question is simple: can you encode your advantage into the terms.

The Law of Capture: Converting Differentiation into Financial Architecture

If you cannot express your edge in valuation, structure, and arbitrage, you are back to trivia. We institutionalize the translation. The result is a buyer profile that wins at equal or lower headline because the economics are wired to your strength.

Financial logic. Private tuck-ins trade at 3–6x EBITDA and close quickly. Public platforms print 10–13x and care about optics. The spread is worth four turns if you can show credible synergy timing. Our guardrails keep pro-forma multiples at or below 9x post-synergy, maintain net debt to EBITDA under 3.0x, and cap dilution under 15%. This is not about paying more. It is about paying smart.

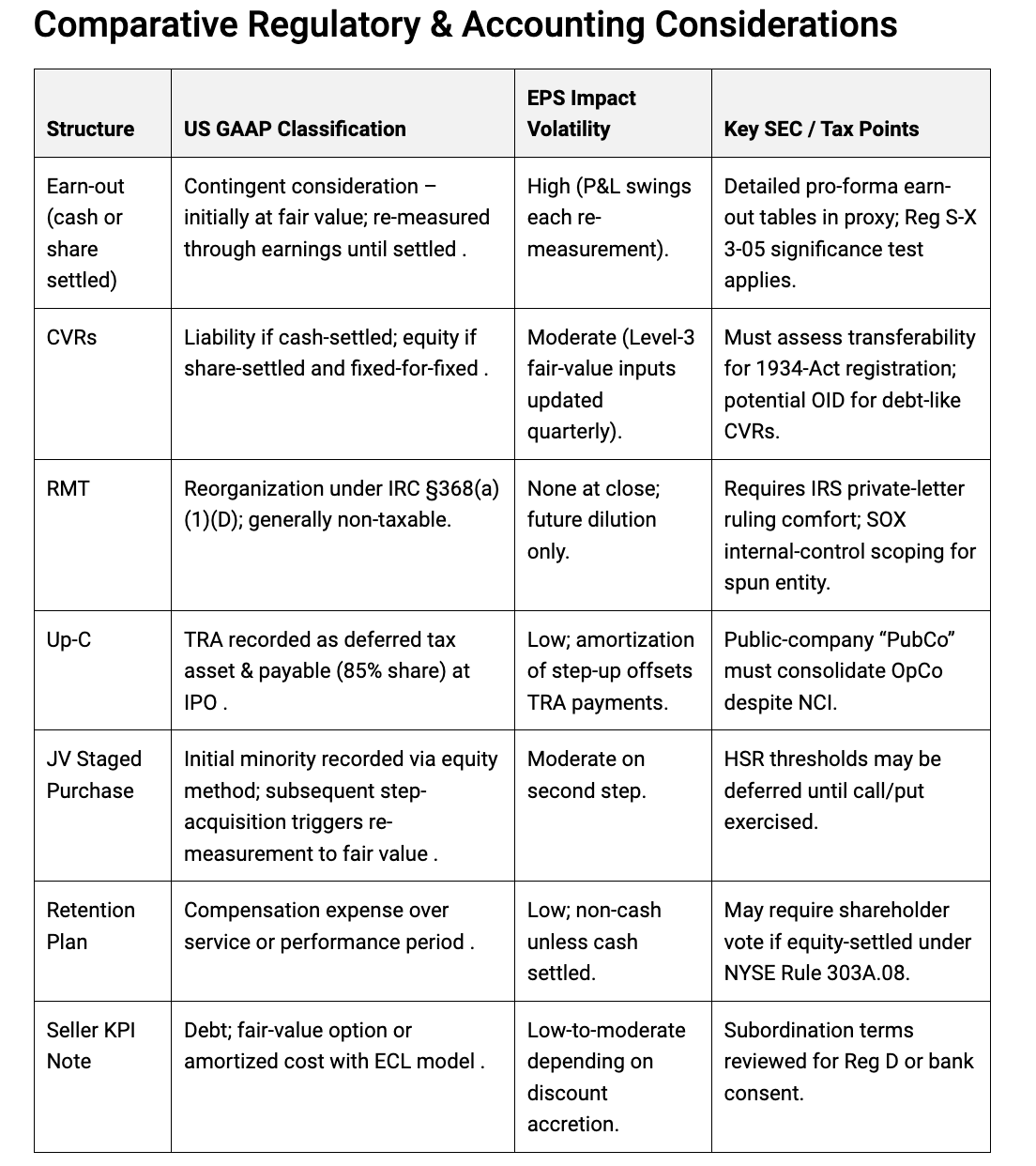

Structures that encode the edge.

Earn-outs and milestone equity swaps. Tie up to 40% of consideration to integration KPIs: synergy run-rate, IT cut-over, churn. Sellers keep upside. You defer cash and fair-value the liability under ASC 805/820.

Contingent value rights. Rights that convert to cash or stock only if performance hits. Headline multiple looks conservative. Sellers keep a “kicker.” Accounting remains controlled until milestones become probable.

Reverse Morris Trust with staged call/put. Tax-efficient spin-merge now, completion when KPIs validate. You “test-drive” and accrete when it is real.

Seller notes linked to integration KPIs. Subordinated interest with principal reductions if synergies miss. Fixed-income floor for the seller, discipline for you.

Hybrid capital stack. Equity-credit preferreds, rollover equity, seller notes. Ratings intact, dilution contained.

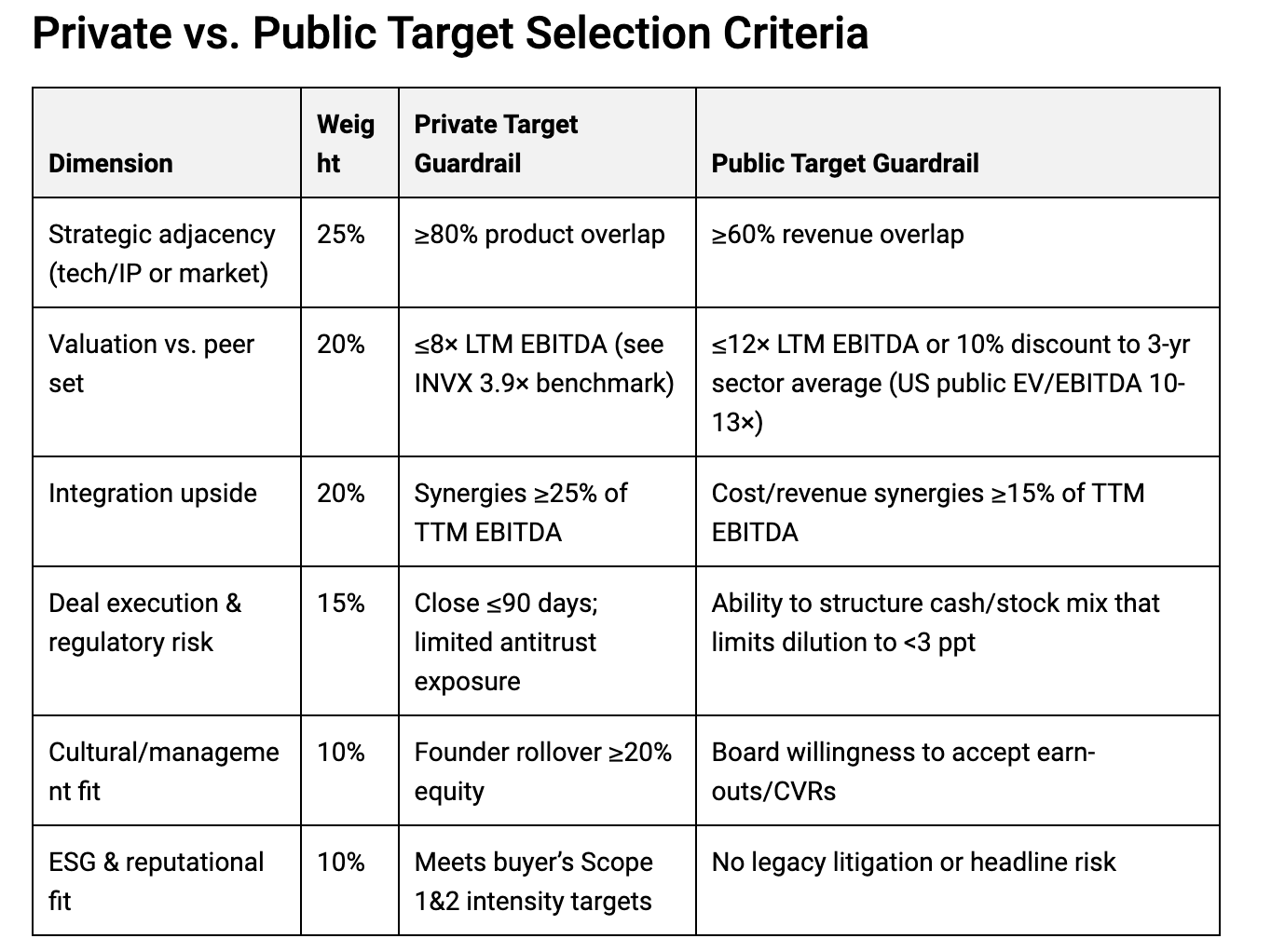

Playbook by target.

Private tuck-ins. Adjacency ≥80%, founders roll ≥20%, synergy ≥25% of TTM EBITDA, close in 90 days, release earn-out tranches inside 24 months.

Public platforms. Revenue overlap ≥60%, cost and revenue synergies ≥15%, stock-heavy consideration layered with CVRs and earn-outs so boards get optics and you keep accretion.

Behavioral science and MESOs. We never show one offer. We show a MESO set that is value-equivalent to us and diagnostic to them. All cash with a tax shield for a year-seven PE fund. Equity rollover for founder upside. CVRs and earn-outs for boards that need a headline. Whatever door they pick, it leads to your economics.

What success looks like. Two privates and one public in twelve months. $500–700m of revenue added, $90–110m of EBITDA, $60–80m of run-rate synergies at 24 months with half in year one. Net debt to EBITDA below 3.0x. Less than 15% dilution. That is not aspiration. That is arithmetic when capture is wired to your edge.

Case Study: Psychedelic Medicine Sell-Side

So far, this is theory mapped to Innovex. Let’s prove the method travels. A real engagement, different industry, zero home-field advantage.

Market backdrop. Psychedelic therapeutics sit in the low single-digit billions today with mid-teens CAGR into the next decade. Spravato validated the model with a billion-plus run-rate, more than 4,500 certified delivery sites, and a reimbursement pathway. None of this happens at a retail counter. Treatments require supervised in-clinic administration. Clinics are the infrastructure.

The client. A Colorado interventional psychiatry clinic and early adopter of psychedelic-assisted therapy.

Most experienced operator. More sessions delivered than any peer. In a new category, repetition equals trust.

Figurehead practitioner. A brand in human form with credibility across conferences and journals.

Operational readiness. Protocols, reimbursement, infrastructure. Turnkey for expansion.

Strategic timing. Motivation to close before a key FDA event and a favorable political window.

They had over twenty unsolicited inbounds without ever running a process.

The buyer. A private family investment group with a track record in high-end adolescent rehab. Their edge was unlocking payor reimbursement for niche care. The parallels to psychedelic psychiatry were obvious. They wanted a beachhead. Other family members were active in adjacent healthcare. They wanted the practitioner front and center and retained in leadership.

Relativity. We quantified the client’s uniqueness: treatment volume, practitioner brand, and operational readiness. Not attributes, proof.

Leverage. We modeled the buyer’s BATNA. Recreate this platform from scratch and you spend years recruiting, burn real money on clinician incentives, and still cannot buy trust. High replication cost means non-fungible differentiation.

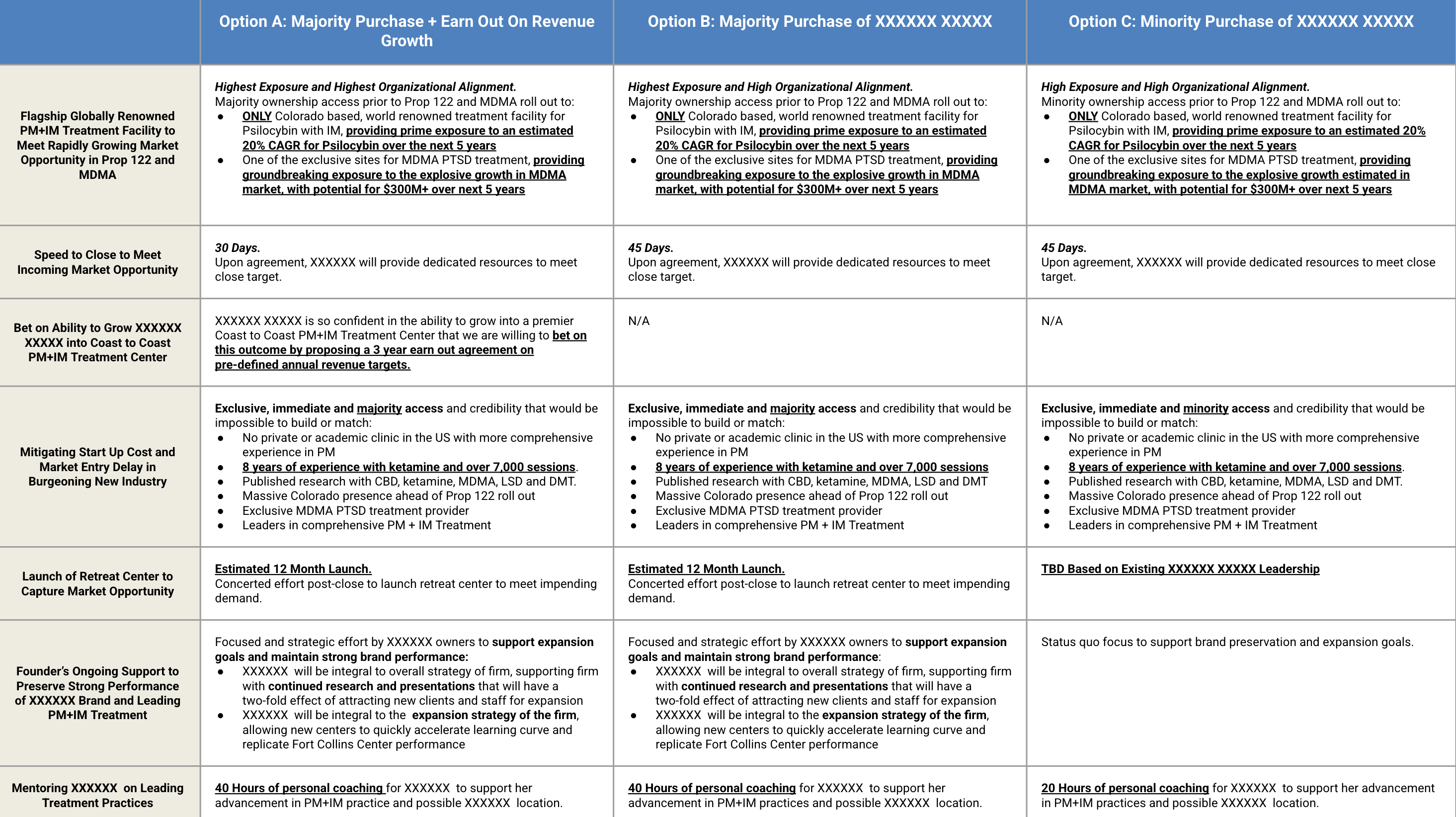

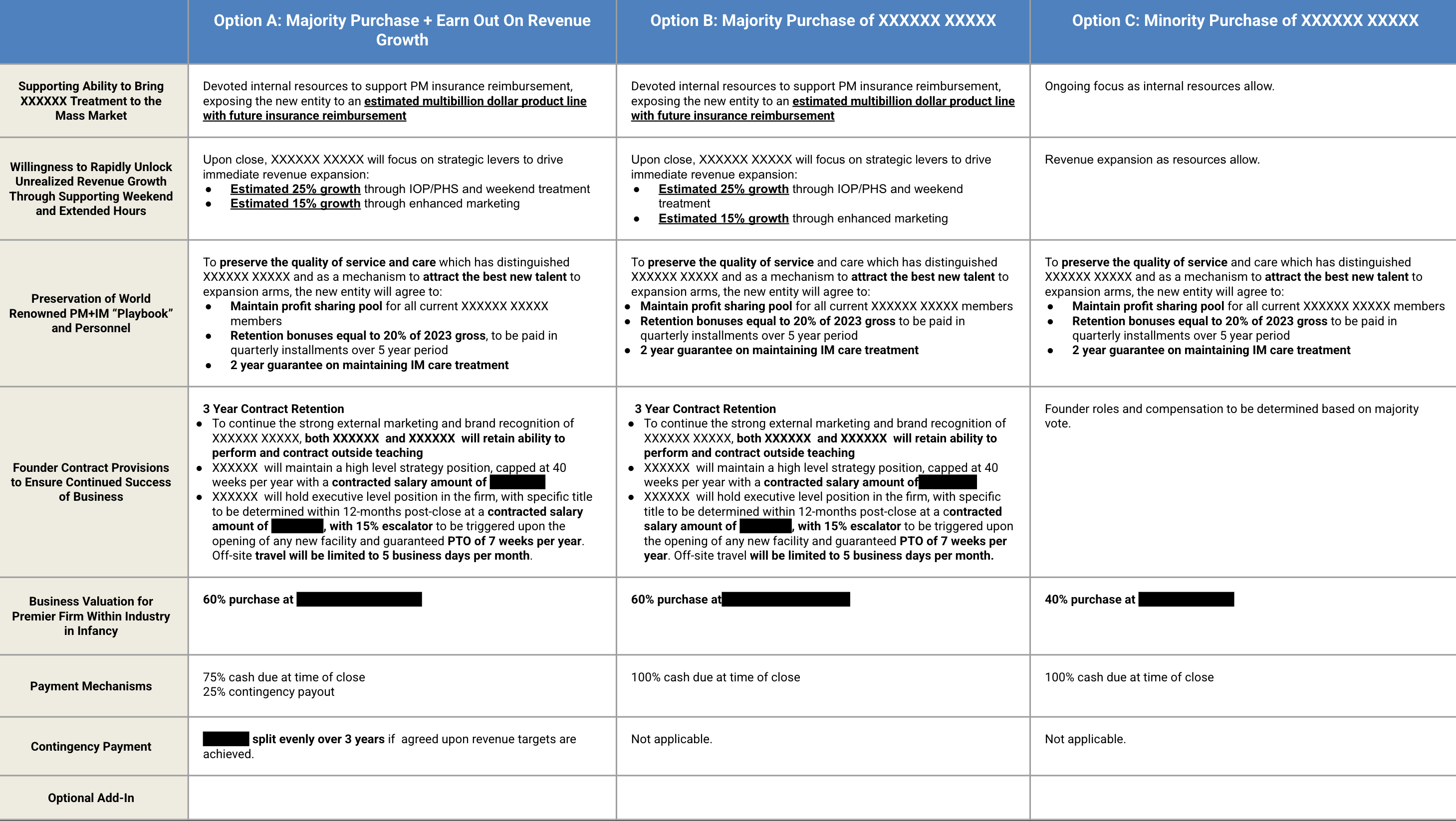

Capture. We built a MESO and re-anchored. Three options.

A. Majority purchase with a performance-based earn-out tied to revenue milestones and integration KPIs.

B. Majority purchase all cash at a discount to A’s economics.

C. Minority investment with lighter involvement.

Each option baked in retention architecture, founder role clarity, immediate growth levers, a buyer-side insurance unlock, and a new-market entry plan. We expected two rounds and designed the set so landing on A’s structure at C’s initial headline would still clear our targets.

Outcome. A three-times uplift versus the initial unsolicited anchor, employment and retention terms on our client’s sheet, and a timeline synchronized to regulatory events. The buyer felt they “won” on upside. We locked downside and sequence.

Why it matters. This was not OFS. It was psychedelic medicine. New space, new rules, same result. Relativity, Leverage, Capture turned intelligence into engineered outcomes. If we can do that in a domain we learned on the fly, imagine what we do in a domain we know cold.

Stop Tilting. Start Taking Ground.

Don Quixote memorized the code and charged the windmills. That is what the industry does when it mistakes data for advantage.

Kalibr does the opposite. We take the same raw inputs and run them through Relativity, Leverage, and Capture until they become something no one else can copy: your advantage, wired to their incentives, locked into the paper.

Not trivia. Not theater. Prescriptive outcomes.

What that means:

M&A. Differentiation quantified, BATNAs mapped, terms that monetize your speed. Earn-outs, CVRs, staged calls and puts, hybrid stacks, clear guardrails on leverage, dilution, and payback. Deliver an integration-indexed term sheet and a 100-day sprint sellers prefer over a higher headline.

Sourcing and contracting. Vendor economics inverted, pressure points exposed, MESO contracts with pass-throughs and option value you actually exercise. Deliver a BATNA scoreboard, a leverage-utilization score, and a clause library that moves free cash flow without touching a frac stage.

Sales and pricing. Your wedge isolated, buyer P&L triggers prioritized, offer portfolios that make saying “yes” the path of least resistance. Deliver counterparty-specific packages that lift win rate and shrink cycle time.

Same data. Different outcome. We do not swing at windmills. We decide which mills to build, price the power, and write the offtake.

That is the cure to the Don Quixote Problem:

Relativity makes you unmistakable.

Leverage makes you irresistible.

Capture makes it bankable.

If you are ready to retire the costume armor and start taking ground, we will bring the lenses, the playbooks, and the term sheets.