Read the rent roll before your next compression renewal

We rebuilt the Permian compression fleet unit by unit. Your vendor knows its book down to the engine and the renewal date. Now you can too.

Nominally Hedged is Kalibr Partners’ briefing on what oil and gas actually costs: every category, CAPEX to OPEX, proprietary data systems, interpreted through a commercial lens. Whichever side of the negotiating table you sit on, you are the intended reader. The data is neutral: the iron does not change shape depending on who reads it. In any single engagement we sit on one side of the table, and we tell you which.

When you buy an apartment building, the seller hands you a rent roll. It is a single sheet, and it is the most important sheet in the transaction: every unit, who lives in it, what they pay, when their lease ends. It is also, in the hands of a motivated seller, the most creative sheet in the transaction. Occupancy gets rounded up. A tenant who is sixty days late is still, technically, a tenant. A lease that expires next quarter looks exactly like a lease that runs four more years, because both are just a date in a column, and the column does not tell you which dates the seller is praying about.

So nobody who does this for a living believes the rent roll. They verify it. They send every tenant an estoppel certificate, a boring legal form that asks the tenant to confirm, in writing, the one thing the seller has every incentive to shade: what they actually pay and when they actually leave. The estoppel is a verification technology. It exists because the asset is observable (you can walk the building) but the income is a story (you cannot walk the leases), and in 2022 and 2023 a great many people who had skipped the estoppel and trusted the pro forma discovered the difference between the two when their floating-rate debt repriced and the collected rent turned out to be a number the spreadsheet had been optimistic about.

There is a name for the general problem, and it is older than the apartment syndication. In 1970 George Akerlof published “The Market for Lemons,” and the insight that won him a Nobel was this: when the seller can see the quality and the buyer cannot, the buyer rationally stops believing the seller’s description and prices the average instead. The good used car and the lemon sell for the same number, because from the buyer’s seat they emit the same signal. The only thing that breaks the pooling is verification: a way for the good car to prove it is good, which is to say, a CARFAX. An independent record of the asset that the seller does not author.

Compression is a rental business that runs on a rent roll nobody outside the vendor has ever read.

I have written before that the compression vendor is a REIT. The model is exact enough to use, not cute: the vendor owns the iron, finances it, and rents it to you at a rate that behaves like a yield on book value. A vendor’s accountant would tell you the rate is contract revenue and the book value is on a different schedule, and that is true; the point is not the ledger, it is that the rate moves with the capital base the way rent moves with a building, and reading it that way predicts what the vendor will and will not give you. Kodiak, Archrock, and USA Compression are the three big public landlords of the Permian, and like any landlord they tell a story about their buildings. They tell it to equity analysts on quarterly calls, and they tell a compressed version of it to you across the renewal table, and it is a good story: diversified tenants, blue-chip credit, ninety-eight percent uptime, seven-to-ten-year leases. You cannot verify any of it from your pad. You can see your unit. You cannot see their rent roll.

So we built the estoppel. For the entire Permian.

Before the rest of this, the punchline, because withholding it would be its own kind of story: we reconstructed the Permian compression fleet from the asset up, unit by unit, operator by operator, and then we did the one thing the equity story never invites, which is reconcile it against each vendor’s own Q1 2026 filings. Most of it ties out. That is the point. The bottom-up iron agrees with the top-down disclosures often enough that you can trust the places where it does not, and it stops agreeing in two specific, expensive places, and it sees a third thing the disclosures were never built to show. One landlord’s diversification is a single tenant. All three landlords’ “long-term” lease books reprice a lot sooner than the word “long-term” is doing on the call. And underneath the brand on every skid is a specific engine, with a specific lead time and a specific scarcity, which is the thing that actually sets your leverage and the one thing no rate card will ever show you.

And it is urgent, not merely interesting. The Permian’s gas problem is structural and getting worse: as the basin’s wells age, the gas-to-oil ratio climbs, associated gas keeps rising whether or not anyone wants more gas, and all of it has to be compressed to move. Demand for horsepower here is not cyclical, it is geological. And the iron to meet it sits on a 110-to-180-week lead time for large new builds, which means the installed fleet is not a commodity you can re-source on a phone call. For two and three years out, it is the only fleet there is. When supply is that tight and that slow, every renewal is a seller’s market, and the one thing that arms the buyer is knowing the seller’s book better than the seller expects you to.

Kalibr packages what follows two ways, one per reader. If you run compression spend for an operator, there is a Permian Compression Benchmark built for your side of the table. If you sell compression, or finance the people who do, there is a Permian GTM Targeting read built for yours. A fair question is how one shop arms both sides, and the answer is the thing that makes the data worth trusting: the iron is the iron, and the fleet does not rearrange itself depending on who is looking. The dataset is neutral; the representation is not. In any single engagement we sit on one side of the table and say which, and the read built for the other side is not one we run against the client we took. Both products are below. If either is your problem, the fastest path is to message us; the rest of this explains why the data underneath them is worth the conversation.

The Iron Agrees, Until It Doesn’t

Before the rent roll, the building. How big it is, and why you should trust a number we built from the iron up instead of one the vendor handed you, which matters more than it sounds: the entire argument that follows depends on the bottom-up agreeing with the vendors, right up until the moment it doesn’t.

The Permian carries roughly 6,380 compression units in our database, and we work the 2,855 we can attribute to one of the three public landlords by name, 2,360 of them active (1,765 in Texas, 1,090 in New Mexico). Kodiak, Archrock, and USA Compression are the consolidated, investable core of this market, and the three counterparties an operator is most likely to be sitting across from when the lease comes due; the rest of the basin is a fragmented tail of smaller fleets that this analysis is not about. Every number in this piece is a unit we can put a vendor’s name to, and the totals reconcile to the vendors’ own filings. If we cannot attribute it, we do not report it.

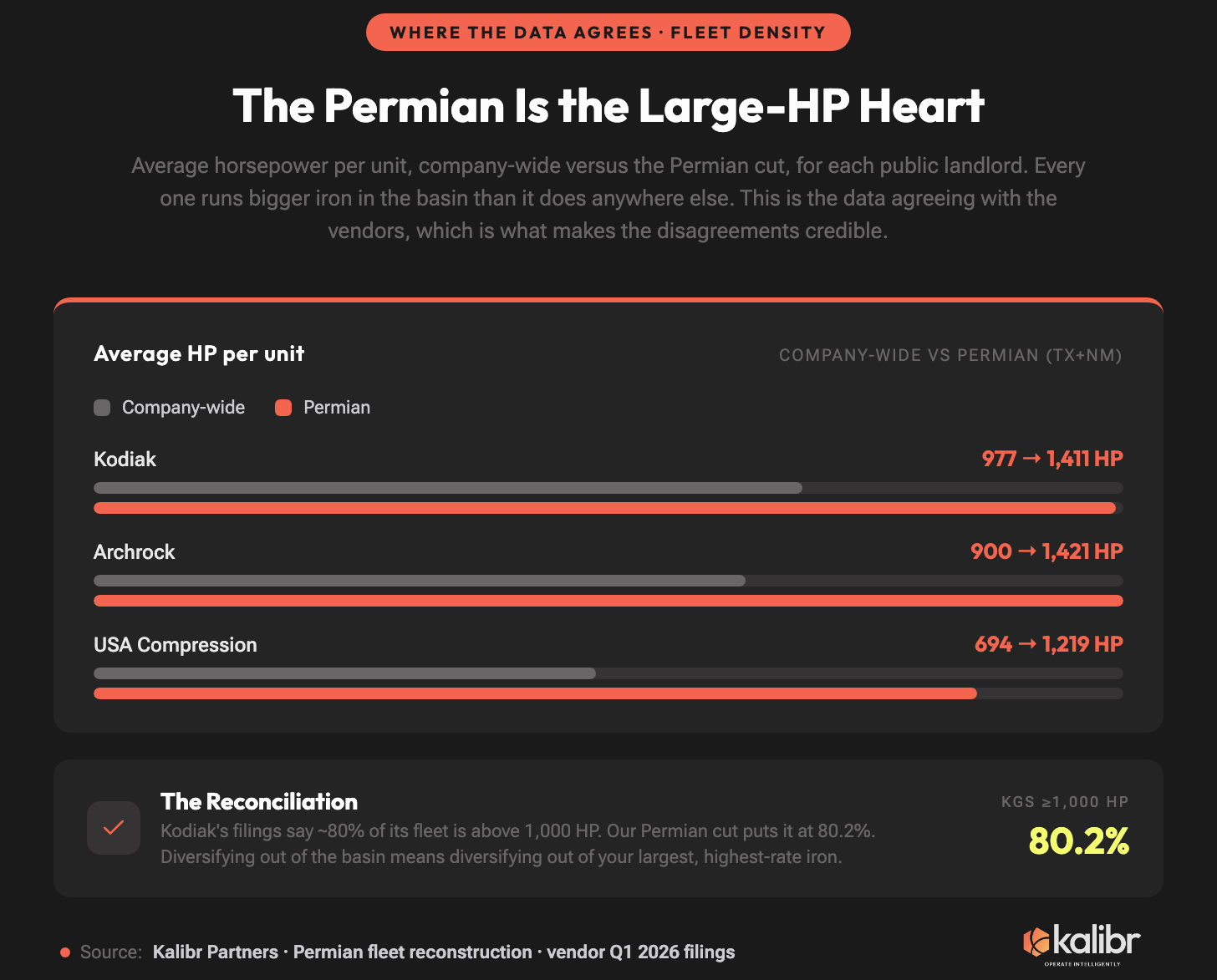

Here is the first thing the iron says, and it says it in agreement with the vendors, which is exactly why it is useful. Every one of these three is bigger in the Permian than it is anywhere else. Kodiak’s company-wide fleet averages 977 horsepower per unit, Archrock’s around 900, USA Compression’s 694. Their Permian fleets average 1,411, 1,421, and 1,219. The basin is where the large iron lives, the G3600s and the high-rate gathering units, the equipment with the highest rate per horsepower and the longest lead time. When Kodiak’s filings say its fleet is roughly 80% large horsepower above 1,000 HP, our Permian cut puts it at 80.2%. When the companies rank themselves by fleet age, our vintage data puts them in the same order they put themselves. The bottom-up reconciles to the top-down.

That reconciliation is the credibility engine, so I want to be honest about where the data argues “for” the vendors before it argues against them. Kodiak really does run the youngest fleet of the three. USA Compression really is the most pressured, and its own disclosures say so as loudly as our data does. Archrock’s equipment really does sit on location for years, exactly as it claims. A model that only ever found problems would be a model worth ignoring. This one finds agreement first, which is the only reason the disagreements are worth your time.

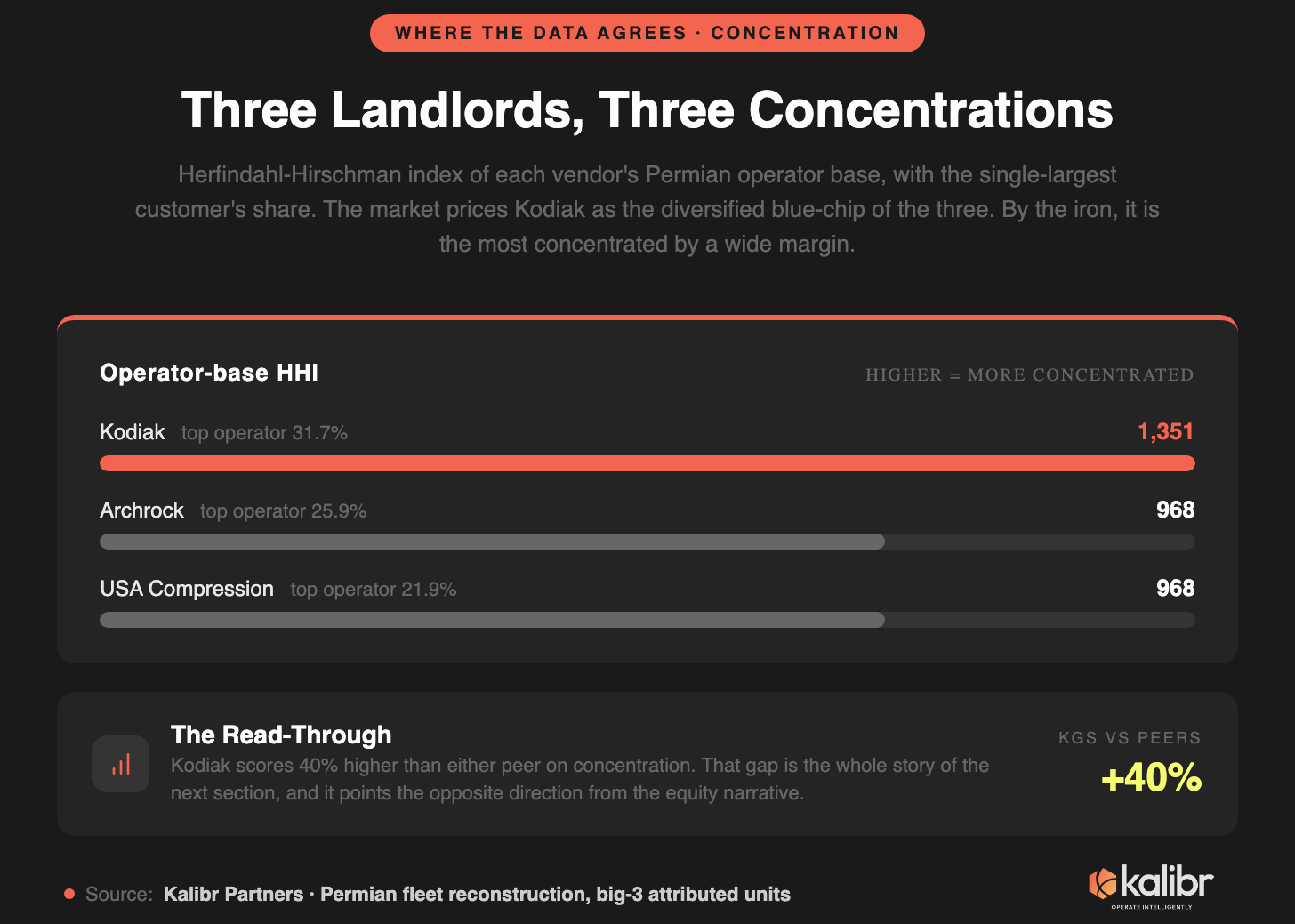

Now the concentration. Run a Herfindahl on each vendor’s Permian operator base and Kodiak scores 1,351 against Archrock and USA Compression at 968 apiece. That gap is the whole story of the next section, and it runs the opposite direction from the one the equity narrative is selling.

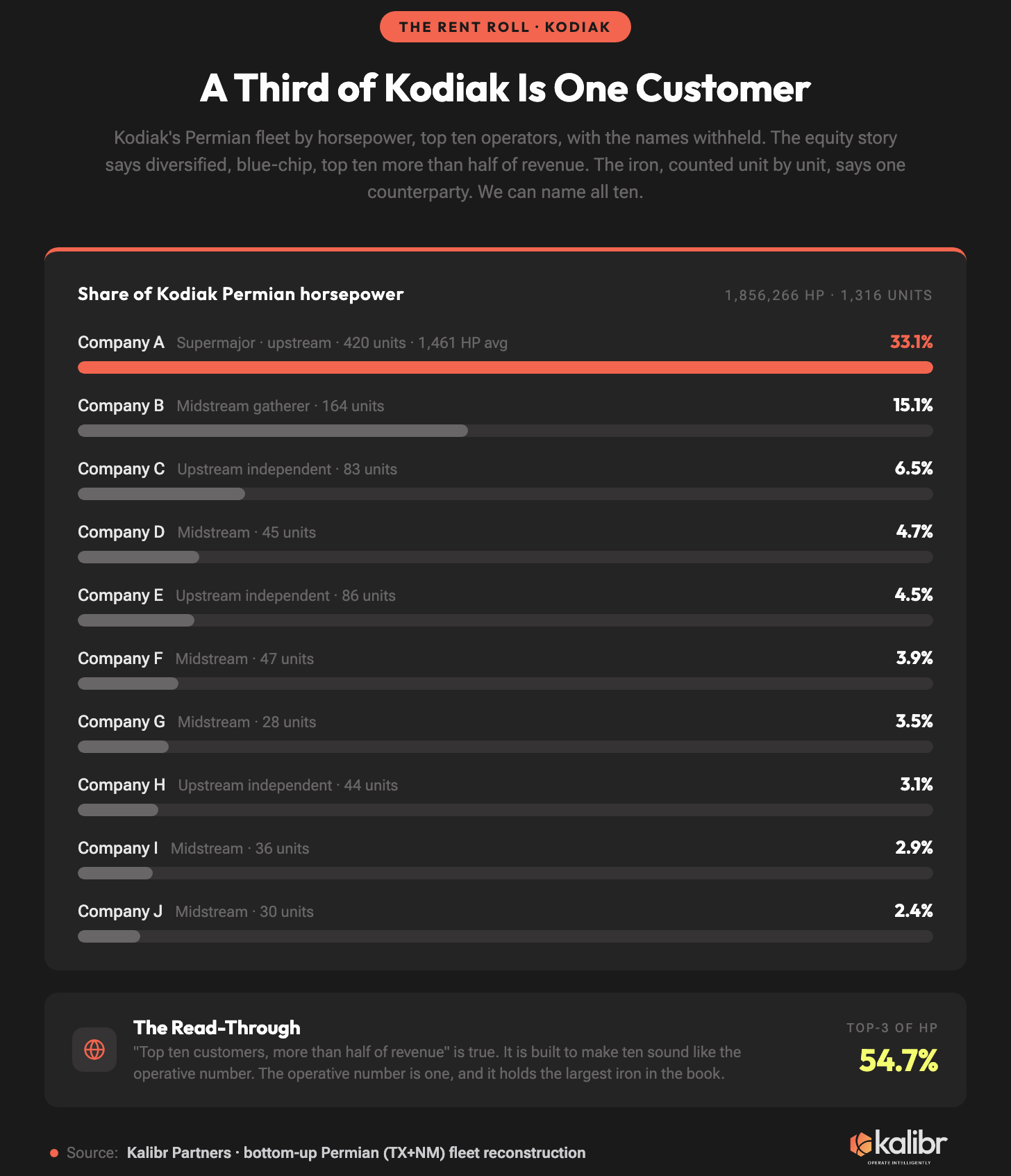

A Third of Kodiak Is One Customer

Kodiak is the market’s favorite compression name, and the case is good. Youngest fleet, highest rate per horsepower, 98% utilization, a pricing environment management expects to run “to 2027 and beyond.” The customer base is described the way you would describe a well-run REIT: top ten customers more than half of contract services revenue, investment grade above 60%, a disclosed roster that reads like a blue-chip index, supermajors and the largest shale independents and the midstream majors. The company describes its mix as roughly 30% upstream and 70% midstream. The word the story wants you to hear is “diversified”.

Here is the rent roll.

Company A, a single investment-grade supermajor, is 420 of Kodiak’s Permian units. That is 31.7% of its attributed Permian fleet by count and 33.1% by horsepower: 613,790 of 1,856,266 horsepower, set behind one logo. The top three operators are 50.7% of the units and 54.7% of the horsepower. And this is not cheap gas-lift volume parked to pad a count. Company A’s Kodiak units average 1,461 horsepower, with 81 of them at 1,500 or above. It is the largest iron in the book, behind the single largest counterparty.

Two honest notes on basis before the conclusion, because they are the difference between a finding and a number you should not trust. The disclosure counts revenue; we count units and horsepower, which is not the same denominator, and we will not pretend it is. And our share is the operator we attribute to each skid from asset data, not a contract we have read. Neither caveat moves the shape. Operator attribution is the part of this dataset we stand behind hardest, populated on essentially every unit, and a third of the core-basin iron sitting behind one counterparty is a fact about the fleet, which is the thing we can see directly, where revenue is the thing the disclosure chooses to show you.

“Top ten customers more than 50% of revenue” is true. It is also the sentence doing the most work in the whole disclosure, because it is built to make ten sound like the operative number when the operative number is one. A third of the core-basin fleet behind a single counterparty is not what diversification means. It is what a levered bet on one drilling program means, and the word for the risk it creates is not concentration, it is hold-up: when you have sunk capital that is specific to one counterparty (and a 1,461-horsepower unit on Company A’s pad is about as specific as capital gets), the counterparty holds the option, and everyone in the relationship knows it.

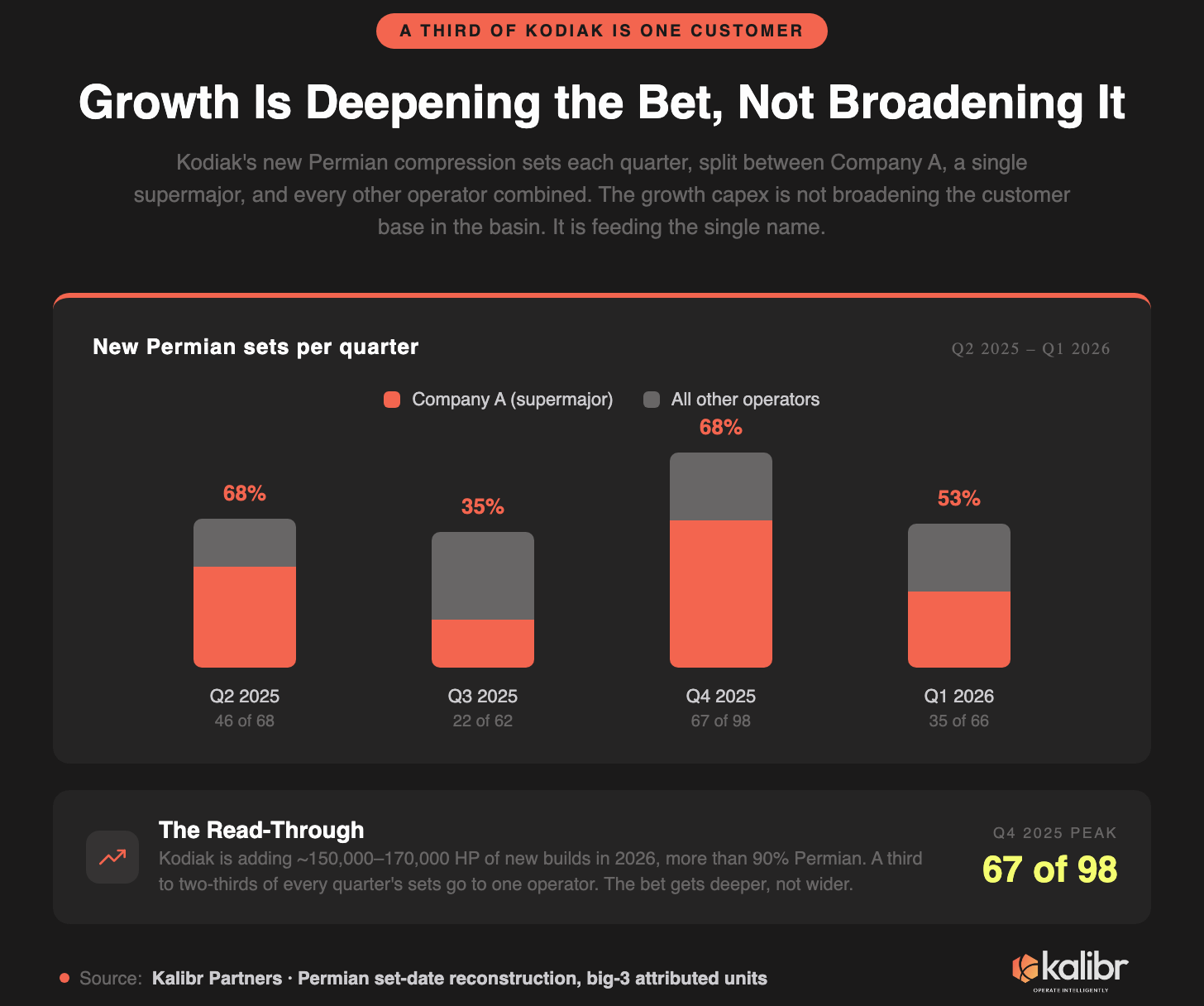

It gets more concentrated, not less, which is the part the growth story inverts. Kodiak is deploying roughly 150,000 to 170,000 horsepower of new builds in 2026, more than 90% of it Permian, essentially all pre-contracted, and the equity story reads that as broad secular growth. The sets say it is feeding the whale. Company A was 46 of 68 Kodiak Permian sets in Q2 2025, 22 of 62 in Q3, 67 of 98 in Q4, 35 of 66 in Q1 2026. Call it a third to two-thirds of new sets every quarter, going to one operator. The growth capex is not broadening the customer base in the Permian. It is deepening the single name.

None of this makes the bet a mistake. Anchoring your fleet to one of the best-capitalized operator in the basin is what you would do if you could: Company A pays, Company A drills through cycles, Company A is the counterparty you want when oil prices sell off. The bet is the right bet. It is also, unmistakably, a bet, with a name and a risk profile, and the equity story has dressed it as the absence of one. For the operator on the other side of it, the gap between those two readings is the whole opportunity: the most important fact about your Kodiak relationship may be how badly Kodiak needs Company A’s drill schedule to stay exactly as good as it is.

Compare the other two landlords, because the contrast is the proof. Archrock’s largest Permian customer is 144 units averaging 932 horsepower, with 4.2% of them at 1,500 or above. USA Compression’s largest is around 100 units averaging 713 horsepower, 5.3% large. Their whales are small wellhead fleets. Kodiak is the only one of the three whose biggest tenant gets the biggest iron, which is the asset-level signature of a concentrated bet that the other two, whatever their other problems, did not make. Hold that fact, because the build years say it again in the next section, by a different measure entirely.

Read the rest. The engine map, the roll-off calendar, and the operator’s playbook are for paid subscribers.