Nominally Hedged | The Oilfield Built a Bloomberg Terminal for CAPEX. The next decade is an OPEX problem.

Maintenance CAPEX pressure, dwindling Tier 1 inventory, and PDP-focused financing models are about to turn the industry's most neglected line item into its most consequential one.

Here is a thing that happened in oil and gas between 2010 and 2025. Operators spent extraordinary organizational energy building market intelligence infrastructure around drilling and completions. Enverus, Novi, Rystad, the whole ecosystem. Type curves calibrated to the lateral foot. D&C cost indices tracked with the precision of Fed funds futures. Formation evaluation that would embarrass a neurosurgeon. The frac spread evolved from artisanal craft to a logistics operation so optimized that the limiting factor is often just the permit.

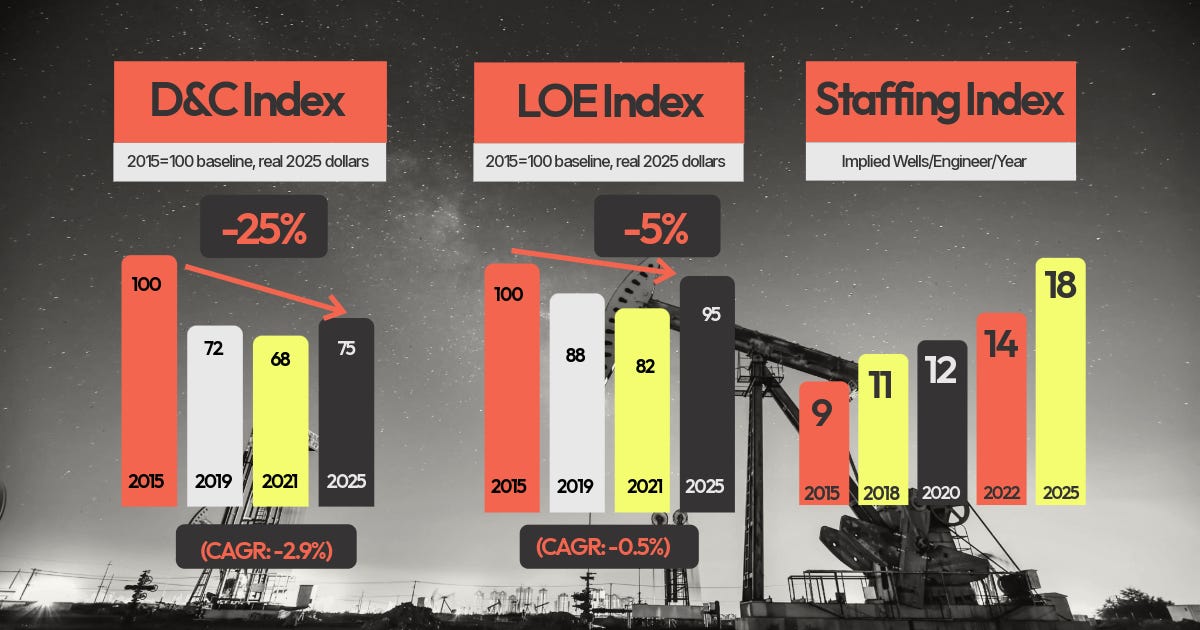

It worked. D&C costs fell roughly 25 points on a 2015-indexed basis. Genuinely impressive, especially considering the service sector was extracting every possible margin on the way up.

Then everyone looked up from their completions dashboards and noticed that LOE had moved about five points over the same period. Five. The gap between those two numbers is not explained by the relative difficulty of the problem. It is explained by where the industry decided to point its analytical infrastructure.

The oilfield decided that finding and drilling hydrocarbons was the interesting problem, and then proceeded to solve it with genuine intensity. The fact that nobody built the same infrastructure for running the wells afterward is not a failure of imagination. It is a choice, legible in where the industry pointed its people, its capital, and its analytical resources for fifteen years. Drilling and completions teams got more of all three. Production teams got the same headcount and a bigger footprint.

The Kalibr staffing index makes that choice visible in a single data point: the same production team is now managing twice the operational footprint, with tools still pointed almost exclusively at the D&C side of the ledger. The industry did not just underinvest in LOE intelligence. It underinvested while the problem was compounding.

This is the gap. Compression is where it starts.

The Part Where My Last Piece Matters

Last week’s piece established the structural constraint on your compression vendor’s pricing. The short version: their $/HP/month is not a negotiating position. It is the number their entire asset base gets marked against on a consolidated basis for the equity story. When you ask for a rate reduction, you have not asked for a discount. You have asked them to call their auditors.

That analysis revealed where the flexibility actually lives: off-book accommodations that compensate without touching portfolio valuation. Free months, mobilization credits, escalator caps. The accommodations that never appear in the blended $/HP/month figure they report, but absolutely appear in your total cost of ownership if you know to ask for them.

That was half the problem. Here is the other half, and it has three pieces.

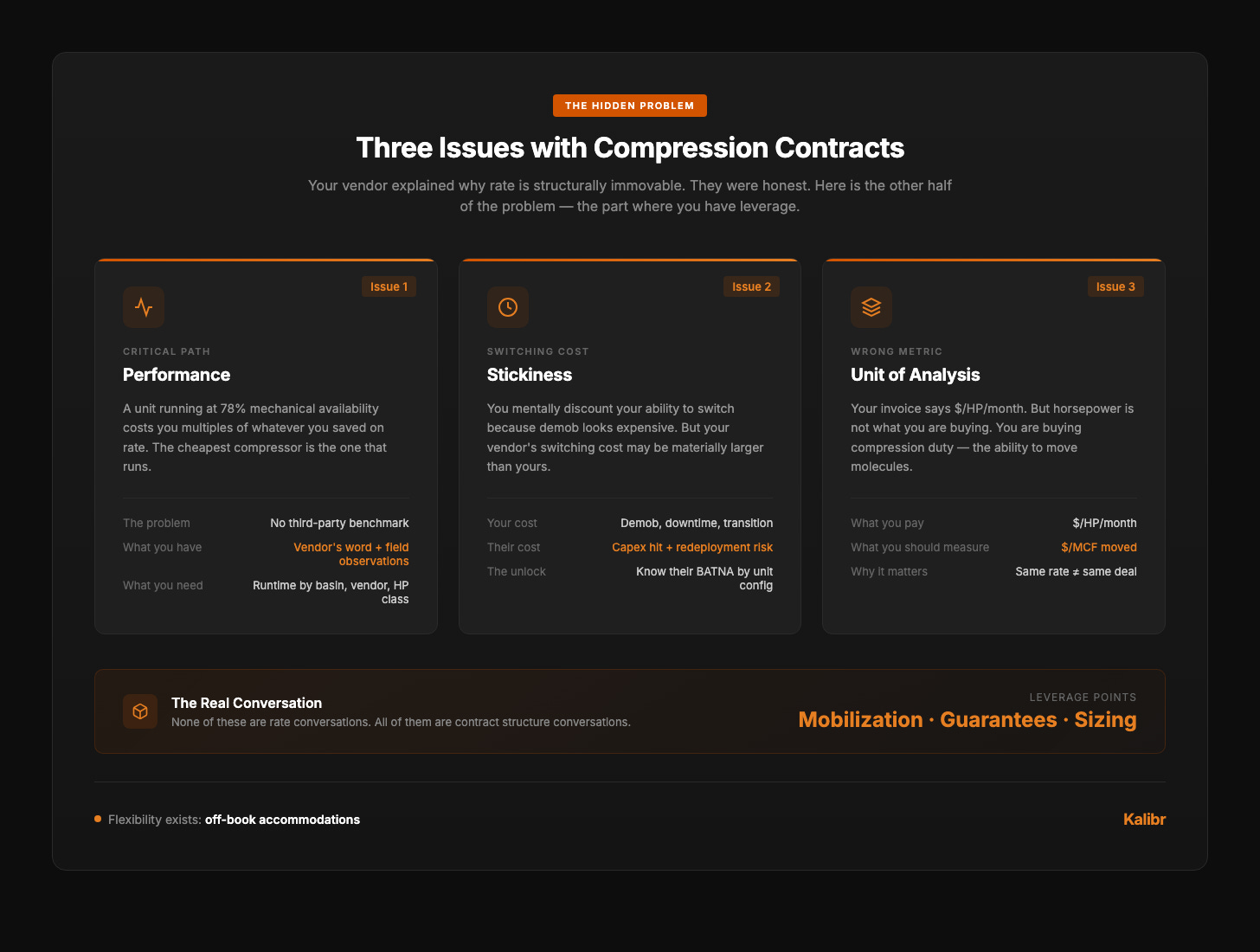

The first issue is performance. Compression is a critical-path service. A unit running at 78% mechanical availability is costing you multiples of whatever you saved on rate. The cheapest compressor is the one that runs. Everyone knows this. The problem is that there is no way to benchmark it. Vendors report mechanical availability in their investor presentations, but those are fleet-wide blended numbers that tell you nothing about the specific equipment class or basin where your wells actually sit. You have no third-party performance data. You have the vendor’s word and whatever your field team has observed firsthand.

The second issue is stickiness. Most operators mentally discount their ability to switch vendors because the demob economics look prohibitive. Downtime windows, new contract minimums, transition logistics, lost production. But consider the transaction from the other direction. Once that unit leaves your pad, your incumbent faces a maintenance capex event, uncertainty about whether the unit redeploys in-basin or gets trucked to another region, and carrying cost if it sits in the yard. Their switching cost is not necessarily smaller than yours. Depending on the unit configuration and current supply/demand balance for that HP class in your basin, it may be materially larger. A new vendor can flex on free months or a rebate structure that offsets your transition cost. Your incumbent knows this. And if you can estimate their redeployment risk by compressor configuration — which Kalibr tracks — you know exactly how much leverage you have before you walk into the room.

The third issue is the unit of analysis. Your invoice says dollars per horsepower per month. But horsepower is not what you are buying. You are buying compression duty: the ability to move gas from your wellhead to your sales meter at the pressure differential and flow rate your reservoir demands. Horsepower is how you get there. It is not the destination.

Nobody evaluates a frac spread on raw horsepower. You evaluate whether it delivers the treatment rate and BHTP your completion design calls for with enough redundancy to pump continuously. The HHP figure matters only insofar as it gets you there. Compression works identically. An oversized unit running at 60% load is not a good deal at any rate. An undersized unit as GOR rises is a production constraint dressed up as a line item. Neither shows up as a problem in the $/HP/month contract. Both show up in your net revenue.

The correct unit of analysis is $/MCF moved — what it actually costs to transport a molecule from your wellhead to the meter. This number integrates equipment sizing, utilization, runtime performance, and contract rate into a single figure you can compare across vendors, basins, and well types. It is also the number that nobody in your organization currently has. Getting there requires matching equipment specs to gas volumes and pressures, correlating runtime by vendor and basin, and having contract timing intelligence that tells you when your negotiating window opens.

That is what Kalibr built.

What Kalibr Compression Intelligence Actually Does

The platform is built on three layers of data that do not currently exist anywhere in a single integrated product. Each layer addresses one of the problems above.

Layer 1 is financial — the pricing benchmark. Every public compression provider discloses consolidated blended metrics: fleet HP, blended $/HP/month, reported utilization. What they do not disclose is how those numbers disaggregate by HP band, basin, fuel type, or contract vintage.

This is not an accident. The consolidated number supports the equity story. The disaggregated number would support your negotiation. So you get earnings calls that reference record pricing and 97%+ utilization without any detail on which equipment classes or basins are driving it.

Kalibr reconstructs that disaggregation. The methodology anchors to the one provider that breaks out HP band revenue in their 10-K and infers the band-level rate structure across the industry. The result is a benchmark matrix: $/HP/month by HP band, basin, vendor, and fuel type, with confidence intervals. This is the foundation — knowing what you should be paying before you walk into the room.

Layer 2 is operational — performance and timing. Kalibr’s proprietary asset dataset matches compression equipment in the field — by HP rating, set date, vendor attribution, and the gas volumes and pressures associated with it — to the producers operating them.

This match enables three things public financials cannot. First, regional runtime correlations by provider: which vendors are delivering mechanical availability above or below their marketed guarantees, by basin, by unit size, in aggregate across Kalibr’s observation set. This is the performance benchmark that does not exist anywhere else.

Second, contract timing intelligence: primary term exposure at the vendor level. This tells you when your negotiating window opens and when your counterparty is feeling renewal volume pressure — the information you need to structure flexibility into the deal.

Third, throughput economics. With equipment specs matched to production data, you can calculate actual compression duty and identify where you are paying for capacity that is not moving molecules. This is the $/MCF analysis.

The asset data is what turns financial benchmarking into operational intelligence.

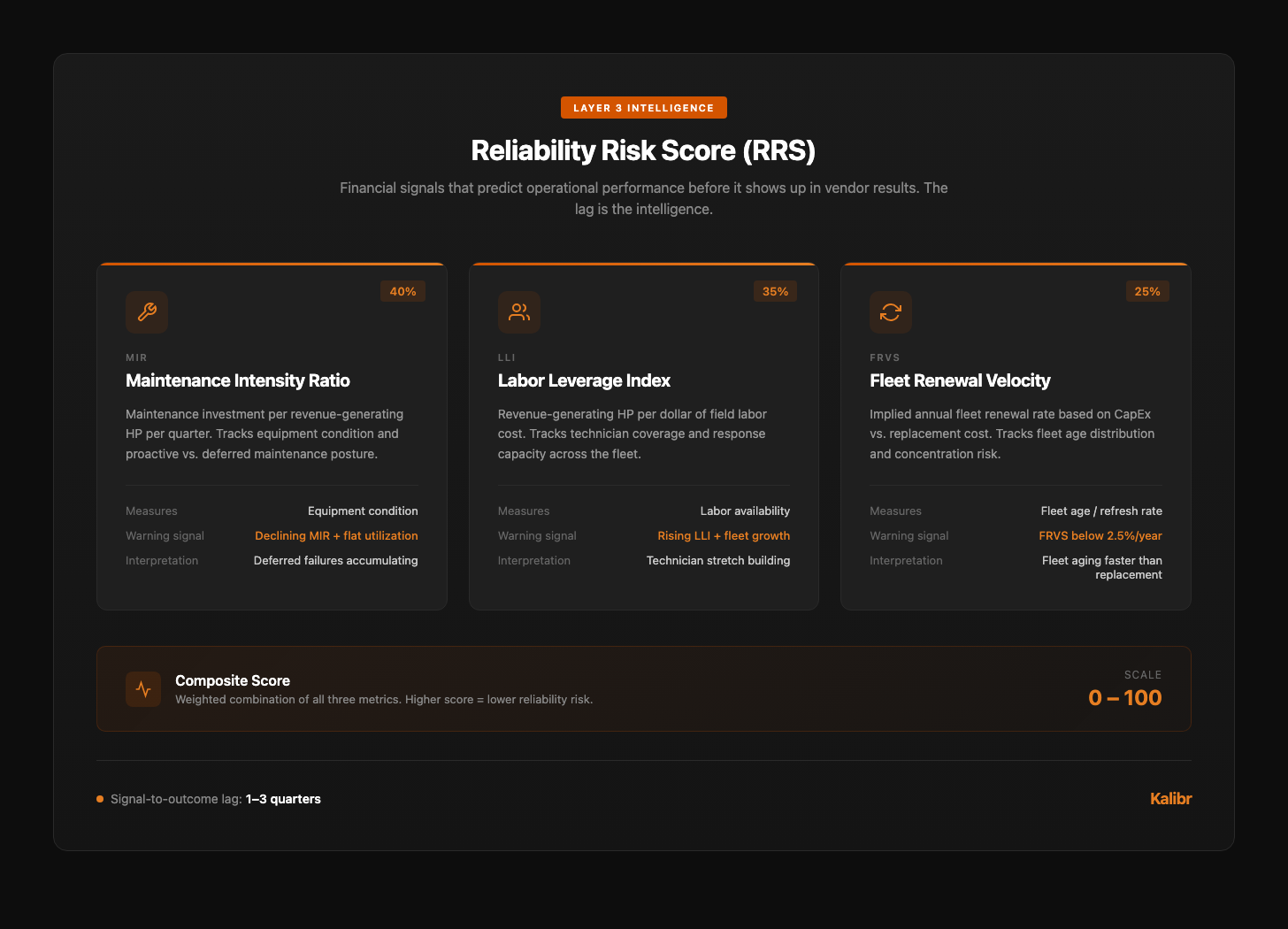

Layer 3 connects vendor financial health to your operational risk. This is the part that functions as a leading indicator — a signal that precedes the outcome by one to three quarters in the historical data.

The logic is straightforward. A vendor deferring maintenance to protect near-term EBITDA margins looks, in the income statement, like they are getting more efficient. Maintenance intensity is falling. Cost per HP is improving. This is the story the equity analyst is writing. It is also the story your account manager is telling you at renewal. What is actually happening is an accumulation of reliability risk that will surface in your operational results before it surfaces in their reported metrics.

The same dynamic applies to labor. A vendor stretching field technicians across more horsepower — HP per technician climbing, disclosed in the filings if you look — looks like productivity improvement. It is actually a response time and preventive maintenance backlog building in the field. The unit on your pad is not getting less attention because it needs less attention.

Kalibr tracks these signals through a composite Reliability Risk Score (RRS) that combines maintenance intensity, labor leverage, and fleet renewal velocity into a single 0–100 metric. A vendor whose RRS is deteriorating is one you want performance guarantees from (or optionality to exit) before the downtime window opens. The financial signal precedes the operational outcome by one to three quarters. That lag is the intelligence.

Layered on top: operational metrics from the asset dataset (HP set intensity, run hours between service, runtime correlations by configuration) that amplify the financial signals with field-level observation. Next week, we will start using this data to benchmark real-time performance in specific basins.

What This Means for How You Negotiate

Put it together. You have a rate benchmark: $/HP/month by HP band, basin, vendor, and fuel type, so you know whether you are above or below market before you open your mouth. You have contract timing intelligence, which tells you whether your vendor is facing renewal volume pressure in your basin right now. You have a $/MCF analysis, which tells you not whether your rate is competitive but whether your contract is sized correctly for the work it is actually doing. And you have the RRS, which tells you whether the vendor’s forward reliability posture warrants performance guarantees or an exit option.

None of these are rate conversations. Rate is the thing your vendor explained is structurally immovable, and for structural reasons they explained honestly. All of these are contract structure conversations: mobilization credits, performance guarantee provisions, escalator caps, early termination rights. The flexibility exists. It has always existed. The question is whether you showed up knowing where to find it.

The practical application works on three levels.

Benchmark the rate. Know whether your $/HP/month is above or below market for your HP band and basin before you walk into the renewal. This sets the frame.

Evaluate the vendor. Check the RRS. A vendor with deteriorating reliability metrics is a vendor you want performance guarantees from — or a vendor you want optionality to exit.

Right-size the contract. Once you know your actual compression duty, you can identify where you are paying for capacity that is not moving gas. That is not a discount conversation. It is a right-sizing conversation, one your vendor can have without touching their portfolio valuation.

The combination of understanding their model (where the off-book flexibility exists) and understanding your own position (where the optimization opportunities are) is what makes this a better partnership,

Kalibr Compression

Starting this quarter, Kalibr is launching the paid tier of Nominally Hedged, anchored by Kalibr Compression, a monthly compression intelligence brief. Each issue covers the following.

Vendor benchmark update. $/HP/month rate movements by HP band and basin across public providers and the independent market. Flagged against prior quarter and trailing four-quarter range.

Reliability Risk Score update. RRS movements for each public vendor, with interpretation of what directional changes mean for operators currently in or approaching renewal.

Contract expiration exposure map. Kalibr’s view of aggregate primary term exposure across the L48 fleet. Regional concentration flags. Where renewal windows are clustering, and which basin supply/demand dynamics are shifting.

Compression intelligence feature. One deep analysis per month. The first issue covers the $/MCF calculation: how to run it against your existing fleet, what the typical range looks like across well types and GOR profiles, and which units to target first.

The free version of Nominally Hedged continues as it has. The paid tier is for operators who want to do something with the analysis.

The Cost Structure Thesis

D&C intelligence was built for the era when drilling was where the value creation happened. That era delivered 68 on the D&C index against a 2015 baseline of 100. The gains compounded. The margins on the service side compressed. The engineers moved on to the next problem.

LOE is a decade older and largely unchanged, The same systematic intelligence applied to compression, chemicals, artificial lift, and production system design will take it lower; not because production engineers are doing their jobs poorly, but because they are doing those jobs without the tools that D&C built over fifteen years. The operators who close that gap first will have a cost structure advantage that does not depend on commodity prices, inventory quality, or how many rigs their neighbor is running. This is not a cyclical edge. It compounds.

Your vendor has been doing this math since before they picked up the phone. The only question is whether you walk into the next renewal as the operator who brought data, or the operator who confirmed what they already suspected.

Nominally Hedged goes out to a small list. If you know someone running compression negotiations this cycle — or who should be — forward it. That's the whole ask.