Nominally Hedged | The Landlord Problem: Why Your Compression Vendor Can’t Lower Your Rate

Axip Energy filed for bankruptcy in a compression bull market. That is either a cautionary tale or a tutorial. It depends on what you do with the filings.

Here is a useful theory of the oil and gas industry: it is subsurface real estate development with better PR.

You assemble acreage. You fund development. You sell production at a significant multiple to capital invested, assuming the reservoir cooperates and your completions engineer read a couple of SPE papers at HFTC rather than tapping out the happy hours. This happens underground, which is why most people miss the parallel.

Commercial real estate runs the same play above ground. You assemble land. You fund development. You sell or lease at a multiple to capital invested, assuming the market cooperates and your architect was right about the floor plate. The developer does not own the excavators. They do not own the tower cranes or the concrete batch plants. Just as the developer would never own the equipment moving dirt between the foundation and the first floor, the E&P does not own the compression moving gas between the wellhead and the sales meter. They contract for that capacity, use it, and, in theory, send it back.

The useful part is this: in both cases, the comparative advantage is finding acreage, reading the market, and funding projects. The investors backing that developer, or that E&P, are paying for geological and financial judgment. They are not paying for compressor maintenance margins or crane depreciation economics. So each industry evolves, naturally and correctly, toward a structure where every function is owned by whoever can finance it cheapest.

Now extend the analogy one step further, because this is where it gets interesting.

The compression vendor is not the developer. The compression vendor is the REIT. They own the building. They lease it to you. Their entire business model, the capital structure, the investor base, the return thresholds, the covenant calculations, is built around the assumption that the rent holds. A REIT cannot selectively cut dollars per square foot for one tenant without that conversation immediately becoming a conversation about what every other unit in the portfolio is worth. The auditors ask. The lenders ask. The covenant calculations update. What looked like a one-off accommodation is now a portfolio-wide markdown.

Compression works identically. The dollars per HP per month your vendor quotes is not a negotiating position. It is a valuation input, the number their entire asset base gets marked against. Ask them to cut it, and you have not asked for a discount. You have asked them to reprice their balance sheet.

Which means the first step in any serious compression negotiation is not asking for a lower rate. It is understanding the model well enough to know what they actually can give you, and what the accounting will and will not allow. That requires reconstructing their return thresholds, their leverage math, and the specific utilization floor below which the arithmetic stops working.

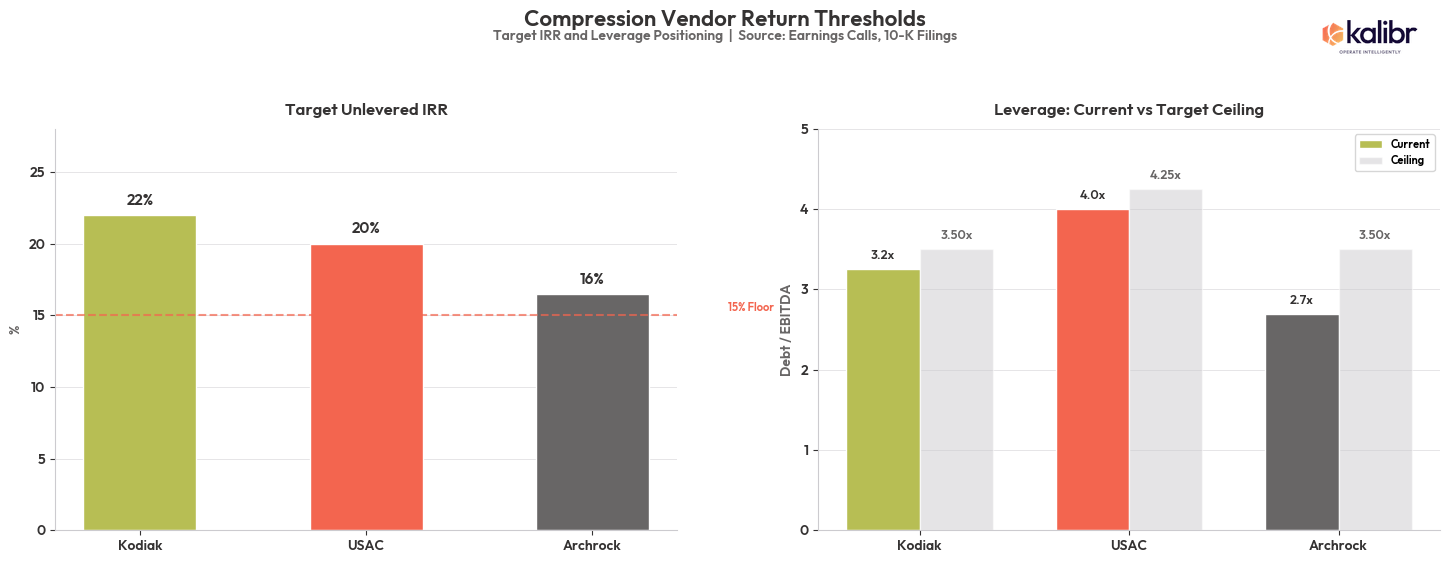

What the oilfield supply chain actually is, and almost nobody talks about it this way, is a tranched capital structure wrapped around a set of operational risks. Think of it like a CLO, except instead of slicing credit risk into senior and junior tranches, you are slicing oilfield operational risk into layers and selling each layer to the investors best positioned to hold it. The E&P equity sits at the top of the stack: reservoir risk, commodity price risk, execution risk, in exchange for the IRRs that justify the geological and financial judgment the investors are actually paying for. The compression vendor sits several tranches lower. Contracted cash flows. Hard asset collateral. Multi-year lease terms with investment-grade counterparties. Predictable maintenance cycles. This is, functionally, an infrastructure yield instrument, and it attracts infrastructure yield investors. Pension funds. Insurance companies. The same capital that buys Prologis warehouses and toll road concessions. These investors accept 12 to 15% unlevered returns because the risk profile warrants it and because their liability structures demand duration, not upside.

The tranching is elegant. The tranching is correct. Modigliani and Miller had a theorem about why vertical integration destroys value here: combining high-beta reservoir exposure with low-beta contracted equipment yield produces a cost of capital that is wrong for both businesses simultaneously. The practical version: the E&P that owns its compression fleet has confused its equity investors, annoyed its lenders, and made its CFO’s job harder, all at once.

The ecosystem is not an accident. It is the industry’s solution to a genuine capital allocation problem. And for compression vendors in particular, it has worked almost suspiciously well.

The Part Where the Vendors Start Making Embarrassing Amounts of Money

It has been a good time to own a compressor.

To understand why, you have to start with what happened to the customer. In a previous piece, we traced how E&P consolidation quietly transformed compression from a commodity rental into a critical-path service. The short version: as operators consolidated, pads got bigger, laterals got longer, and simul-frac operations demanded more horsepower delivered to a single location. The architectural decision to run gas lift, driven by capex efficiency and slimmer casing designs, locked compression into the production system the way a conveyor belt gets locked into a factory floor. Rising gas-oil ratios across maturing Permian fields deepened the dependency further. You were no longer renting a compressor. You were building your production system around one.

That shift did two things to vendor economics that do not show up immediately in the headline numbers. First, it upgraded the counterparty. The operators committing to compression contracts on large centralized facilities are not small privates running a three-well pad on a prayer. They are Devon and Diamondback and Coterra, locking in compression for drilling programs that have already been AFE’d, approved, and scheduled. Investment-grade credit risk on mission-critical equipment. The contract book got longer, the credits got better, and the embedded switching costs got higher, all at the same time.

Second, and this is the part that rarely gets written about: the supply chain collapse did not just constrain new capacity. It restructured how vendors carry risk. Caterpillar engine lead times stretched to 90 to 120 weeks at the peak, call it two years from order to delivery on a large horsepower unit. Vendors responded by requiring operators to commit to contracts before equipment was ordered. The mechanics matter here. The vendor does not pay the balloon payment to Caterpillar or the engine manufacturer until the unit sets on location, which is also when the contract starts and revenue begins. No float. No inventory carrying cost. No speculative deployment. The vendor is running a pre-sold order book against a manufacturer who holds the inventory risk.

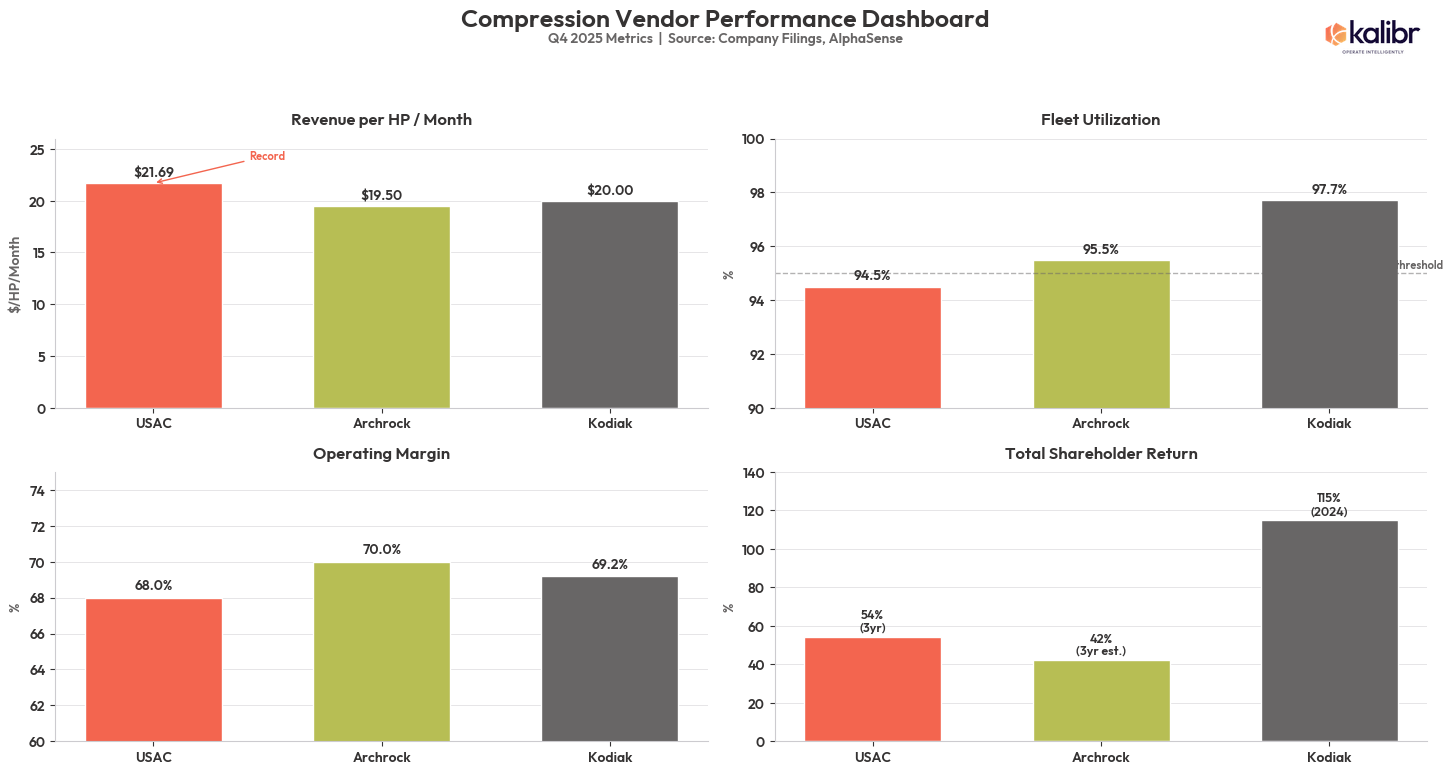

The numbers are what you get when all three of those things compound simultaneously. USAC reported revenue per horsepower per month of $21.69 in Q4 2025, a record. Archrock’s operating margins have exceeded 70% for five consecutive quarters. Kodiak’s fleet utilization sits at 97.7%, which in a capital-intensive equipment business is essentially the speed of light. You do not get meaningfully closer to full without something breaking. USAC has made 50 consecutive quarterly distributions without a cut since its IPO, returning approximately $1.9 billion to unitholders.

The bad debt figure is the one that stops the room. Over nineteen years, USAC’s write-offs have totaled 0.06% of billings. Not 6%. Zero point zero six. When your customers are investment-grade operators running production systems they cannot shut down, and your contracts were pre-sold before the equipment existed, bad debt becomes a rounding error on a rounding error.

To put that in context your CFO will appreciate: USAC’s three-year total shareholder return of 54% nearly matched the S&P 500 Value index during one of the most aggressive tech bull markets in history. Compression does not have a ChatGPT moment or a Blackwell chip launch. It has a Caterpillar 3608, a multi-year contract, and a customer who cannot turn off the gas lift without killing the well. It turns out that is a durable competitive position.

Which makes the Axip Energy Services bankruptcy filing, Southern District of Texas, February 22, 2026, genuinely interesting in a way that has nothing to do with sympathy for Energy Spectrum Capital’s limited partners.

In a market this favorable, going broke requires some effort. But here is the thing about a compression bankruptcy in a compression bull market: it is the only controlled experiment you are going to get. Every healthy vendor is running the same fundamental model, same return thresholds, same accounting logic, same structural constraints. But they are not required to show their work. Axip is. The capital structure, the return thresholds, the utilization floor below which the arithmetic stops working, the exact sequence of events that made refinancing impossible, all of it goes into the public record, sworn and filed under penalty of perjury. Most operators will read the headline and move on. That is the wrong read. The Axip filing is a tutorial on the model your vendor is running, and therefore a precise map of where the leverage actually sits when you are sitting across the table from Archrock or USAC or Kodiak at contract renewal.

The Part Where We Pull Out a Calculator

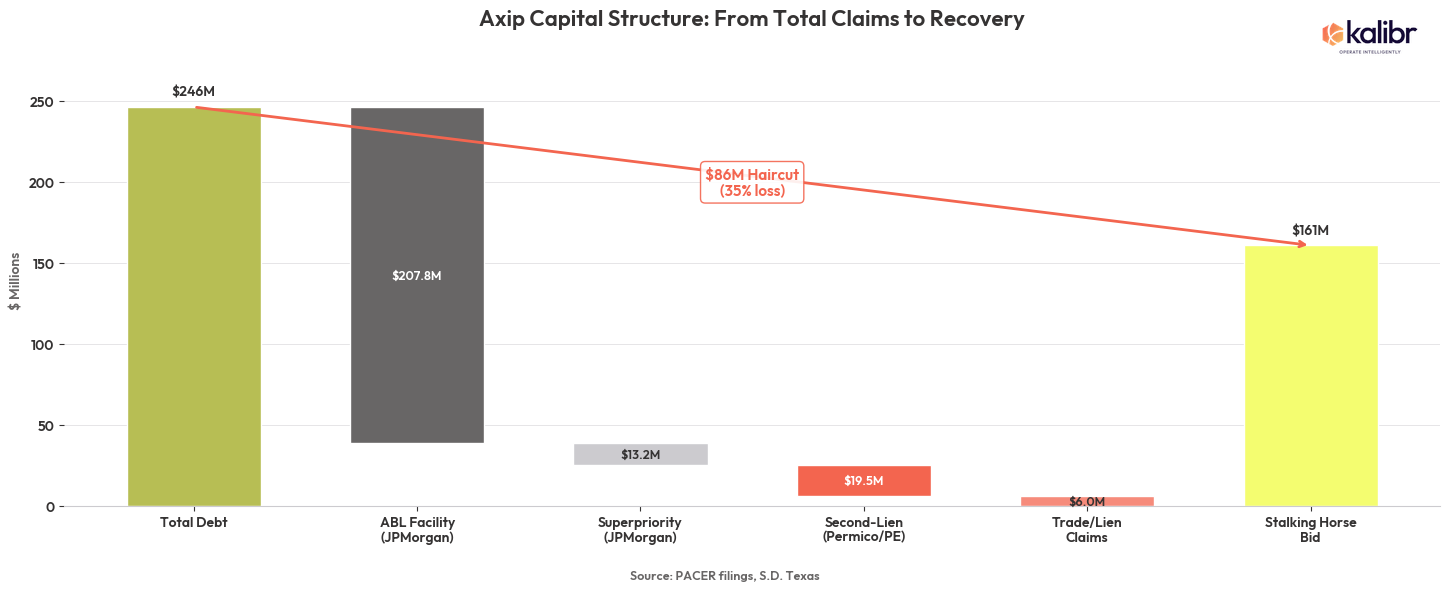

On February 22, 2026, Axip Energy Services filed for Chapter 11 in the Southern District of Texas. Energy Spectrum Capital had acquired the company in September 2022, loaded it with $240.5 million in debt, and watched the thesis fall apart in roughly three years. The stalking horse bid from Service Compression LLC came in at $161 million, 33 cents on the debt dollar.

The capital markets press wrote it up as a private equity cautionary tale. That reading is not wrong. It is just not useful.

What the filing actually is, the First Day Declaration, the capital structure schedules, the forbearance amendments, all of it sworn under penalty of perjury, is a detailed post-mortem on what the occupancy model looks like when it breaks. The REIT parallel from earlier is not decorative here. Axip did not fail because they were bad operators. They failed because vacancy crossed a threshold their debt structure could not survive. Understanding exactly how that happened tells you more about your vendor’s negotiating constraints than anything they will voluntarily disclose across a contract renewal table.

The building and the mortgage

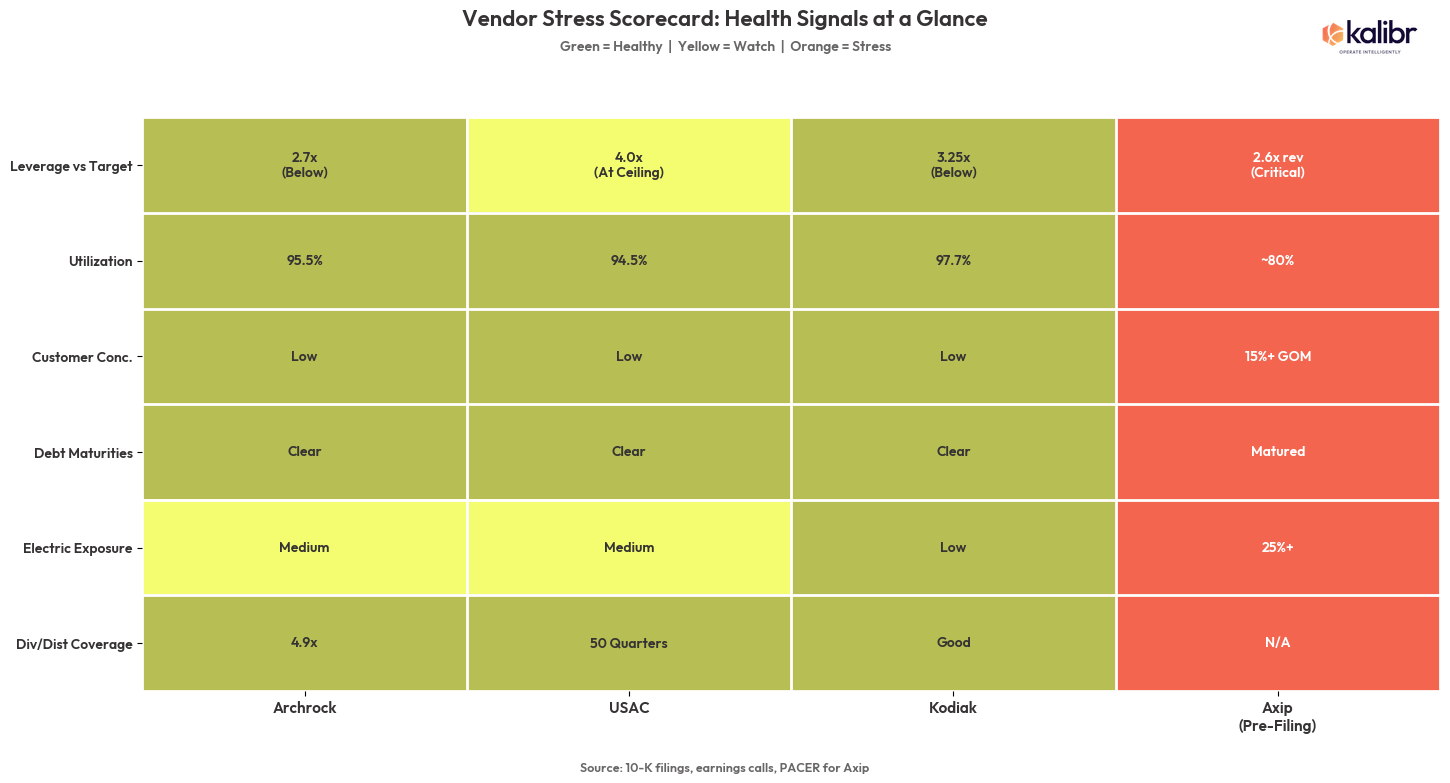

Axip operated 940 units totaling 326,070 HP across seven facilities in Texas, New Mexico, North Dakota, and the Gulf of Mexico. Against that asset base sat $240.5 million in funded debt: an ABL facility with JPMorgan Chase at $207.8 million, a superpriority tranche at $13.2 million, and a second-lien held by Permico Inc. at $19.5 million. At roughly $92 million in annual revenue, that is a 2.6x debt-to-revenue ratio. There is no margin for error in that structure. A building owner running 2.6x debt-to-rent does not survive a vacancy spike. Neither does a compression vendor.

Note the second-lien holder. Permico is PE-affiliated. Seller financing at the junior layer is a signal that the leverage could not be fully placed with third-party lenders at closing. It is not conclusive, but it is a tell worth filing away when you are evaluating vendor financial health.

The tenant that did not pay and could not leave

In Q1 2024, a major Gulf of Mexico customer filed Chapter 11 and converted to Chapter 7 liquidation. Twenty-four offshore units, over 15% of Axip’s total horsepower, were stranded overnight. The customer did not pay demobilization costs. The units could not be economically redeployed onshore. Offshore compression does not truck to the Permian. It sits.

The EBITDA impact was immediate and unrecoverable. But the more important lesson is structural: one counterparty event erased 15% of revenue on a balance sheet with no cushion to absorb it. This is the right-tail risk that the occupancy model carries silently until it does not. For operators evaluating vendors, counterparty concentration is not an abstract risk factor buried in a 10-K. It is the variable that determines how much negotiating room your vendor actually has, because a vendor carrying fragile customer exposure needs your stable, investment-grade contract more than their renewal posture suggests.

The building that needed a generator to turn the lights on

More than 25% of Axip’s fleet was electric-motor driven. On paper, a forward-looking strategic position. In practice, a mismatch between strategy and ecosystem.

Electrification is not a bad bet. Archrock and Kodiak are making similar investments, and the long-term direction of the market is not seriously in dispute. But executing an electrification strategy requires your customer base to be able to support it: reliable grid access, infrastructure buildout, power availability that matches compression demand. Axip’s customer mix could not deliver that. When grid availability failed to keep pace with deployment, customers ran generator sets to power units they were already renting, effectively paying twice for the same compression. That math accelerates the decision to return equipment considerably.

The contrast with Archrock is instructive. Archrock can pursue electrification credibly because their customer base includes operators large enough to command grid infrastructure buildout. ExxonMobil does not run generator sets. Axip’s customers did. Strategy requires ecosystem alignment, and a vendor pursuing a strategy their customer base cannot support is a vendor burning capital and absorbing returns. Which is both a risk signal and, if you are in their customer base, a leverage signal.

What the vacancy actually cost

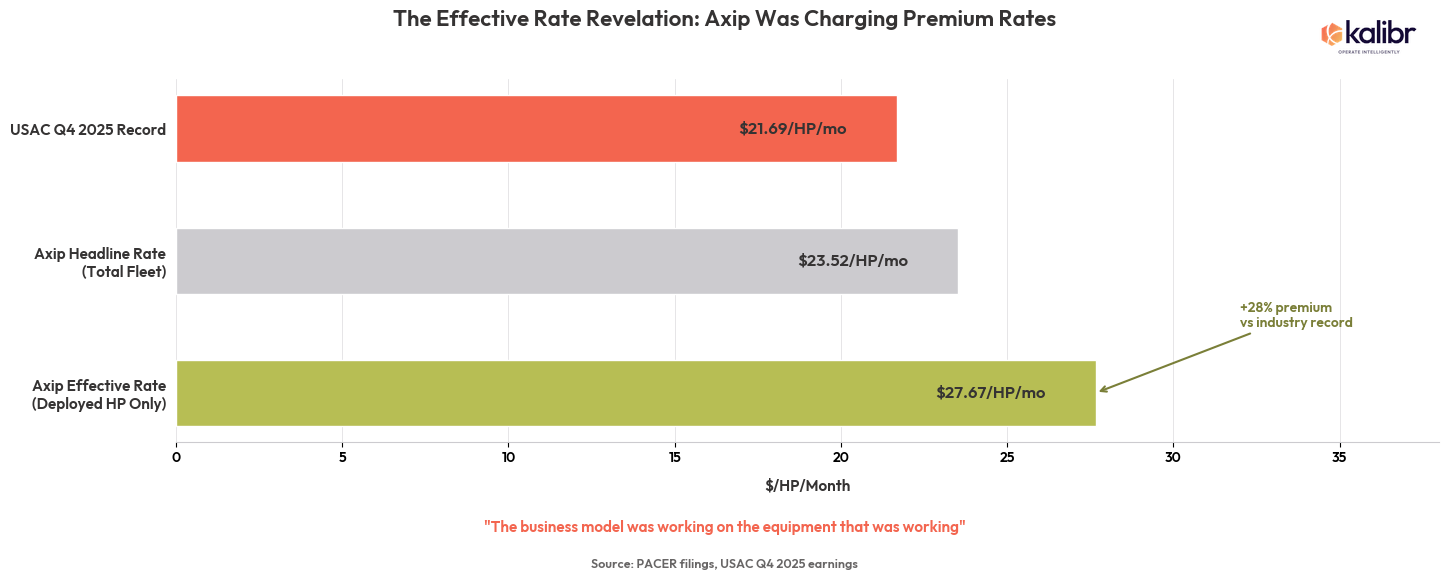

Axip’s pre-stranding revenue ran approximately $92 million annually against a fleet of 326,070 HP, an implied rate of $23.52 per HP per month across the total fleet. But 15% of that fleet was stranded and generating zero revenue. Calculate on deployed horsepower only and the effective rate was $27.67 per HP per month, higher than USAC’s record $21.69. Axip was not losing the rate war. The business model was working on the equipment that was working. What it could not survive was the vacancy.

Post-stranding, revenue dropped to approximately $78 million. Gross profit at industry-standard margins fell to roughly $51 million. Debt service alone consumed most of that. The remaining operating cost structure consumed the rest. There was no path to solvency that did not require either a significant equity injection or a buyer willing to reset the capital structure, and after six months and 85 parties contacted in an Evercore-run process, neither materialized.

What your vendor’s balance sheet is actually telling you

The Axip autopsy is not a story about bad luck or bad management. It is a demonstration of how the occupancy model fails, and therefore a precise illustration of what makes it fragile even when it appears to be working.

Three things to take away.

First, utilization is not a performance metric. It is a solvency metric. For a vendor running 4x leverage against contracted equipment cash flows, the difference between 95% and 80% utilization is the difference between distributable cash and covenant breach. The problem is that in the current market, all three majors are running 94 to 98%. The headline number does not tell you much. What matters is primary term exposure: which contracts are rolling, when, and what that does to forward utilization when the aggregate looks healthy. That is where the fragility hides. It is also where the negotiating window opens, if you know where to look. (Kalibr tracks primary term exposure at the vendor level. More on how to use that in a future piece.)

Second, counterparty concentration is a commodity exposure signal, not just a default risk flag. Consolidation has largely removed outright bankruptcy risk from the E&P customer base. Devon and Diamondback are not going Chapter 7. But concentration still matters, because it tells you what your vendor’s growth outlook is actually tied to. A vendor with a gas-heavy contract book in a weak gas price environment is a vendor whose forward EBITDA is under pressure. If you are an oil-weighted operator in the Midland Basin, you are not just a renewal. You are a hedge against the exposure that is compressing their growth outlook. That asymmetry is leverage, and it is leverage most operators never think to calculate because they are focused on their own commodity exposure, not their vendor’s. Read their 10-K customer concentration disclosures and map it against the current price environment before you walk into a renewal.

Third, know your vendor’s strategic white space and know where you sit inside it. Every vendor has edges where they are strong and edges where they are exposed. A vendor overextended into a technology or geography their customer base cannot support is a vendor absorbing execution risk that will eventually show up in your service quality or their willingness to deal. Understanding the shape of their strategy tells you where the pressure points are before they become your problem.

The practical starting point for all three is the same: model the occupancy floor. What utilization does your vendor need to service their debt at current rates, and how close are they to it? That calculation sets the realistic bands of negotiation, not what you want, but what the arithmetic will actually allow. The inputs are their cost basis, their WACC, their stated IRR targets, and their leverage structure. Archrock, USAC, and Kodiak publish most of this. What they do not publish is reconstructible from public filings. (This is what Kalibr’s market intelligence package is built around: the vendor-level economics that turn a renewal conversation from a negotiation about numbers into a negotiation about constraints.)

Once you have the floor, the last piece is understanding what form a concession can actually take. Rate cuts are a balance sheet conversation your vendor cannot have without repricing their entire portfolio. The auditors ask, the lenders ask, the covenant calculations update. But off-book accommodations are a different category entirely. Free months, mobilization credits, escalator caps, priority dispatch commitments: accounting-friendly concessions that do not touch the portfolio valuation. Understanding which category each ask falls into is the difference between a negotiation that goes somewhere and one that does not. That is where we are going next.

The Part Where We Tell You What to Do With All of This

Here is what you now know that most operators sitting across a compression renewal table do not.

The rate your vendor quoted is not a negotiating position. It is the number their entire asset base gets marked against. Ask them to cut it and you have not asked for a discount. You have asked them to call their auditors and explain why their portfolio is worth less than it was yesterday. That conversation does not happen. Not because your vendor is unreasonable. Because their accounting will not allow it. The REIT does not discount one floor of the building. The compression vendor does not discount one contract. The math is the same.

What the Axip filing gave you, and what three years of record utilization, record margins, and record distributions from the healthy vendors obscures, is a precise picture of how fragile the occupancy model actually is. One counterparty event. Fifteen percent vacancy. A debt structure with no cushion. The building empties faster than the mortgage adjusts. That fragility does not disappear because USAC is at 94.5% utilization and Archrock’s dividend coverage is 4.9 times. It goes underground. It waits. And it surfaces, quietly, in the primary term exposure of a contract book that nobody outside the vendor’s treasury department is tracking.

Until now, anyway.

Build the model. It does not have to be perfect. It has to be better than walking in blind, which is a low bar to clear. Use their public filings. Use their stated IRR targets and leverage ratios and cost of capital disclosures. Back into the utilization floor below which the arithmetic stops working. Map their counterparty concentration against the current commodity price environment and ask yourself whose problem you are solving by signing a renewal. That is your band. That is the realistic range of what this negotiation can produce, before anyone has said a word about rates.

Then, and this is the part that turns a framework into a result, look for the intelligence that tells you where you sit inside that band. Primary term exposure. Counterparty concentration. Strategic overextension. The signals that tell you whether you are negotiating from the middle of their comfort zone or the edge of it. (Kalibr tracks this at the vendor level, if you would rather not spend a weekend with a Bloomberg terminal and three years of 10-K filings. Either way, the inputs exist.)

What you will find, once you have done this work, is that the negotiation looks different than it did before. Not because the vendor suddenly became generous. Because you stopped asking for things the accounting will not allow and started asking for things it will. There is a whole category of concessions that compress vendor economics without touching the portfolio valuation, concessions that are, in some cases, worth more to an E&P operation than a rate cut would have been anyway.

That is next week.

But here is the thing to sit with until then. Every sophisticated commercial real estate tenant knows that you do not walk into a lease renewal and ask the landlord to reprice the building. You ask for three months free rent, a tenant improvement allowance, and a right of first refusal on the suite next door. The landlord says yes, the portfolio valuation stays intact, and both parties leave the table having gotten something real. The dollars per square foot never moved. Nobody’s auditors had an uncomfortable morning.

Your compression vendor is the landlord. You have been asking them to reprice the building. You need to be asking about the tenant improvement allowance. More to come.

Nominally Hedged goes out to a small list. If you know someone running compression negotiations this cycle — or who should be — forward it. That's the whole ask.