Nominally Hedged: The Denominator

Harold Hotelling’s 95-year-old theory, Devon’s $2.63 billion answer, and the four strategies left when the rock runs out.

There is something underground. It has value today. It will have value tomorrow. The only question is: which value is higher?

If you sell it today and put the money in a savings account, you earn the interest rate. If you leave it in the ground and sell it next year, you earn whatever the market decides that thing appreciates by over the next twelve months. When the interest rate wins, you extract. When the ground wins, you hold.

In 1931, an economist named Harold Hotelling wrote a paper that formalized this logic for exhaustible resources. The paper is 28 pages of differential equations and it boils down to one sentence: the price of a finite resource in the ground should rise at the rate of interest, because if it rose faster, nobody would extract, and if it rose slower, everyone would extract today. It is the kind of insight that seems obvious once someone states it, which is the hallmark of work that is genuinely important.

For 95 years, the American oil industry operated as though Hotelling was wrong. Not because the math was bad, but because the premise felt irrelevant. There was always more rock. The Spraberry led to the Barnett, the Barnett led to the Marcellus, the Marcellus led to the Wolfcamp, and somewhere in there we learned how to drill sideways and frack the hell out of tight formations that a decade earlier would have been written off as source rock. The denominator (drillable Tier 1 locations) felt infinite. So the industry spent a decade perfecting the numerator: returns per well, free cash flow margins, capital discipline, DSU optimization, all the things that make quarterly earnings presentations look crisp and Wall Street analysts say nice things.

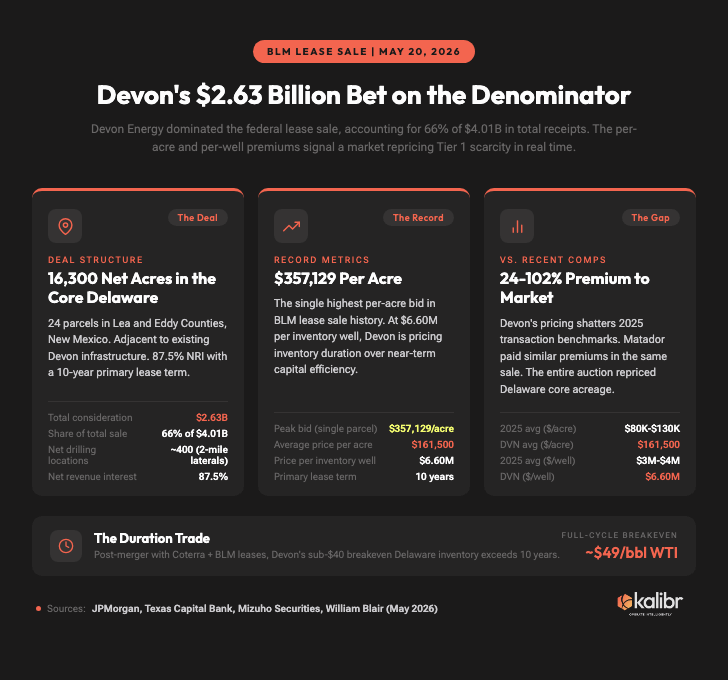

On May 20th, Devon Energy paid $357,129 for a single acre of undeveloped New Mexico desert.

And Hotelling’s Rule arrived in the Permian Basin.

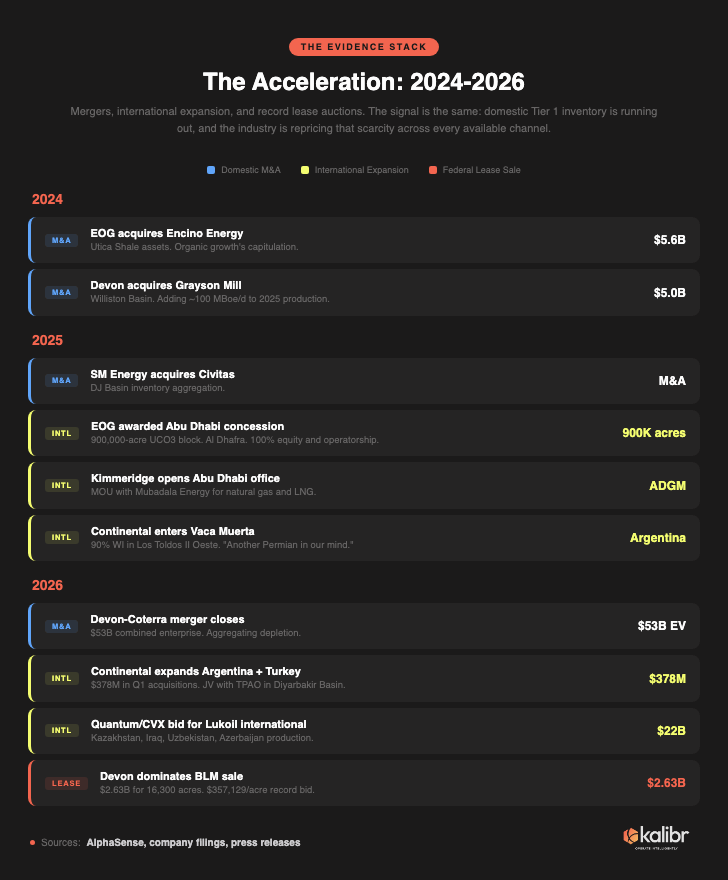

I have been writing about this for a year. In January, I called the Devon-Coterra merger what it was: not a growth story, but an exercise in aggregating depletion. In June 2025, I watched EOG, the company that built its entire identity around organic growth, spend $5.6 billion on Encino because the drill bit alone could no longer solve the problem. This is the third article in a series I did not plan to write. The first two were about the diagnosis. This one is about the prognosis.

The Part Where Devon Buys the Desert

The Bureau of Land Management held a federal onshore oil and gas lease sale on May 20, 2026. The total receipts were $4.01 billion. Devon Energy accounted for $2.63 billion of that. Sixty-six percent.

The company secured 24 parcels covering approximately 16,300 net undeveloped acres in the core of the Delaware Basin, specifically in Lea and Eddy Counties, New Mexico. The acreage adds roughly 400 net drilling locations normalized to two-mile laterals at an average cost of approximately $161,500 per acre and $6.60 million per inventory well. The net revenue interest is 87.5% (the federal royalty is 12.5%, which is actually more favorable than typical state or fee leases in the region). The primary lease term is ten years. The acreage is directly adjacent to Devon’s existing infrastructure, which means the company can plug these locations into its current midstream facilities without building from scratch.

Those are the mechanical details. Here are the ones that matter.

Recent Permian transactions have priced at $80,000 to $130,000 per acre and $3 to $4 million per well. Devon paid $161,500 per acre on average, with one parcel clearing $357,129. That is a 24% to 102% premium to the 2025 average, depending on which comp you use. And Devon was not alone. Matador Resources spent $1.14 billion in the same sale for 5,154 acres at an average of $221,700 per acre, including one bid of $330,002 per acre for a single 1,000-acre tract. Federal Abstract Company paid $221,800 per acre for six parcels. The entire sale priced at a level that would have been unthinkable 18 months ago.

Here is where it gets interesting. Mizuho ran Devon’s new acreage through its ARCHIE model and found that the geology is Tier 1 (some of the most productive rock in the Delaware), but the full-cycle economics are Tier 2 because the acquisition cost lifts the breakeven by approximately 30%, to roughly $49 per barrel WTI. The rock is world-class. The purchase price turns it into something that merely generates very good returns instead of exceptional ones.

(This is the kind of distinction that matters enormously if you are underwriting the asset and not at all if you are writing the press release.)

But here is what Devon’s management is actually solving for. Prior to this acquisition and the Coterra merger, investors had flagged the duration of Devon’s top-tier inventory as a concern. Post-merger, post-BLM sale, Devon’s sub-$40 breakeven Delaware inventory now exceeds ten years. That is not a growth investment. That is a duration investment. Devon did not buy rock to drill faster. Devon bought rock to drill *longer*.

And that, if you have been paying attention, is Hotelling.

The Part Where the Evidence Stacks Up

Devon’s BLM bid is not an outlier. It is the latest and most expensive data point on a trend line that has been building for two years. And if you stack the signals chronologically, the pattern is less of a trend and more of an acceleration.

Start with the mergers. Devon and Coterra combined to create a $53 billion enterprise. SM Energy acquired Civitas. EOG bought Encino for $5.6 billion. In each case, the stated rationale was some version of “synergies” and “scale,” and in each case the actual rationale was inventory duration. You do not merge two depleting portfolios to grow. You merge them to extend the runway.

Then the international moves. Continental Resources, the company Harold Hamm built in the Bakken, acquired a 90% working interest in Argentina’s Vaca Muerta shale in November 2025 and followed it with a 20% non-operated stake in four additional blocks with Pan American Energy in January 2026, spending $378.3 million on acquisitions in Q1 2026 alone. Continental’s CEO Doug Lawler compared Vaca Muerta directly to the Permian: “It could very easily be another Permian in our mind.” He added a line that should make every domestic operator uncomfortable: “The rock doesn’t know what country it’s in.”

EOG, which I wrote about in June 2025 as the bellwether for organic growth’s capitulation, was awarded a 900,000-acre unconventional oil concession in Abu Dhabi’s Al Dhafra region in May 2025 (100% equity and operatorship during the three-year appraisal phase) and established a tight gas sand joint venture in Bahrain. Drilling commenced in Q3 2025. The company that defined “drill it, earn it, repeat” is now drilling it in the Arabian Gulf.

Kimmeridge Capital Management, one of the most prominent US E&P-focused private equity shops, opened a dedicated office in Abu Dhabi in May 2025 and signed an MOU with Mubadala Energy for natural gas and LNG investments. Quantum Energy Partners partnered with Chevron on a joint bid for Lukoil’s non-Russian international assets, valued at approximately $22 billion, spanning production in Kazakhstan, Iraq, Uzbekistan, and Azerbaijan.

And then there is Diamondback. Kaes Van’t Hof, during the Q4 2025 earnings call in February 2026, said it plainly: “Listen, we’re in a depleting business, right? And we think about inventory every day.” Travis Stice had said it even more bluntly in Q2 2024: “We’re running out of Tier 1 inventory.” By Q1 2026, Van’t Hof was writing in the stockholder letter that the light had turned green on growth, because “the operator with the best inventory quality and the lowest cost structure with the longest inventory depth probably has the right to grow organically.”

Probably. An interesting word to put in a stockholder letter. Probably has the right to grow. That is what passes for confidence when the denominator is going to zero.

There is a 19th-century economist named William Stanley Jevons who could have told you this was coming. In 1865, Jevons observed that as steam engines became more efficient, England used *more* coal, not less. Efficiency made the resource cheaper per unit of work, which made more activities profitable, which increased total consumption. The shale revolution followed Jevons’ script perfectly: longer laterals, tighter spacing, optimized completions, better capital efficiency per well, all of which accelerated the rate at which Tier 1 inventory got consumed. The industry optimized its way into scarcity.

But is there a way to measure this structurally, not just anecdotally?

The team at Novi Intelligence published a paper in April titled “From Reserves to Returns” that quantifies it with a precision I am not going to replicate here, and that I’d recommend to any E&P executive or investor who hasn’t read it. The core metric is what they call the Recycle Ratio: operating cash flow per barrel divided by organic proved developed finding and development cost per barrel. It tells you how much cash you generate from your existing production relative to what it costs to replace that production through the drill bit. It is, fundamentally, a replacement metric.

And their key finding is uncomfortable for anyone still running the capital efficiency playbook: the number one driver of variation in Recycle Ratio between operators is not operating cost structure, not capex per well, not price realizations. It is the quality of the underlying rock. The 3-year weighted average Recycle Ratio for the US E&P peer group fell from 213% in the 2022-2024 period to 190% in 2023-2025. All three companies that were acquired and taken off the board in 2025 (HES, CIVI, VTLE) were in the bottom quartile of Recycle Ratio performance.

The market is selecting for rock quality. And rock quality is a function of inventory. Which brings us back to the denominator.

The Part Where the Industry Forks

For ten years, every E&P in America ran essentially the same playbook. Optimize capital efficiency. Return cash to shareholders. Grow modestly, if at all. The playbook worked because the underlying assumption was true: Tier 1 inventory is abundant enough that the only question is how efficiently you can convert it into free cash flow.

Devon’s $2.63 billion BLM bid is the market telling you that assumption has expired.

So what do you do when the essence of your business is running out?

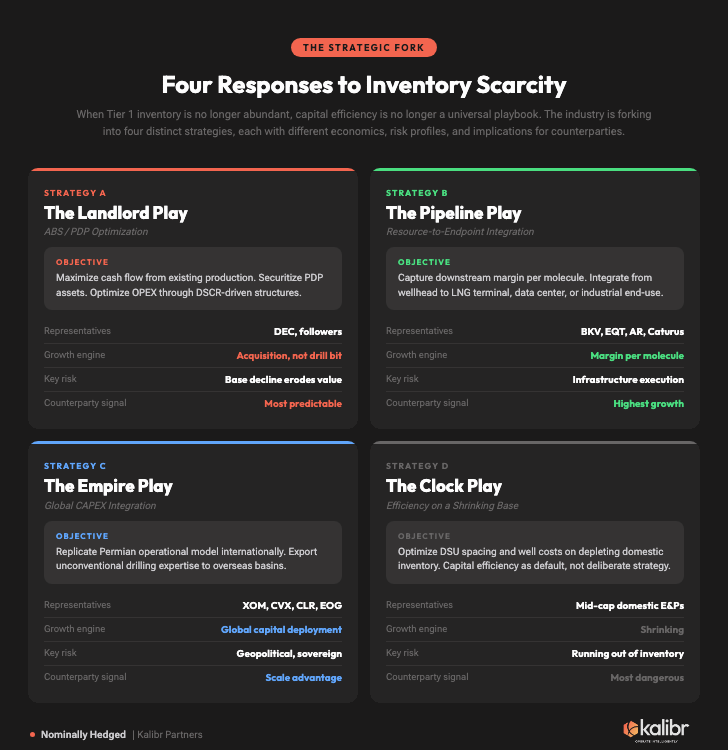

I think the answer is that there is no longer *one* answer. The industry is forking, and the strategies are divergent, not points on a spectrum. Four distinct playbooks are emerging, and understanding which one your company (or your counterparty) is pursuing is, I would argue, the single most important question in E&P right now.

The Landlord Play.

Some operators have accepted that organic growth is over and are restructuring around maximizing cash flow from existing production. I wrote about this in May with the ABS architecture piece: Diversified Energy has built a machine that acquires PDP assets, securitizes them into bankruptcy-remote SPVs, and generates management equity through OPEX discipline rather than CAPEX growth. The structure rewards cost control with a leverage that would make a hedge fund blush. This is early innings. Cumulative upstream ABS issuance has reached roughly $20 billion. Annual volume scaled from $0.5 billion in 2020 to $4.3 billion in 2025. The economics are straightforward: 6.0% to 6.5% ABS coupon versus 8% to 10% high-yield corporate debt, non-recourse, no borrowing base redetermination. For operators who are honest about the denominator, the Landlord Play is not a retreat. It is a different objective function entirely. But it requires a new operational playbook: optimizing OPEX like you have never optimized it before, because every dollar saved flows directly to equity through the DSCR waterfall.

The Pipeline Play.

BKV, EQT, Antero, Caturus, Commonwealth LNG. These companies are vertically integrating from the wellhead to the demand point: LNG export terminals, data center power generation, industrial end-use. The logic is straightforward for gas (you can contract directly with the consumer of your product) and much harder for oil (the refining intermediary fragments the value chain). Antero’s firm transport contracts for LNG, EQT’s play into data center gas supply, BKV’s direct gas-to-power strategy, Commonwealth’s integrated LNG development: these are all different expressions of the same thesis. If you cannot grow the denominator (inventory), grow the numerator (margin per molecule) by capturing value further downstream. More compression per molecule, longer value chain, higher margin.

The Empire Play.

ExxonMobil, Chevron, and to a lesser extent the companies following Continental’s lead into Argentina and the Middle East. These operators are replicating the Permian operational model internationally: applying unconventional drilling and completion techniques to overseas basins where the geology is promising but the technology has not arrived. Lawler’s line, “the rock doesn’t know what country it’s in,” is the thesis. EOG in Abu Dhabi, Continental in Vaca Muerta and Turkey (where early estimates suggest 6 billion barrels of oil and 12 to 20 Tcf of gas in the Diyarbakir Basin alone), Quantum and Chevron bidding $22 billion for Lukoil’s international portfolio. The advantage here is not domestic inventory. It is the ability to deploy capital efficiency techniques, the very skills honed over the last decade, at global scale.

The Clock Play.

Everyone else. Companies that are still optimizing DSU spacing and well costs on a shrinking domestic inventory base. Capital efficiency is the right answer to a different question. If your drilling locations are 15% less productive than last year’s locations (and the Delaware Basin-wide data says they are declining 6% annually), then a 5% improvement in well costs is not solving the problem. It is slowing the rate at which the problem gets worse.

Optimizing the font on a resume when the job no longer exists.

I am not saying capital efficiency is irrelevant. Diamondback, with its $550-per-lateral-foot well costs and sub-$40 breakeven inventory stretching twelve years, has earned the right to run the efficiency playbook because it solved the denominator first. The question for everyone else is whether they are running the same playbook because it is the right strategy, or because it is the only one they know.

What This Means

For operating teams: the first question is not “how do we drill more efficiently?” It is “which strategy are we actually pursuing, and does our capital allocation reflect it?” If you are running the Landlord Play, your compression and service contracts should be structured for OPEX stability, not CAPEX flexibility. If you are running the Pipeline Play, gathering and processing infrastructure is not a cost center; it is a strategic asset. If you are running the Clock Play and have not yet asked your board which of the other three you are transitioning toward, that conversation is overdue.

For service providers (and this includes compression, which is where Kalibr lives): the strategy fork changes your counterparty risk profile fundamentally. Landlord operators are the most predictable counterparties: cost-disciplined, DSCR-driven, stable contract structures. Pipeline operators are your highest-growth counterparties: more infrastructure per molecule, longer value chains, expanding service needs. Clock operators are the most dangerous counterparties, because their business models have not yet adapted to inventory scarcity, which means their capital allocation is the least predictable. Understanding which strategy your counterparty is pursuing is the first step in any negotiation. Everything else is details.

The theory says that the rational response to a depleting finite resource is for its in-ground value to rise until extraction becomes uneconomical or the market finds a substitute. For 95 years, the American oil industry dodged the second half of that prediction by finding new plays. The plays are running out.

Devon’s bid is not irrational. It is not desperation. It is the market pricing what Hotelling described on paper in 1931, repriced in real time, on 16,300 acres of New Mexico desert.

The numerator was never the problem.

The denominator was always the constraint.

Devon just paid $2.63 billion to extend it.

The question for everyone else is simpler. And harder.

What are you going to drill?

Nominally Hedged goes out to a small list. If you know someone thinking about improving sales / lowering CAPEX and OPEX — or who should be — forward it. That's the whole ask.