Nominally Hedged | The Capital Stack Is The Counterparty

Blue Owl’s liquidity problem, David Bowie’s bond portfolio, and the financing structure quietly reshaping how oil and gas assets get bought, sold, and operated.

The way institutional money found its way into risky corporate loans over the past five years was through private credit funds. The way private credit funds kept that money was by not giving it back.

This is not a criticism. It is a business model. David Einhorn figured this out at Greenlight Capital back in 2018, when his investors wanted to leave and he said (I am paraphrasing) no. The investors complained to the Wall Street Journal. Einhorn kept the money (To be clear - if your investors are complaining to the press about how onerous your liquidity terms are, you made the right call on the liquidity terms).

Private credit scaled this insight to $2.1 trillion. The pitch was elegant: we raise long-term locked-up capital, we lend it long-term to borrowers, and because the money is locked up, we cannot be forced to sell assets at the worst possible moment. We are not a bank. We are not runnable. Sleep well.

Then Blue Owl’s investors stopped sleeping well.

In February 2026, Blue Owl permanently gated redemptions on its $1.6 billion OBDC II retail vehicle after withdrawal requests surged 200%. The firm sold $1.4 billion in loans at 99.7 cents on the dollar to CalPERS, OMERS, BC Investment Management, and (notably) its own insurance arm, Kuvare. Blue Owl’s co-president, Craig Packer, went on CNBC and said: “We’re not halting redemptions, we’re just changing the form, and if anything, we’re accelerating redemptions.”

One way to read that sentence is that Blue Owl found a creative solution to a liquidity problem. Another way to read it is that the structural run-proofing that justified the entire asset class is being tested, and the test is producing sentences like that one.

Blue Owl was not alone. BlackRock TCP Capital reported a 19% NAV decline in Q4 2025. Blackstone’s BCRED faced $3.8 billion in redemptions (7.9% of total assets) in Q1 2026. Moody’s revised its entire BDC sector outlook to negative. Payment-in-kind interest hit 12.8% across BDCs. Median debt-to-EBITDA ratios in private credit climbed from 5.2x in 2020 to 6.5x. Portfolios are estimated to be 85% covenant-lite.

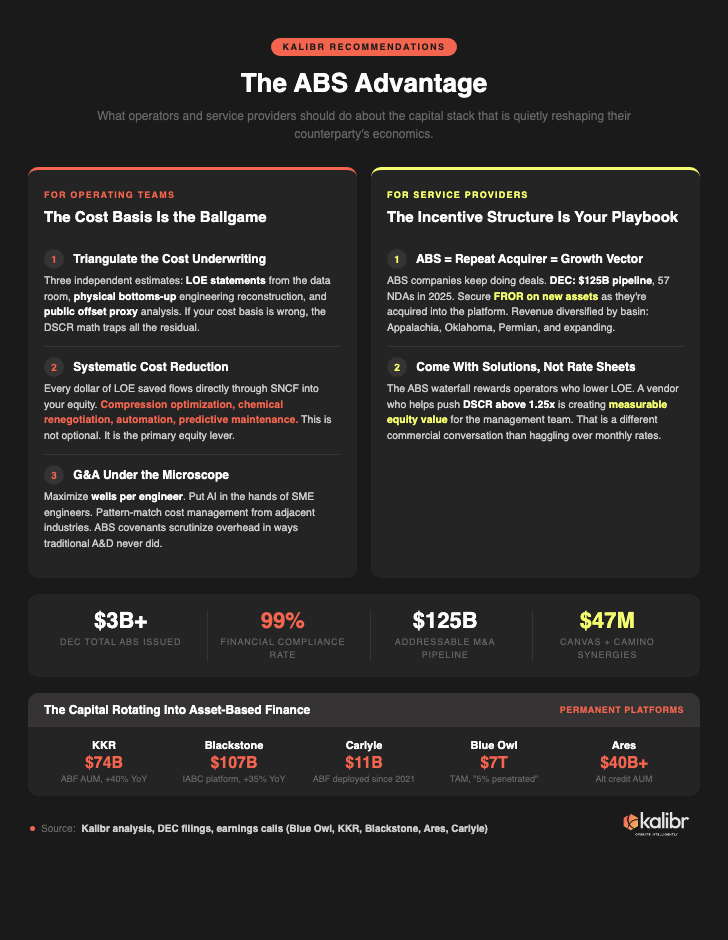

And so $543 billion in undeployed private credit capital needs somewhere to go. Blue Owl’s own management described the destination: asset-based finance, which they called “a $7 trillion market only 5% penetrated by private solutions today.” KKR scaled its ABF book to $74 billion (40% year-over-year growth). Blackstone’s infrastructure and asset-based credit platform hit $107 billion (35% growth). Ares, Apollo, Carlyle: all building permanent platforms to deploy capital into hard-asset-backed structures.

The rotation is not subtle. And one of its most interesting destinations is a corner of the oil and gas capital markets that almost no one outside of structured finance is paying attention to.

The Thing About Cash Flows

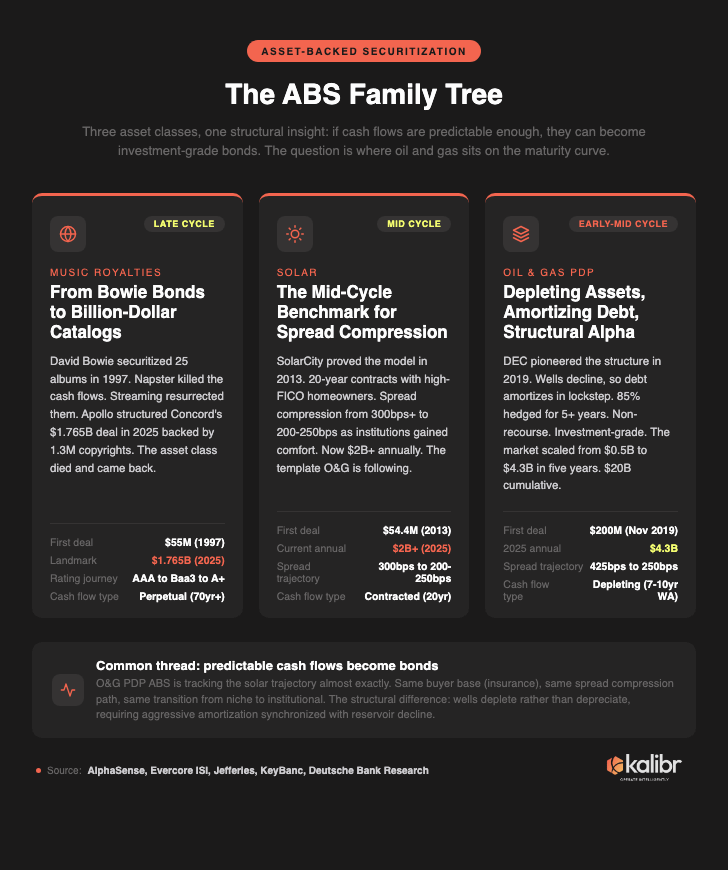

If you have seen *The Big Short* (and if you are reading this newsletter, the probability is high), you know the basic architecture. An asset-backed security is what happens when something throws off cash predictably enough that an investment bank can package those cash flows into a bond, get a ratings agency to bless it, and sell it to an insurance company that needs yield.

The “something” can be almost anything. Mortgages, obviously (that one went well). Music royalties: David Bowie securitized 25 of his pre-1990 albums in 1997 for $55 million at a 7.9% coupon with a AAA rating. Then Napster arrived, the cash flows evaporated, Moody’s downgraded the bonds to Baa3 (one notch above junk), and the music ABS market went dormant for a decade. Then streaming happened, consumption patterns stabilized, and Apollo structured a $1.765 billion securitization for Concord Music in 2025 backed by 1.3 million copyrights (including catalogs from The Beatles to Taylor Swift), achieving an A+ rating from KBRA. The asset class came back from the dead because the underlying cash flows became predictable again.

Aircraft leases. The $4 billion Airplanes Group transaction in 1996 was the largest ABS deal ever completed at the time. By 2025, the market produced 16 transactions totaling $9.5 billion. Solar panels: SolarCity issued the first solar ABS in 2013 ($54.4 million, BBB+, 4.8% coupon). The sector now clears over $2 billion annually. Railcar leases. Trade receivables. Auto loans. Equipment finance.

And now: proved developed producing (PDP) oil and gas wells.

The structure is more elegant than it sounds. An operator transfers PDP assets into a bankruptcy-remote special purpose vehicle via a true sale, which legally isolates the cash flows from the parent company’s credit risk. The SPV issues monthly-pay amortizing notes with weighted-average lives of 7 to 10 years (legal finals out to 2037-2044), sculpted to mirror the natural production decline curve of the underlying wells. The issuer hedges 80% to 95% of expected production for five to eight years, which transforms volatile hydrocarbon revenue into something that looks, to a fixed-income investor, remarkably like a mortgage payment.

The waterfall is strict: taxes and LOE first, then hedge settlements, then senior interest and scheduled principal, then reserve top-ups, then junior tranches, then (and only then) residual equity to the management team. Performance triggers tied to debt service coverage ratios, loan-to-value, and production tracking tests accelerate amortization if things deteriorate. The structure does not trust anyone. That is the point.

Where Oil and Gas Sits

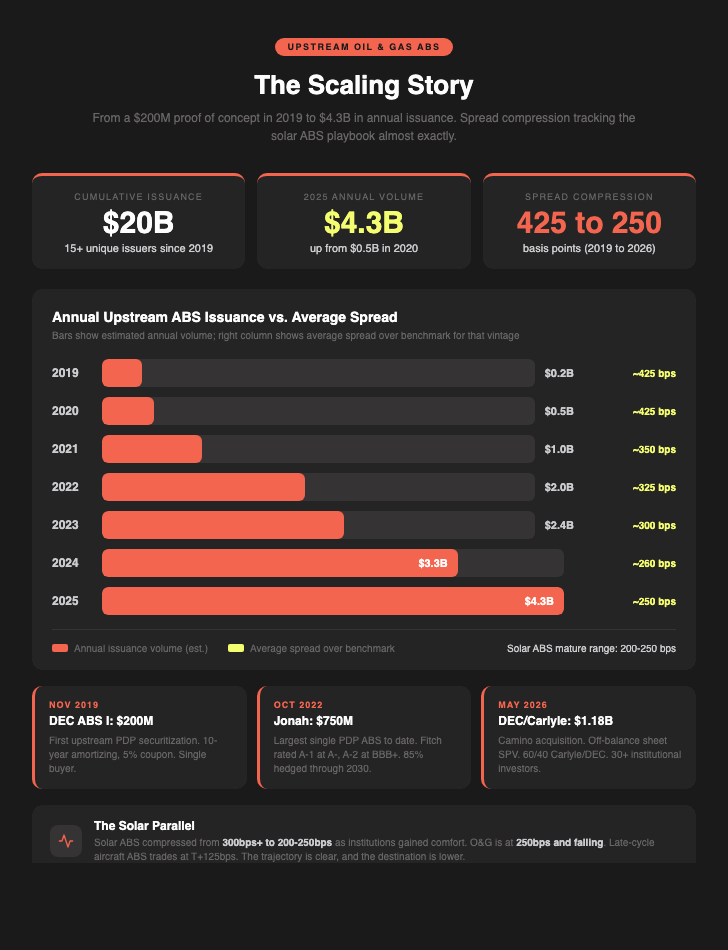

Diversified Energy Company executed the first upstream ABS in November 2019: a $200 million, 10-year amortizing note with a 5% coupon. It was a proof of concept. Six years later, DEC has issued over $3 billion in ABS notes, maintains 85% rolling hedge protection on a five-year basis, operates at a 10% base decline rate with a gas breakeven of $1.80 to $2.00/mcf, and carries a 99% financial compliance track record across its securitized portfolio.

The market followed. Jonah Energy has completed seven issuances generating over $3 billion in total proceeds, including the largest single PDP securitization to date ($750 million, October 2022). Cumulative upstream ABS issuance has reached approximately $20 billion across more than 15 issuers. Annual volume scaled from $0.5 billion in 2020 to $4.3 billion in 2025.

The spread compression tells you where the market is on the maturity curve. DEC’s inaugural deals (2019-2020) priced at approximately 425 basis points over benchmark. The multi-tranche structures from 2021 to 2023 came in around 325 basis points. The broadly marketed variable funding notes from 2024 to 2026 are clearing at roughly 250 basis points. If that trajectory looks familiar, it should. Solar ABS followed almost exactly the same path: early proof-of-concept deals pricing above 300 basis points, compressing to 200-250 basis points as institutional comfort deepened. Late-cycle aircraft ABS trades at approximately T+125 basis points. Oil and gas is early-to-mid-cycle, tracking the solar playbook.

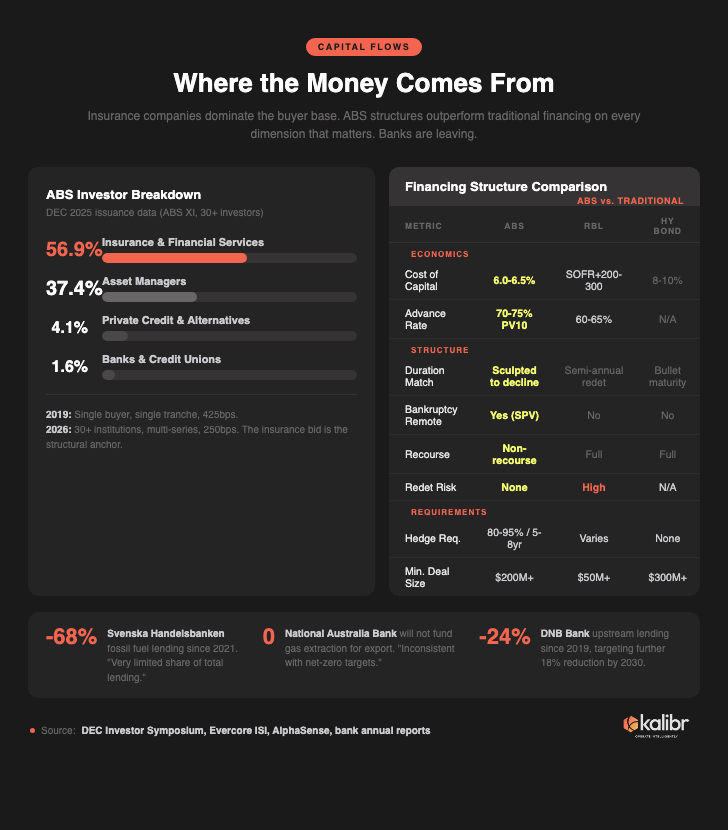

The economics are straightforward. ABS A-tranche coupons price at 6.0% to 6.5%, versus 8% to 10% for high-yield corporate debt. Advance rates run 70% to 75% of PV-10 value, compared to 60% to 65% for traditional reserve-based lending. The debt is non-recourse. There is no semi-annual borrowing base redetermination. No refinancing cliff.

The buyer base has institutionalized rapidly. Insurance and financial services firms now represent 56.9% of allocated capital. Asset managers account for 37.4%. Private credit and alternative funds hold 4.1%. Banks: 1.6%. The insurance bid is the structural anchor, driven by the same thing that drives every insurance allocation decision: long-duration, investment-grade, self-amortizing cash flows that match multi-decade liability profiles. DEC’s most recent issuance (ABS XI) attracted over 30 unique institutional investors. In 2019, the first deal went to a single buyer.

The Management Math

Here is the part that matters if you are an operator, a service provider, or anyone who negotiates with either.

ABS entities are not normal counterparties. The financial structure creates a management team that is economically levered to operating cost discipline in a way that traditional E&P equity holders or PE-backed operators simply are not.

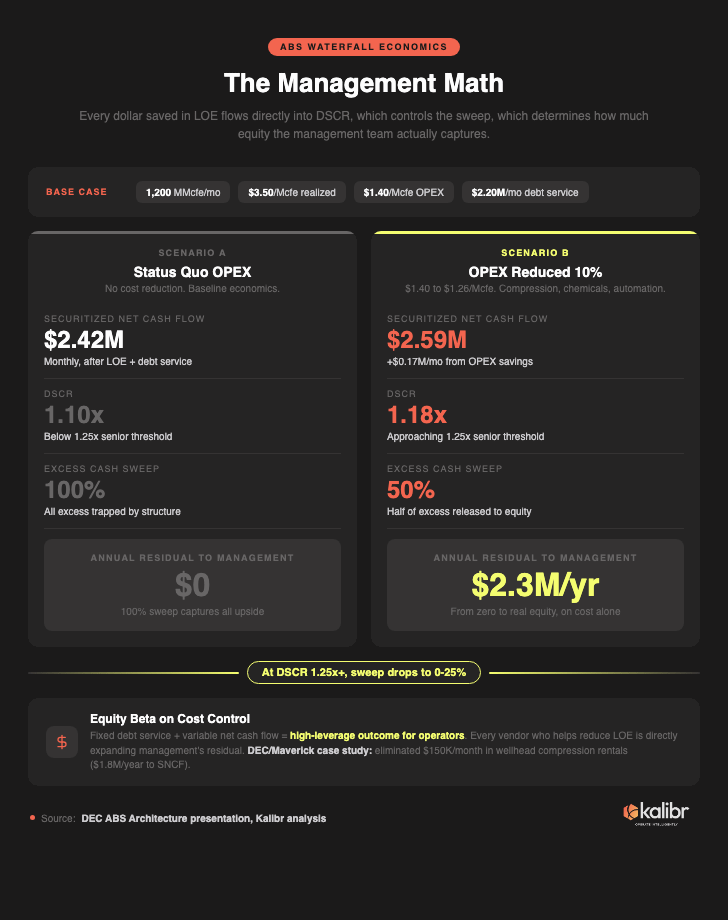

The mechanism: every dollar saved in lease operating expense flows directly into securitized net cash flow, which raises the debt service coverage ratio. Higher DSCR lowers the mandatory cash sweep percentage, which releases trapped cash to the management team as residual equity distributions.

Take a base case: 1,200 MMcfe/month production, $3.50/Mcfe realized price (with hedges), $1.40/Mcfe base OPEX, $2.20 million/month debt service. Securitized net cash flow: $2.42 million. DSCR: 1.10x. At that level, the structure mandates a 100% excess cash sweep. Residual to management: zero.

Now reduce OPEX by 10%. SNCF increases by roughly $0.17 million per month. DSCR rises to 1.18x. The sweep drops from 100% to 50%. Residual to management: $2.3 million per year. And if you can nudge DSCR to 1.25x or above, sweep rates fall to 0% to 25%, and the equity take expands dramatically.

This is something close to equity beta on cost control. Fixed debt service plus variable net cash flow equals a high-leverage outcome for the people running the assets.

DEC’s acquisition of Camino Natural Resources (announced May 2026, $1.18 billion) demonstrates the programmatic model. DEC contributed $210 million from its credit facility. Carlyle took a 60% majority equity interest in the SPV. DEC retained 40%, plus 100% of the undeveloped acreage, plus operating and management fees. The ABS debt is deconsolidated from DEC’s balance sheet. DEC retired $92 million in outstanding ABS principal in Q1 2026 alone. The machine acquires, securitizes, optimizes, builds equity, and repeats. In 2025, DEC signed 57 NDAs, submitted 24 bids, and closed one deal. The pipeline is $125 billion.

What This Means

For operating teams, the implications are structural, not incremental.

Cost underwriting becomes the ballgame. I know from experience on the A&D side that fixed and variable cost analysis typically gets a quick pass using the LOE statements in the virtual data room. Most of the analytical energy goes to PUDs and alpha created at the bit. That approach made sense when the capital structure rewarded production growth. In an ABS structure, where management’s economics are a direct function of DSCR, the cost basis is the single most important variable in the deal model. Get it wrong and the sweep traps all the residual.

Kalibr recommends a triangulation method: LOE statements from the data room, a physical-asset-based bottoms-up reconstruction of the cost structure (I am biased here, since this is what I have invested to build, but I also think it is correct), and public offset proxy analysis to reduce error. Three independent estimates. Converge on a defensible number. The legal and advisory fees on these deals are substantial, so the deal size needs to justify the aggregate cost. You cannot afford to get the underwriting wrong on a structure where every dollar of OPEX error compounds through the waterfall.

Systematic cost reduction is not optional. It is the primary equity lever. The only way management makes money in an ABS structure is driving cost out of the system. Every improvement in LOE (compression optimization, chemical renegotiation, automation, predictive maintenance) reduces the sweep and waterfalls more cash to management. DEC demonstrated this when it integrated Maverick Natural Resources: the team identified and eliminated $150,000 per month in wellhead compression rentals by leveraging existing Diversified infrastructure. That is $1.8 million per year, flowing directly through SNCF into management’s residual.

G&A is under a microscope. These deals are scrutinizing overhead in ways traditional A&D never did. The question is: how many wells can I run per engineer while holding to the cost discipline above? This is where AI belongs. Not as a buzzword in an investor deck. In the hands of subject matter expert engineers who can use it to monitor more wells, pattern-match best practices from adjacent industries, and reduce the technical headcount required to operate a given portfolio. Fewer engineers running more wells, armed with better tools. That is the structure this capital stack rewards.

For service providers, the calculus is different but equally clear.

Understand the growth vector. Companies embracing ABS will keep doing deals. It is purely a cost-of-capital game: once you have proven the structure works, you acquire more assets into the platform. DEC sees $125 billion in actionable deal flow over the next five years. Identifying these companies early and securing first right of refusal on new assets gives you a revenue stream that is diversified by basin (Appalachia, Oklahoma, Permian, with Bakken, DJ, and Eagle Ford on the horizon) and anchored to a counterparty with structural incentives to maintain the relationship.

Understand the incentive structure. These operators do not want your rate sheet. They want solutions that lower their LOE, because every dollar you help them save expands their residual equity through the waterfall. A vendor who helps the management team push DSCR above 1.25x is creating measurable economic value. That is a fundamentally different commercial conversation than negotiating monthly rates. Come with the cost reduction plan. The capital stack will do the rest.

The capital rotating out of private credit direct lending and into asset-based finance is not a temporary dislocation. Blue Owl, KKR, Blackstone, Ares, Apollo, and Carlyle are building permanent platforms. The banks are leaving. The void is being filled by a capital stack that is structurally different from the one operators and service providers are accustomed to negotiating against.

The counterparty across the table increasingly lives inside an ABS waterfall. Their economics, their incentives, their tolerance for cost, and their appetite for growth are all functions of that structure. If you understand it, you can position for it. If you do not, you are negotiating against a set of incentives you cannot see.

Understand the capital stack. It is the counterparty.

Nominally Hedged goes out to a small list. If you know someone thinking about improving sales / lowering CAPEX and OPEX — or who should be — forward it. That's the whole ask.