Nominally Hedged: The Best Bet in the Permian Is Against the Permian

Chevron's twenty-year Microsoft deal is a stack of bets, and the ones on top reprice decisions all the way down. We follow one to where it lands.

Nominally Hedged is Kalibr Partners’ briefing on what oil and gas actually costs: every category, CAPEX to OPEX, proprietary data systems, interpreted through a commercial lens. Whichever side of the negotiating table you sit on, you are the intended reader. The data is neutral: the iron does not change shape depending on who reads it. In any single engagement we sit on one side of the table, and we tell you which.

The most useful thing Annie Duke took from twenty years at a poker table was not a tell, or a bluff, or a way to count the cards that could still save a hand. It was a complaint about the English language. We do not have a clean word, she noticed, for a good decision that happens to turn out badly. When the cards come in wrong we call it a mistake, and when they come in right we call the player across the table a genius, and most of the time we are wrong on both counts, because we are grading the dealer’s work and crediting it to the player. She named the error “resulting”: judging the quality of a decision by the quality of its outcome, two things that are correlated, on average, eventually, and almost never in the moment you actually have to decide.

The cure she prescribed was to stop thinking in answers and start thinking in bets. A decision is a bet on a future you cannot see. When you choose, you are not declaring what is true; you are pricing what is likely, putting capital behind a probability, and accepting that a good price can still lose. This is not a metaphor energy people need translated. An oil and gas company is a machine for making bets under uncertainty, and everyone who works inside one knows it, whatever the investor deck calls it. You drill a well against a type curve you will not confirm for eighteen months. You hedge a strip against a price you do not control. You sign a ten-year midstream dedication against a basin differential nobody can forecast past next winter. The drill bit is a wager. The hedge book is a wager. The acreage is a wager. The only unusual thing about the industry is how rarely it says the word out loud.

The reason to say it out loud now is that the rest of the world has started pricing beliefs the same way, on purpose, and charging admission. Prediction markets have gone from a novelty to a quote you check, and the thing they do that a press release cannot is strip a decision down to its implied probability. A contract trading at sixty cents is not an opinion. It is a number that says the crowd thinks this happens sixty percent of the time, and you are welcome to disagree, except now your disagreement has a price and a counterparty. Once you have spent any time reading the world that way you cannot stop, which is the small tragedy of learning it. Every commitment starts to look like a position with an implied view buried inside it, and the headline is never the interesting part. The interesting part is the question underneath: what does this person have to believe for this to be the right bet?

So when Chevron signed a twenty-year agreement on June 22 to sell roughly 2.67 gigawatts of behind-the-meter power to a Microsoft data center in Reeves County, and the trade press filed it under “oil major becomes an AI infrastructure company,” the framing was not wrong so much as incurious. Infrastructure is the word you reach for once a bet has paid off and you would prefer everyone forget it was ever a bet. What Chevron actually signed is a portfolio of nested wagers, stacked one inside the next, each with an implied view you can read if you hold it up to the light. There is a bet about power prices and a bet about turbines and a bet about who needs whom more across a twenty-year table. And underneath all of them, doing quiet work almost nobody has bothered to price, is a bet against the Permian itself: against the value of the very molecule that made Chevron rich in this basin in the first place.

That last one is the one we do for a living. Hold that thought. We are going to walk down the whole stack to reach it, because the bet at the bottom only makes sense once you have seen the bets stacked on top of it.

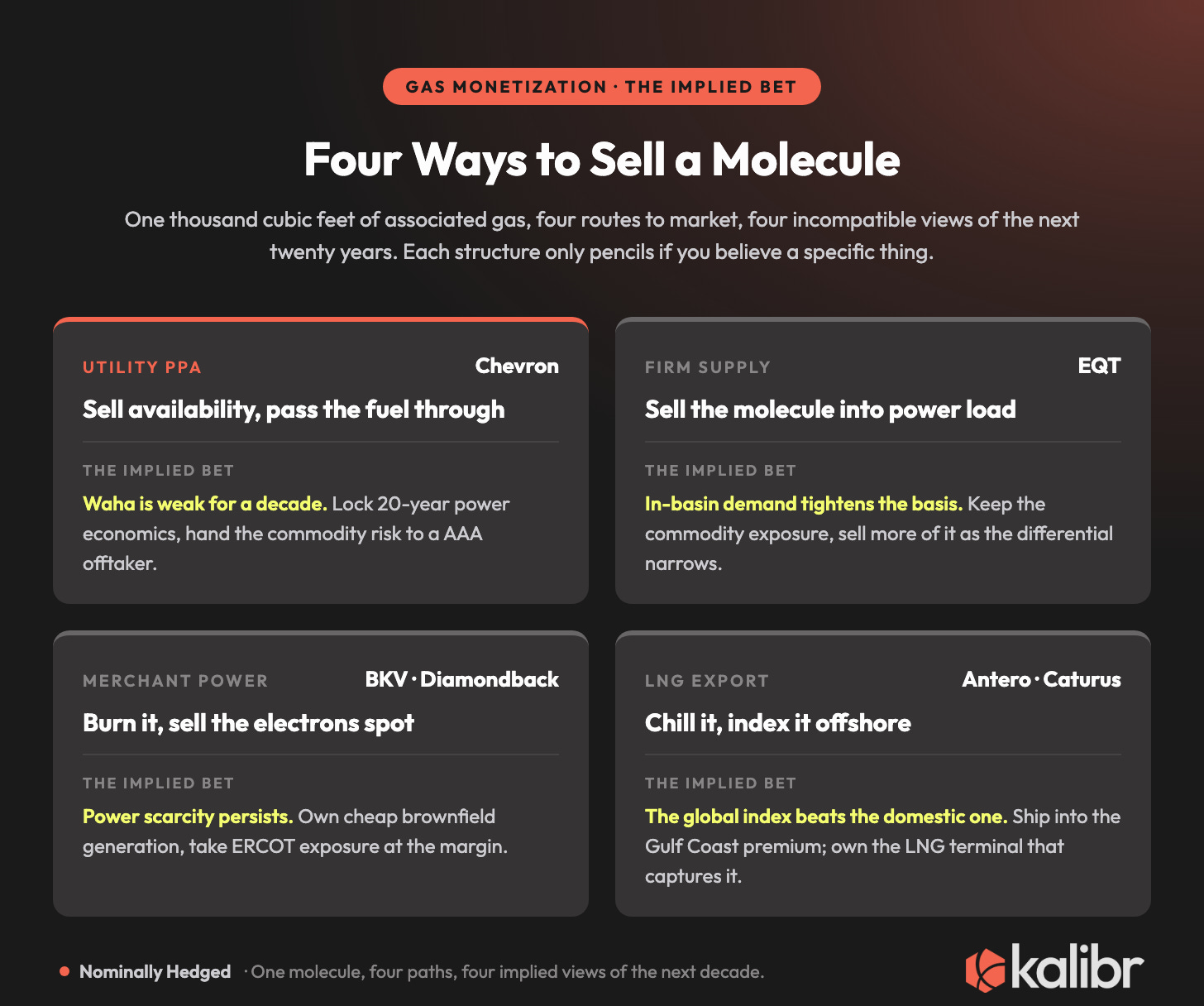

Four Ways to Sell a Molecule, Four Different Things to Believe

Start with the decision Chevron actually faced, because it is the decision every gas-long producer in America is facing right now. A molecule of Permian associated gas can be sold four ways:

1. as gas, to whoever is buying gas;

2. as firm supply, to someone who burns it for power and pays you for the molecules;

3. as merchant electrons, which you make yourself and sell into the grid; or

4. as LNG, chilled and shipped to a buyer indexed to a price on another continent.

These are not styles. They are positions, and each one pencils only if you believe a specific thing about the next ten to twenty years. Suppose you are Chevron, sitting on a molecule that has lately been worth less than nothing at the hub. Which of the four you pick is a confession about where you think that molecule is worth the most, and for how long.

1. The utility PPA, which is the bet Chevron made.

Chevron’s structure, signed through a subsidiary called Energy Forge One LLC, is the one that looks least like an oil and gas decision and is therefore the most revealing. Microsoft pays a fixed capacity payment to reserve the 2.67 gigawatts, and the variable cost, the gas fuel itself, passes straight through to Microsoft. Chevron has, in other words, reverse-engineered itself into a regulated utility: it earns a return on the iron and on the availability, and it has handed the commodity risk to a counterparty rated AAA. Reported economics put the first phase near $7 billion of capital (Chevron has not confirmed the figure, so treat it as reported, not disclosed) against a mid-teens return, first investment decision targeted for late 2026, first power in 2028. What the power actually clears at, I don’t know, and neither does anyone quoting it: broker estimates run from the low $60s per megawatt-hour to north of $85, which is less an estimate than a confession of how little is public. The deal is variously described as throwing off more than a billion dollars of annual EBITDA to the New Energies segment or roughly $250 million of annual free cash flow from 2029. Those are different metrics measured at different points, and the gap between them is the gap between a press release and a model.

Here is the implied view, and it is the whole point. You do not lock twenty years of power economics over your own gas, and then volunteer to pass the commodity through to someone else, if you think the commodity is going to be worth a lot. The PPA is a bet that the ten-year Waha outlook is weak. Chevron looked at the value of its own molecule at the hub, looked at the value of that same molecule converted to a reserved electron behind the meter, and decided the second number was so much larger and so much steadier that it was worth $7 billion and twenty years to stop selling gas and start selling availability. This is, to be clear, a smart trade: a way to be short your own molecule for two decades and collect a utility return for the privilege. It is also about the most bearish thing a Permian operator can do at the wellhead while keeping a straight face. You don’t take it if you think the molecule comes back.

2. Sell it like gas, which is the EQT bet.

Up in Appalachia, EQT looked at the same demand wave and made the opposite wager. Rather than build and own the generation, EQT signed long-term firm supply into power and data-center load: roughly 665 million cubic feet a day to the Homer City redevelopment (a retired Pennsylvania coal site being rebuilt as a multi-gigawatt campus) and about 800 million a day to an industrial park on the Ohio River, something on the order of 1.5 billion cubic feet a day of incremental demand contracted as molecules, priced index-plus. EQT keeps the commodity exposure it is famous for being the low-cost holder of (operating costs around $1.09 per Mcfe will do that), and bets that in-basin demand tightens the very differential that has haunted Appalachia, pulling its realized price up toward the hub instead of paying to ship gas away from it. It is the same demand wave Chevron is reading. EQT just read it as a reason to hold the molecule tighter rather than hand it off.

3. Burn it and sell the power merchant, which is the BKV and Diamondback bet.

A third group is splitting the difference: own the generation, but sell at least some of the output into the merchant market rather than under a fixed twenty-year capacity payment. BKV is buying brownfield combined-cycle plants in Texas at a fraction of greenfield cost (Temple I for about $570 per kilowatt in 2021, Temple II for roughly $460 in 2023, against the $1,000 to $1,200 it costs to build new) and underwriting incremental merchant PPAs at $80 to $100 per megawatt-hour. Diamondback has floated a joint venture with independent power producers to put gas-fired plants on its own Permian surface, pitching cheap land plus cheap gas as the package. The implied view here is the most aggressive of the three. It is the only one of the four that needs ERCOT to stay scared, tight enough for long enough that selling electrons at the margin beats the safety of a fixed contract.

4. Chill it and ship it, which is the Antero and Caturus bet.

The fourth answer ignores domestic power entirely and bets on the spread between American gas and the rest of the world. Antero sends roughly 2.3 billion cubic feet a day, about three-quarters of its production, into the Gulf Coast LNG fairway, and sits on transport that has been clearing a premium to Henry Hub (the Tennessee 500-leg path has run something like sixty-four cents over Henry Hub for calendar 2026, tapering to the high twenties by 2028), while keeping its NGL barrel almost entirely unhedged to catch the export bid. Caturus has gone a step further and is building the export itself: the Kimmeridge-backed South Texas producer (Abu Dhabi’s Mubadala owns 24.1 percent of it) is aiming more than a billion cubic feet a day of Eagle Ford dry gas at Commonwealth LNG, the 9.5-million-tonne, roughly $12.5 billion liquefaction terminal it controls on the Louisiana coast, with about 7 million tonnes a year already sold on twenty-year contracts to international buyers (EQT, Aramco, PETRONAS, Mercuria, Glencore), a final investment decision due in 2026 and first cargoes in 2029. The bet is that a global index beats a domestic one, that the molecule is worth more measured in Rotterdam or Tokyo than anywhere a pipeline can reach it at home. Antero is positioning for the export bid. Caturus is building the thing that sets it, which is a more expensive way of believing the same number.

Four companies, four structures, four incompatible views of the same future, all defensible, all funded. That is what a market under genuine uncertainty looks like: not consensus, but a spread of bets wide enough that somebody is going to be wrong and nobody yet knows who. Which leaves the only question worth asking once the bets are lined up side by side. Under what conditions does each one actually win?

When Each Bet Wins, and the Range That Decides It

A bet is only as good as the price you got and the world that shows up. So define the world. The parameters that decide which of these four wins are not exotic: the path of Waha and Henry Hub over the term, the power price you can clear, the capital cost per kilowatt, the capacity factor you actually run, and the length of the contract. Move those five and the ranking reshuffles.

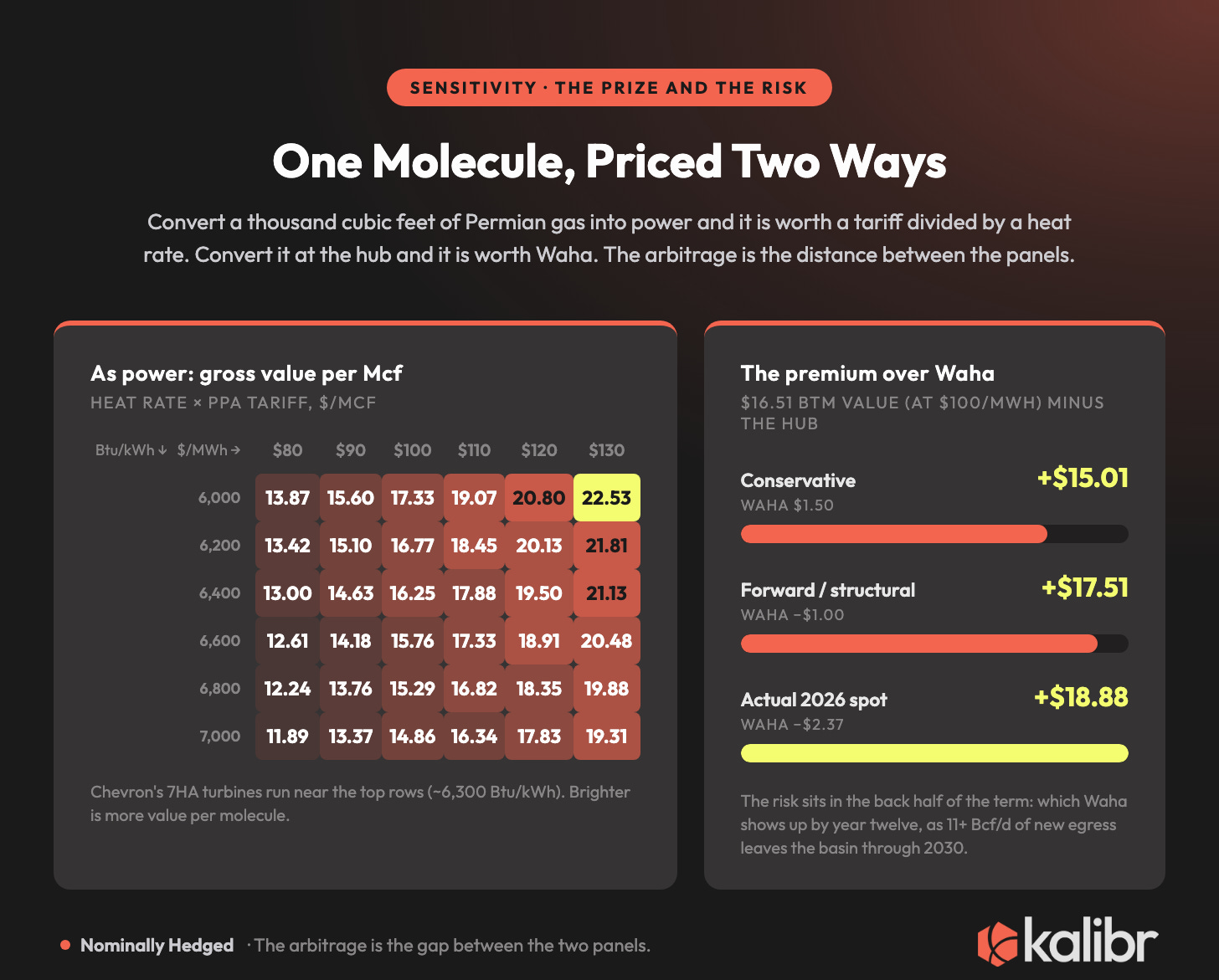

The cleanest way to see it is the napkin version: convert one molecule into one electron and price it both ways. A thousand cubic feet of Permian residue gas carries about 1.04 million Btu. Run it through Chevron’s chosen turbines at a design heat rate near 6,300 Btu per kilowatt-hour and you get about 0.1651 megawatt-hours of electricity out the other side. At a $100 PPA that molecule is worth $16.51 as power. At an $80 PPA it is $13.21; at $130 it is $21.46. The full grid of heat rate against tariff runs from roughly $11.89 to $22.53 per Mcf of gross power value, and the entire arbitrage lives in the distance between those numbers and what the same molecule fetches as gas.

This is where the honest range matters, because the gap between the conservative case and the actual 2026 case is enormous, and we are going to carry both rather than quote whichever one flatters the thesis that day.

The conservative case is the one our own model was built on before the year got strange: Waha around $1.50 and a PPA around $65, run through the thirstier bridge-generation heat rate rather than the efficient turbines. Even there the arbitrage is real. Push the conservative inputs through the same conversion and the molecule is worth about eight dollars as power against a dollar and a half as gas, better than five to one, which is already enough to change every downstream decision in this article.

The actual 2026 case is not conservative at all. Waha has spent the year below zero. The hub averaged about negative $2.37 per million Btu early in the year, printed negative $3.30 in May, and stayed underwater for 89 consecutive trading sessions, which obliterated the prior record of 27 set in 2024 (records in this market do not get broken so much as embarrassed). For stretches this spring the Permian was paying people to take its gas, and the prompt month traded as low as negative $5.69. Against a negative Waha the power conversion stops being a re-rating and becomes a rescue. The molecule went from a liability you pay to dispose of to a reserved electron worth sixteen dollars, and the spread is the entire number, not a premium layered on top of one.

Put the two together and you get the range that actually decides the bet. The premium of behind-the-meter power value over the Waha alternative runs somewhere between roughly $13 and $16 per Mcf in the published scenarios, and wider than that on the days Waha is deeply negative. That is the prize. The risk is not in today’s number. It is in the back half of the term, because the same forces that crushed Waha are scheduled to ease: more than 11 billion cubic feet a day of new egress is set to leave the basin through 2030 (Blackcomb at 2.5 Bcf/d late this year, Hugh Brinson’s first phase around the same time, and a queue behind them), and Permian gas production that ran 17.2 Bcf/d in 2021 and 27.6 in 2025 keeps climbing toward 28-plus by 2030. The forward curve already converges toward Henry Hub through the late 2020s, with serious modelers pegging the Waha discount settling into roughly negative 25 cents to negative $1.25 per Mcf once takeaway catches up. So the thing Chevron is betting against is scheduled to partially fix itself, on a known timetable, and Chevron signed anyway, for twenty years, which tells you how long it thinks the broken part lasts.

So read the four bets against that range. The utility PPA wins biggest precisely in the world Chevron is implicitly forecasting: Waha weak-to-negative for years, power firm, the commodity a thing to be rid of. It wins least in the world where egress overshoots and Waha snaps back to a healthy positive number, because then Chevron handed twenty years of commodity upside to a AAA counterparty in exchange for a utility return, which is a fine outcome and a small one. The EQT bet is the mirror image: it needs the basis to tighten, and it loses if demand disappoints and Appalachia stays long. The merchant bet needs ERCOT to stay scarce and is the first to break if it doesn’t. The LNG bet needs the international spread to hold against a wave of global liquefaction. None of them is free. Each is a price on a different probability, and only one of the four has actually shown you its hand, because the structure Chevron chose makes no sense unless Waha stays broken.

The Equipment Is the Position

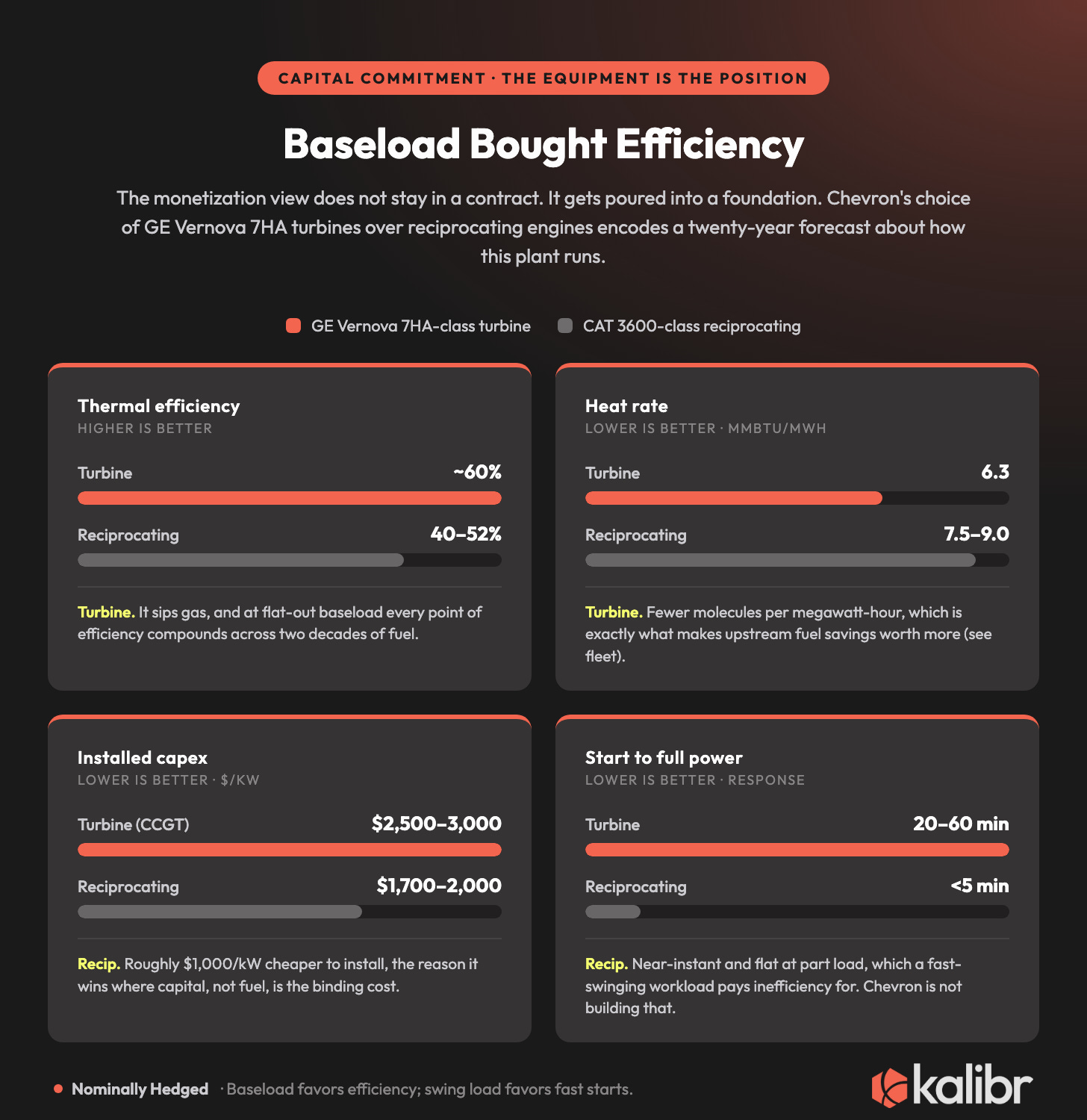

Here is where the bet stops being a spreadsheet and becomes steel with a lead time, because the monetization view does not just sit in a contract. It gets poured into a foundation, and the equipment you choose is the bet made physical and made expensive to reverse.

Chevron’s deal leans on two kinds of iron. The bulk of the generation comes from GE Vernova heavy-duty gas turbines, the 7HA class, running at roughly 60 percent thermal efficiency and that 6,300 Btu per kilowatt-hour design heat rate, with Caterpillar’s Solar Turbines supplying additional dispatchable capacity. The partner structure is its own tell: Engine No. 1, the activist-turned-energy-investor, launched a company called Joulent (built with GE Vernova) that holds a 50 percent option to co-fund the project. That option is not a footnote. It is optionality in the literal finance sense, a way to commit to the slot without committing all of the capital, which is exactly what you do when you like a bet but would rather keep your downside sized to your conviction.

The heavy-duty turbine is a bet on efficiency at baseload. It sips gas relative to the alternatives, which matters enormously when you intend to run it flat-out for twenty years and every hundredth of a point of heat rate compounds across two decades of fuel. The competing iron is the reciprocating engine, the Caterpillar 3600 class and its kin, and it makes the opposite bet. A recip is less efficient (heat rates of 7.5 to 9.0 against the turbine’s 6.3, an efficiency of maybe 40 to 52 percent), and it costs less up front (call it $1,700 to $2,000 per kilowatt installed against $2,500 to $3,000 for combined cycle), and it does one thing the turbine cannot: it starts almost instantly, full power in under five minutes, and it barely loses efficiency at part load. For a workload that swings hard and fast, the recip’s responsiveness is worth paying inefficiency for. For a hyperscale baseload that wants to run pinned at the top of its range, the turbine’s efficiency is worth paying for. Chevron is building for steady AI baseload over twenty years, so it bought efficiency, and paid for it in capex it cannot easily walk back.

And the choice is getting harder to make and harder to unmake, because the iron itself is now the scarce asset. GE Vernova is sitting on something like 100 gigawatts of gas-power commitments (roughly 44 gigawatts of firm backlog plus another 56 in slot-reservation agreements) inside a corporate backlog north of $160 billion. Caterpillar’s backlog hit a record $62.7 billion, with its reciprocating-engine book up more than three and a half times since the start of 2024 and lead times past 200 weeks, which is to say you can order the engine today and take delivery sometime after the contract you bought it to serve has begun. The top turbine makers cannot deliver a new heavy-duty machine before the end of the decade. Chevron locked seven GE Vernova turbine slots with deliveries in late 2026 and 2027, and those reservation agreements carry non-refundable down payments of 10 to 20 percent of the equipment cost. Pause on that. The slot reservation is itself a bet, a non-refundable premium paid for the mere right to build, in a market where the right to build is suddenly the binding constraint. You are no longer just betting on power prices. You are betting on your place in a four-year queue, with real money you don’t get back if you are wrong about needing the place.

Every bet so far has been visible from the outside. The PPA is in a press release. The turbine order is in a backlog. The Waha strip is on a screen. They are the bets everyone can see, which is precisely why everyone is writing about them. The bet nobody is pricing is sitting in a field in Reeves County, burning gas to do its job, and it happens to be the one we can actually measure.

A Third to a Half of the Fleet Already Stands Behind It

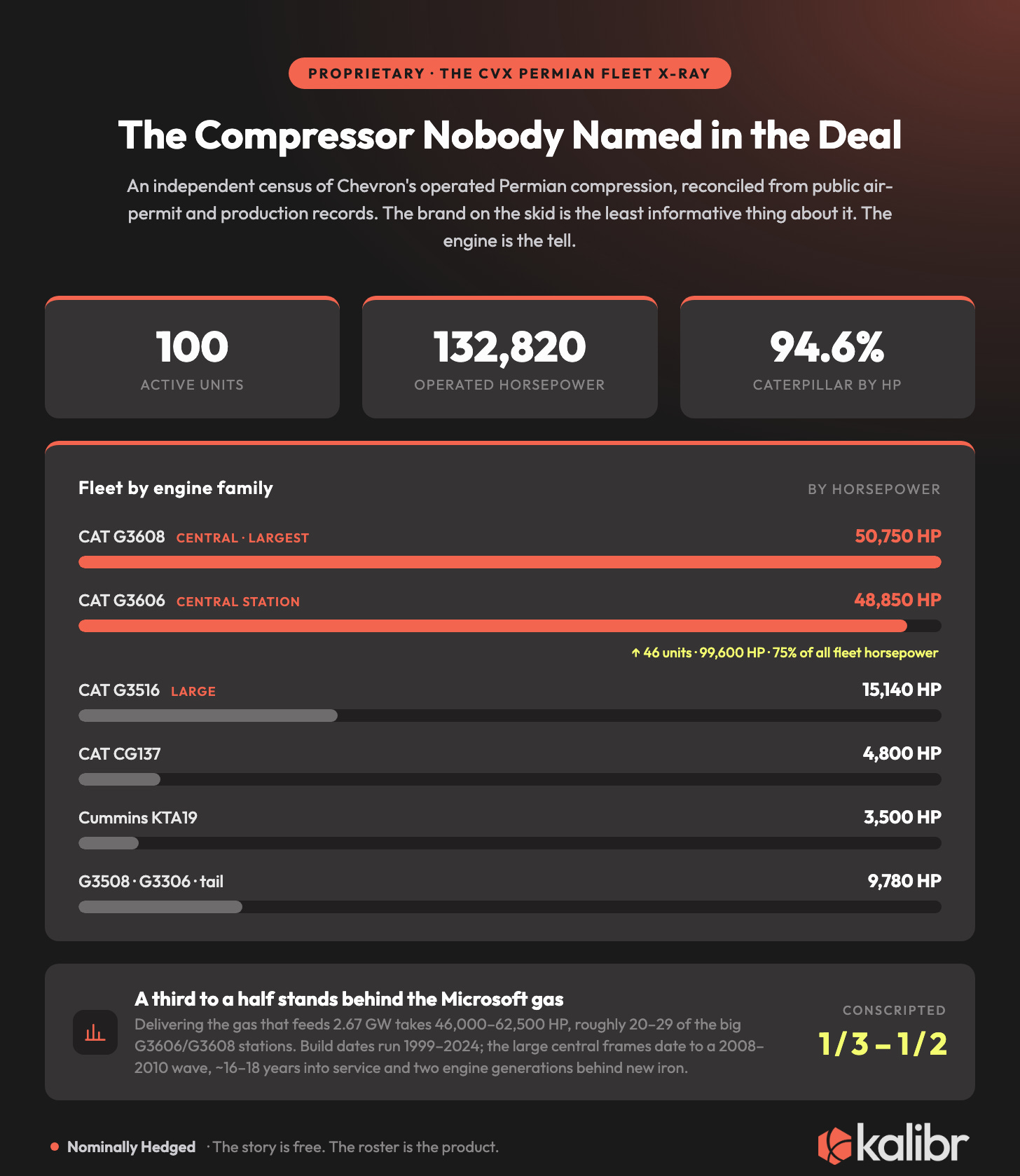

We have spent years building the one thing nobody outside a compression vendor has ever had: an independent census of the iron. Who runs which units, where, of what make and vintage, behind which operator, across the Permian, reconciled against what the vendors themselves disclose. We are going to use it here at the level the argument needs and hold the unit-by-unit roster back, because the roster is the product and the argument is the advertisement. What the argument needs is the shape of Chevron’s fleet, and the shape is unusually clean.

Chevron operates ~100 active compression units in the Permian, 132,820 horsepower, and the fleet is almost entirely one make. Caterpillar is 94.6 percent of the horsepower. Two engine families do most of the work: the G3608, twenty units at 50,750 horsepower, and the G3606, twenty-six units at 48,850 horsepower, which is forty-six big central-station machines carrying 75 percent of every horse Chevron runs in the basin. The largest iron lives in New Mexico, where Eddy and Lea counties hold 48 percent of the basin horsepower on thirty units, at stations whose names sit in the public air permits: Sand Dunes, Dagger Lake, Antelope, Pronghorn, Hayhurst, Salado Draw. And roughly half of all that horsepower, about 51 percent, runs under a single compression provider, which makes one packager the dominant landlord on Chevron’s Permian iron (we know which one, and we can age every unit it runs). Hold that fact too. It comes back.

Now lay the data center on top of the fleet. Delivering the gas that feeds 2.67 gigawatts takes somewhere between a third and a half of this iron. Size it against the efficient turbines Chevron actually bought and it is about 46,000 horsepower; size it against thirstier bridge generation and it is closer to 62,500; either way it is twenty to twenty-nine of those big G3606 and G3608 stations, the Sand Dunes and Dagger Lake and Antelope machines, give or take. Read that sentence twice, because it is doing something the deal coverage missed entirely. A third to a half of Chevron’s Permian compression fleet is now standing behind a twenty-year power contract with Microsoft. Nothing in the press release, the broker notes, or the deal’s own org chart so much as mentions a compressor, which is roughly the standard treatment for the asset that actually moves the gas.

And the database ages the iron. The build dates span a quarter century, from a lone 1999 unit to a single new 2024 machine at Antelope, and the horsepower that matters here sits in two clusters: a wave of large central frames built between 2008 and 2010 and a buildout of smaller wellhead units across 2013 to 2015. Date the big G3606 and G3608 stations that feed the data center and they land in that 2008-to-2010 window, iron sixteen to eighteen years into a service life, running lean-burn technology two engine generations behind what you would install new today. Old, thirsty iron, sitting in the gas path of a twenty-year power contract. For fifteen years that was a deferred-capital problem nobody could justify fixing. Whether it still is depends entirely on what the gas it burns is now worth, which is the arithmetic in the next section.

The Gas the Compressor Burns Was Repriced by a Contract It Never Signed

A bet this size does not stop in the boardroom. It travels all the way down to the person turning the wrenches, and it quietly changes what their job is for. Take a production engineer on these assets. The week is a priority stack: keep the wells flowing, keep the compressors up, chase the next tie-in, hold lease operating expense down. Fuel gas has never been on that stack, and it never should have been. A compressor burns field gas to run (the driver on a G3606 or G3608 is itself a Caterpillar engine, pulling gas off the stream to turn the crank), and across the operated fleet that burn is about 16.7 million cubic feet a day, roughly 1.5 percent of the gas. Priced at the wellhead, it is a rounding error every engineer correctly ignores. You do not optimize a molecule worth a dollar and a half when the well next door makes ten thousand dollars a day. Ignoring it was the correct arithmetic, and it stayed correct for years.

And lately the molecule has been worth less than nothing. At a negative Waha the gas a compressor burns is, strictly, a molecule you were going to pay to dispose of, combusted for free to do useful work, which is the one silver lining of negative prices nobody puts on a slide. So the fuel-efficiency upgrade has never penciled. Every compression engineer in the Permian knows the old iron is thirsty, and every one of them has watched that upgrade die in the capital committee, because the thing it saved was never worth the capital it took to save it.

Priced at the wellhead. That is the assumption the data center just broke.

Now run the same molecule through the new contract. Once the gas this fleet moves is feeding 2.67 gigawatts of reserved power, the molecule a compressor burns is no longer worth the Waha price. It is worth what it would have made as power, the PPA price divided by the plant heat rate, on the order of sixteen dollars per million Btu at a hundred-dollar tariff. The compressor’s fuel gas did not change. The molecule did not change. A contract it never signed changed what the molecule is worth, by roughly an order of magnitude, and in doing so it lifted fuel-gas efficiency from the bottom of that production engineer’s priority stack to somewhere near the top. The strategic bet, made once at the top of the chain, reaches down and rewrites what the person at the bottom is paid to optimize.

Put the arithmetic on the table, both ways, because the gap between the two is the finding. Repower the old, thirsty iron (call it the 60,000 horsepower of pre-2015 large frames that sit in the data center’s gas path) with modern lean-burn engines, and you cut fuel consumption on that horsepower by about 12 percent. That frees up roughly 0.94 million cubic feet a day of gas, about 343,000 million Btu a year, that used to go up the stack and now does not.

Measured the old way, against Waha, that saved gas is worth about half a million dollars a year, and in a negative-price stretch it is worth nothing or less. The project dies, the way it always died.

Measured against the PPA, the same saved gas is worth about $2 million a year in our conservative world ($65 power, the thirstier heat rate, Waha at a buck and a half) and closer to $6 million a year in the world that actually showed up ($100 power, the efficient turbines, a Waha that has been deeply negative). The capex is identical and the molecules are identical. The only thing that moved is where the saved gas goes, and where it goes is now worth four to twelve times what the hub would have paid for it. Over the twenty-year term of the contract, discounted, that single repower is worth somewhere between roughly $18 million and $53 million of value created out of the identical physical project, which is what turns a fuel-efficiency upgrade from an O&M line the capital committee rejects into a revenue-backed investment it should be fighting to fund.

And that is the floor, because it assumes you swap like for like, which no one who has read this far would. The fleet was sized for a job it is no longer only doing. Right-size the horsepower to the throughput it actually moves, optimize the operating points instead of running big frames at part load, and the savings compound on top of the vintage swap. Run the logic across the full hundred-thousand-odd horsepower of G3606 and G3608 iron and the saved gas roughly doubles, the annual value runs to $12 or $13 million, and the twenty-year figure crosses $100 million, all of it out of compression nobody outside the vendor had bothered to age.

There is a twist in here worth saying plainly, because it inverts the instinct most people walk in with. You would think a more efficient power plant makes the upstream fuel savings matter less. It is the opposite. The better the plant’s heat rate, the more electricity each saved molecule becomes, and so the more each saved molecule is worth. Chevron buying the efficient turbines made the compression prize bigger, not smaller. (I had this backwards the first time I ran it, which is how I know it is counterintuitive.) The bets are stacked, and they compound in the same direction.

The bet also changes when you should move. Compression iron goes through major overhauls on a schedule regardless of any of this, and a repower folded into that cycle, or into the data center’s own multi-year ramp toward first power in 2028, lands as a planned swap rather than a capital shock. Do it proactively and the upgrade rides existing maintenance spend with no large step-up in operating cost. Do it reactively, after a failure or a scramble to feed a contract that is already signed, and you pay the premium twice, once for the iron and once for the hurry. So the move is to do it early, on the maintenance cycle, before the signed contract turns a planned swap into an emergency.

Now read the same case from the other side of the contract, because roughly half of this fleet is not Chevron’s iron at all. It is the provider’s, rented under contract, and the engine that just got repriced sits on the packager’s balance sheet, not the operator’s. A compression company that understands this before its customer does is not looking at a fuel-efficiency problem. It is looking at a go-to-market: approach the operator first, fund the new iron, and bundle the upgrade into a longer contract term, which is exactly the trade the equity market rewards a packager for making. The REIT model is unforgiving here, because a packager’s multiple is a function of contracted backlog and duration, so an upgrade the customer already wants, written into a longer term, is the rare deal that improves the asset and the contract at the same time. Get to that number before your competitor and you write the longer renewal yourself, which is the whole game; get there late and you inherit a contract where the upgrade was already funded on someone else’s balance sheet.

This is the part no press release can show you. One strategic bet, made once, at the top of the chain, reaches down and rewrites a production engineer’s priority stack, a capital committee’s hurdle math, and a packager’s sales motion, all at once, and it does it differently for every player depending on the bet they made and the iron they hold. The same map that reads Chevron’s implied view also tells you where the next fleet upgrade, the next contract extension, and the next exposed operator are going to surface. Reading how each bet wins and loses is how you get to plan around the people making them instead of reacting after they have moved.

Resulting in Reeves County

Strip the deal back to what it is and it is one directional bet, made by one operator, that the molecule is worth more as a reserved electron than as Permian gas. A bet that size does not stay where you place it. We have just followed it from a PPA to a turbine slot to the fuel a compressor burns to the renewal between an operator and the landlord that owns its iron, repricing each rung on the way down, and the only people who can see the whole path today are the ones who can read the fleet.

So the discipline is the one Duke prescribed: refuse to result. Read the implied view, not the outcome that has not arrived. Chevron’s structure wins only if Waha stays broken for a decade, which is a real and well-made call, and also one that can be wrong, with a probability attached and a way to lose, which is everything the word “infrastructure” is built to paper over. Everyone downstream is holding a piece of that same wager now, most of them without having chosen it. The operator that reruns its fuel math moves its repowers early. The packager that sees the renewal coming gets there before its rival does. The investor reads the iron instead of the press release.

Whether Chevron is right about Waha, I don’t know. Neither does Chevron; that is what makes it a bet rather than a fact. What I do know is that the bet traveled four steps down a chain the deal never named and came to rest on a compression fleet nobody told it was holding a position. The fleet is real, it is old, and it is sitting in Reeves County with its build dates. Anyway, that is where I would start reading.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. Kalibr Partners is an independent firm and is not affiliated with, endorsed by, or compensated by any company named herein. The analysis draws on public sources (SEC filings, earnings calls, press releases, and state air-permit and production records) together with Kalibr’s proprietary compression dataset; figures are presented in good faith without warranty as to accuracy or completeness, and certain figures are estimates or reported (not officially disclosed) and are flagged as such. All trademarks and company names are the property of their respective owners.