Nominally Hedged: Survivor, Sovereign Debt and SOFR

From Tokyo to Texas: How Japanese 20-Year Bonds Affects a Waukesha in Midland

Why We Study Your Peers

I got an interesting question from a friend last week that’s been tumbling around in my head:

“Why do you guys write about other E&Ps if your core business is vendor negotiation intel?”

It’s a fair question—smart even—because on the surface, it doesn’t seem obvious. But let’s use my favorite tool for unpacking not-obvious things: games.

Strategy, Survivor, and SEC Filings

Games aren’t trivial. In economics, we gave them their own field—Game Theory—because of course we did. Games are powerful mental models. They help us clarify chaos, identify incentives, and reverse-engineer victory. Reality rarely offers that kind of clarity, but games are the closest thing we have to X-ray vision.

Speaking of games: ever watch Survivor?

It’s basically corporate strategy on an island—fewer earnings calls, more coconut-related injuries.

There’s one challenge that always stuck with me: two teams, 21 flags. On each turn, you can take 1 to 3 flags. The goal? Take the last one. So what’s the optimal opening move? Take 1 flag. Why? Because if you work backward from the endgame, you want your opponent stuck with 4, 8, 12, 16, or 20 flags. That’s how you control the board.

This is what we do at Kalibr. We reverse-engineer strategy. We map the field, assess the players, and model behavior based on incentives. Because while Survivor ends in fire-making, oilfield strategy ends in contract terms, unit rates, and activity continuity.

But real life adds complexity. Unlike in Survivor, where every contestant wants to win and mostly means it, corporate negotiations have two complicating factors:

1. Ambiguity Around Opponent Objectives

In Survivor, incentives are obvious. In business, they’re legally footnoted.

Here’s where public markets lend us a hand. Thanks to SEC filings, earnings calls, and investor decks, public companies must spell out their priorities. And while 10-Ks read like sedatives, they’re beautifully honest in what they reveal. Want to know what keeps a CEO up at night? Read the risk section.

Public companies are disciplined—not because they want to be, but because the cost of even perceived deviation is litigation. For private companies, the game is murkier—but even tighter. Less transparency, but more expensive capital. If rates are tightening for the majors, they’re suffocating the privates.

Everyone’s playing the same game. Just with different levels of oxygen.

2. It’s Never a Two-Player Game

Your vendor isn’t just negotiating with you. And your investors don’t grade on a curve—they grade on a curve against your peers.

Since 2020, the average E&P balance sheet has gone from wildcatter to wealth manager. Hedged. Disciplined. Shareholder-obsessed. But capital doesn’t flow to “good” companies. It flows to the best relative option.

Want Permian exposure? Investors choose between CIVI and MTDR. Need revenue? Vendors do the same. And your financial health—particularly your relative resilience—dictates how likely you are to keep drilling when prices wobble.

More resilience equals more predictable activity. And in a spot market-dominant industry, where contracts are often handshake-plus-terms, that reliability becomes leverage.

Debt: The Invisible Hand Behind Every Contract

We spend a lot of time talking about WTI’s effect on rig count. But that’s first-order logic. Let’s talk second and third-order. Let’s talk debt.

And let’s do our best Ashton Kutcher impression for a butterfly effect that starts with Japanese 20-year government bonds and ends with compression rates in the Permian.

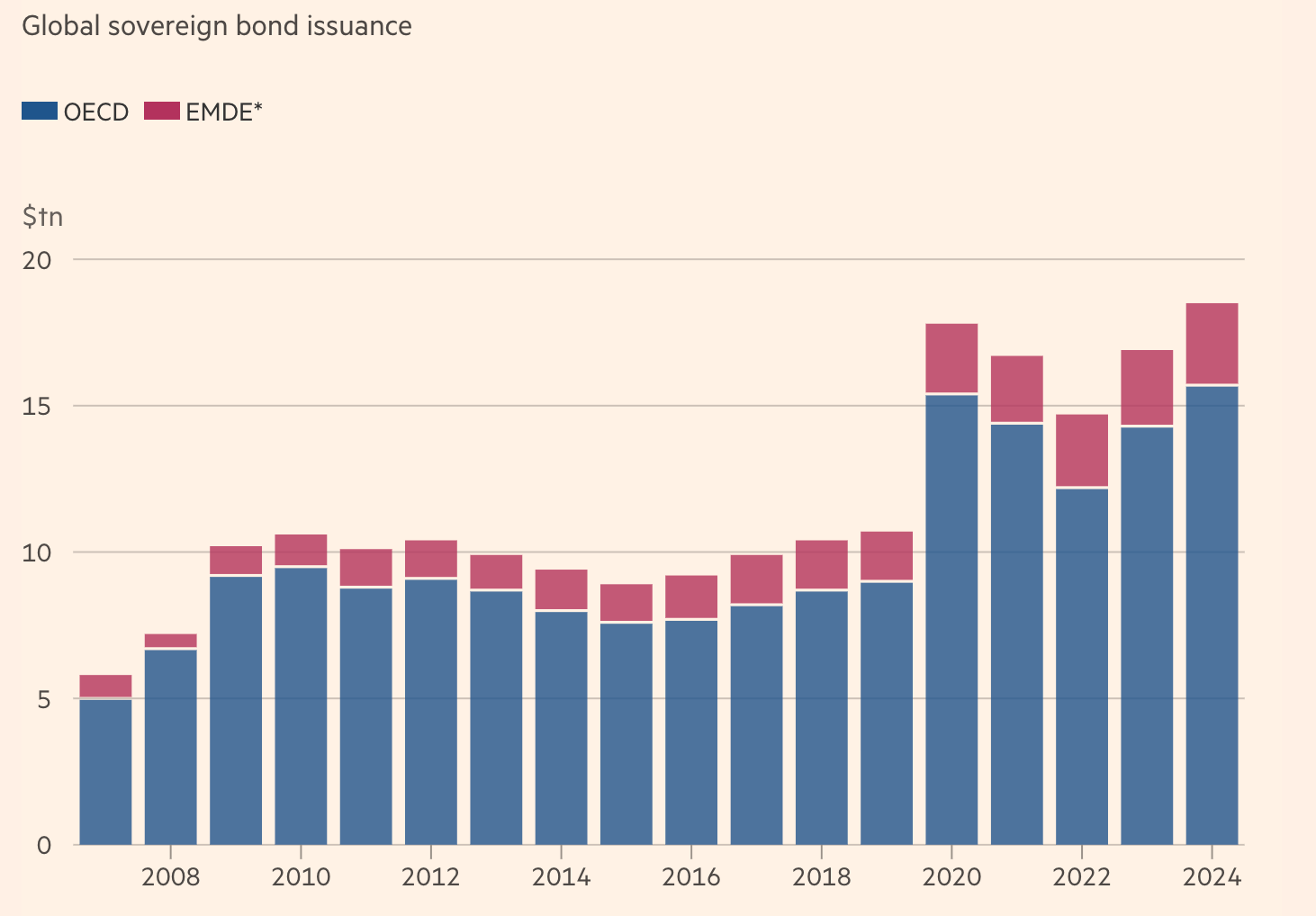

Debt is no longer boring. It’s existential.

Private credit has ballooned to a $3 trillion market. LIBOR is gone; SOFR now ties your borrowing cost to Jerome Powell’s caffeine intake. Meanwhile, demand for sovereign debt is cooling, pushing term premiums higher. That means capital is getting more expensive—and more selective.

So let’s roleplay. I’m Kalibr Resources, a public Permian E&P bidding for compression capacity. My peer set? CIVI and MTDR. My vendors? USAC and KGS. How does macro dislocation in the credit markets influence my cost to lift a barrel?

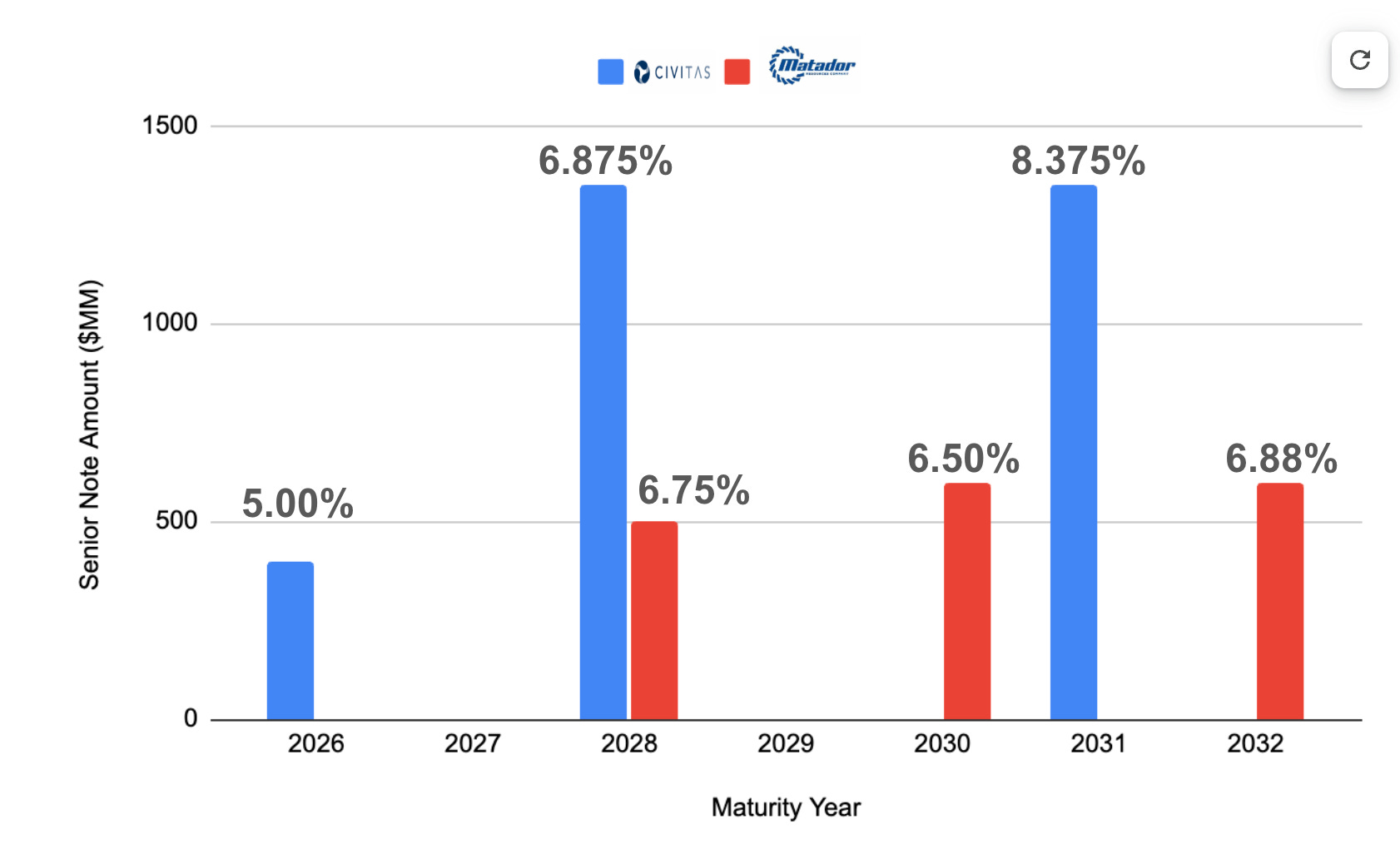

CIVI: Constraint Disguised as Control

Civitas (CIVI) is sitting on $5.15B in debt and has promised to trim it to $4.5B by year-end 2025. Sounds disciplined. But let’s peek under the hood.

Fixed-rate notes ranging from 5.0% to 8.375%. A $450M revolver floating at SOFR + 250 bps (~7.8%). And $400M in 2026 maturities. If refinancing happens in a 9.5% world, interest expense spikes up to $15.2M/year post-tax—a direct hit to discretionary FCF.

Pile on a $1.775B CapEx plan and $183M in fixed dividends, and CIVI’s flexibility starts to look more like fragility. Asset sales? DJ Basin packages are now trading at discount rates normally reserved for junior mining equities.

CIVI isn’t distressed (far from it)—it’s just running low on strategic oxygen.

MTDR: The Luxury of Optionality

Matador (MTDR) plays a different hand. $2.95B in debt, no material maturities until 2028. A lightly drawn revolver. $1.8B in liquidity. Fitch gave them a sticker and a smile.

Even in a $62 WTI world, they’re generating FCF. San Mateo midstream throws off stable cash. Management has options—pay down debt, return capital, or buy growth when others can’t.

CIVI is managing risk. MTDR is managing optionality. And in a world where CAPEX decisions compete with refinancing walls, vendors notice the difference.

Vendor Balance Sheets Aren’t Boring Either

Let’s flip the table.

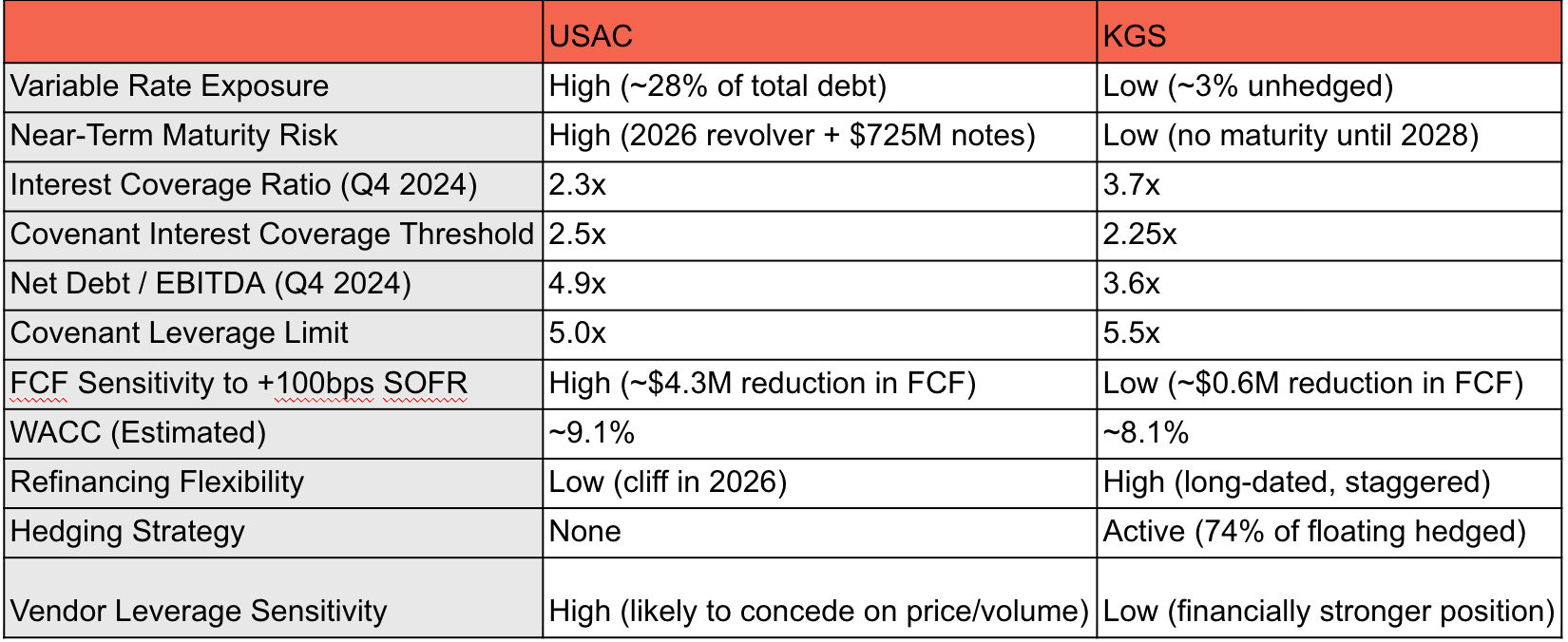

Take USAC and KGS—two giants in the compression game. Structurally? Couldn’t be more different.

USAC: $2.3B in debt. Half floating. Refinancing cliffs ahead. SOFR rising means their FCF is getting squeezed. Warrants? The financial equivalent of “exposure therapy”—nostalgic but not useful.

KGS: $2.57B in debt, but $1.4B is hedged via swaps. Minimal floating-rate exposure. Result? Predictable cash flow, stable dividends, and internal reinvestment without panic.

So ask yourself: in the next compression cycle, which vendor is more likely to hold firm on price? Which one is likely to blink?

Strategic Implication: Relative Health Drives Contract Outcomes

Let’s state the obvious that most operators miss:

Your vendor is watching your peers.

You’re not just managing operations. You’re managing optics.

If your peer is financially strained (again, relative to others, no one is in the 2010s situation now adays), their program is more likely to be downsized. That gives you—assuming stronger footing—an opportunity to be the safer, stickier partner. That doesn’t just lead to better pricing. It leads to continuity, preferred terms, and preferred treatment.

Why We Model Peers

This is why we analyze E&Ps.

This is why we break down vendor balance sheets.

This is why we connect sovereign debt apathy in Tokyo to frac spreads in Midland.

Because macro forces don’t just influence public markets.

They cascade down into every decision—every deal, every contract, every execution risk.

That’s what Kalibr’s intelligence platform delivers:

Multi-dimensional strength assessments

Category-specific vendor pressure indicators

Probabilistic contract scenario planning

And yes, reverse-engineered flag games.

So no, we don’t just “write about” other E&Ps for sport.

We study them because understanding their balance sheet sharpens how we negotiate yours.

Because in this game, knowing your next move isn’t enough.

You need to know theirs.