Nominally Hedged | Q1 2026 Earnings Intelligence: NGS + Flowco Deep Dive

Two vendors posted their best quarters ever. Both immediately told Wall Street not to believe it. We took them at their word.

Programming Note: Pushing the CAT supply forecast breakdown until after the holiday. Be on the look out next week!

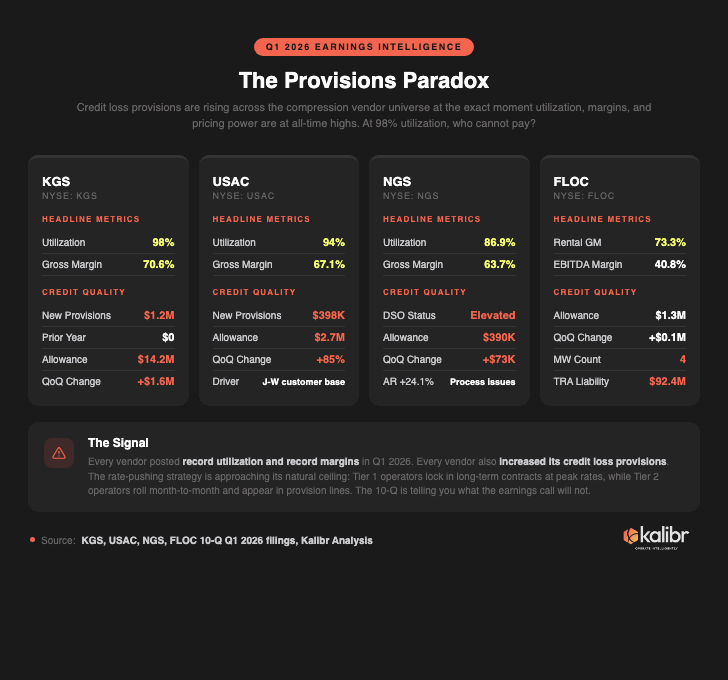

Last week I ended the quarterly update with a question that I did not answer. It was buried in the Bifurcation section, two paragraphs past the part about KGS signing a 10-year contract extension (still the longest primary term ever disclosed in public compression), in a sentence that was doing a lot of work for something that looked like a throwaway.

The sentence was: “KGS booked $1.2 million in credit loss provisions in Q1, up from zero in Q1 2025. At 98% utilization and record margins, who cannot pay?”

I left it there because I did not have the full picture yet. I do now.

Here is what happened when I pulled the same line item across every public compression vendor’s Q1 2026 10-Q filing. Not the earnings call transcript (where nobody mentioned it). Not the investor deck (which is a marketing document with fonts). The 10-Q, which is the one document that an auditor has reviewed and a CFO has signed and a securities lawyer has blessed, and which, because of all of that, contains the things that companies would rather you did not read carefully.

KGS: $1.2 million in new credit loss provisions. Allowance up from $12.6 million to $14.2 million. USAC: allowance up 85% in a single quarter, from $1.5 million to $2.7 million. NGS: CFO acknowledged DSO was “above our expected level” due to “discrete collection and process-related items” (which is a very polite way of saying “some of our customers are slow-paying and we are not entirely sure our back office noticed quickly enough”), allowance up to $390,000 from $317,000. Even Flowco, which is a different business model and probably should not be in this comparison except that I find it interesting, ticked up from $1.2 million to $1.3 million.

Every vendor posted record margins. Every vendor posted record or near-record utilization. Every vendor also quietly increased what it expects never to collect.

There is a wonderful term in behavioral economics for what the 10-Q just gave you. Revealed preference. Companies say a lot of things on earnings calls. (Mickey McKee said pricing power “will continue to 2027 and beyond,” which is a thing you say when you believe it, but also a thing you say when you need your stock to trade above 9x EBITDA.) The provision line is different. The provision line is what the company tells its auditors when no one is performing for the sell-side. It is the honest answer to the question: of all the revenue you booked, how much of it are you actually going to get?

At 98% utilization, the answer got worse.