Nominally Hedged: Organic Growth Gets Moldy, AI Bros Hoard 3306 Compressors, and Deficits Aren’t Sudden Onset Emergencies

When "drill it yourself" hits bedrock, GPUs meet horsepower, and trade deficits turn into existential dread.

Organic Growth Has a Shelf Life

Even for EOG.

For years, EOG wore its “organic growth” badge like armor. It wasn’t just a strategy—it was a brand. A signal to investors that while everyone else was out chasing $80,000 per acre and announcing billion-dollar “synergy” deals, they were doing it the old-fashioned way. Drill it. Earn it. Repeat.

And it worked. EOG had the rock, the returns, and the reputation. The last time they did a material deal—Yates, 2016—they were still explaining the Permian to analysts. Since then? Nothing. Just discipline and delineation.

Which is why the Encino deal matters.

Not because it’s reckless. (It’s not.)

Not because it’s expensive. (It isn’t.)

But because it signals something that, until now, EOG never had to say out loud:

Even the best-run E&Ps eventually run out of rock.

Let’s be clear—this is a good deal.

$5.6B for 235 MBOE/d implies ~$24,000 per flowing barrel, well below public comps trading north of $26K/BOE/d—and Encino brings a balanced product mix (~20% oil, ~30% NGLs, ~50% gas) with existing ops and midstream adjacency. Compare that to the FANG–Double Eagle tie-up, where undrilled locations cleared $6 million each.

Even better, EOG is funding it with just $2.1B in cash and a little leverage. The rest? Synergies and PDP. They’re modeling 10% EBITDA accretion and 9% FCF uplift. As Larry David would say, “Pretty, pretty, pretty good.”

For Encino, it’s the IPO alternative—one with a cash-out and a transition plan.

But for EOG, it’s more than financials. It’s narrative.

The company said “organic” 8 times on the Q1 call.

But this time, it felt less like a mission and more like a memory. They still talked about their $45/$2.50 hurdle rates. They still said the Utica play is self-sourced. But if it quacks like a duck and clears like an M&A deal, well—it’s a duck.

This is what smart strategy looks like when geology begins to outpace capital discipline.

The pivot isn’t to M&A. The pivot is to reality.

The consolidation wave of 2022–2023 was dressed up in synergies and scale. But the real truth? The best rock is running thin. And now, even the most devout “organic-first” operators are quietly buying what they once insisted they could build.

EOG didn’t blink. That tells us something. If they need to go external to maintain the story, others will follow.

Because the real scarcity now isn’t cash. It’s inventory.

Closing thought:

This isn’t a strategy shift. It’s an update to the math.

When organic growth becomes geological wishful thinking, you buy what can’t be drilled—and remind the market you’re still the best allocator in the room. Even if that means finally opening your wallet.

Oilfield Unicorns

When I co-founded Clear Creek Resource Partners, a scrappy private equity firm chasing North DJ assets, my biggest headaches weren’t sophisticated strategic questions—they were visceral, physical problems. Like sourcing a workover rig on Christmas morning to fish a wrench out of tubing. Or replacing a man-camp door after a completion superintendent punched through it over a heated debate about Keith’s drill-out method (High Reynolds number forever). It was gritty, tangible, real-world infrastructure dilemmas, and the thorniest was classic chicken-and-egg: drill wells to justify pipeline investment, or build pipelines to avoid flaring gas.

Amidst our infrastructure scramble, my CEO suggested a sit-down with a solo entrepreneur sporting a crazy idea—stranded gas powering Bitcoin mining rigs. We never pulled the trigger, but he pivoted that little gas-to-bitcoin operation toward AI computing instead. The next thing we knew, his startup was a unicorn—and he’ll probably make a guest appearance in the next Mountainhead movie (highly recommend, by the way).

I share this story not just for nostalgia, but to underline how bizarrely intertwined AI and conventional energy have become. Three years ago, it was quirky, speculative territory; today it’s core infrastructure. EQT—America’s largest natural gas producer—is quietly cementing its vertical integration by becoming the premier power supplier for AI-driven workloads. CEO Toby Rice recently let slip that EQT is negotiating a dozen gas-fired projects in Appalachia, projecting a staggering 6–7 Bcf/d of demand by 2030. Why Appalachia? Simple market physics: when $5 billion of pipeline infrastructure evaporates under regulatory heat, data centers migrate to the gas, not the reverse.

Meanwhile, NVIDIA reported earnings last week. It didn’t just clear expectations—it cemented itself as the most reliable bellwether of the AI power economy. Their Data Center segment alone clocked $22.6 billion in revenue last quarter, tripling year over year. CEO Jensen Huang didn’t give an earnings call. He issued an energy policy. He described “AI factories”—sovereign-scale deployments of NVL72 racks, each pushing 130 terabytes per second, drawing 30–50 kW per rack, deployed by the thousands. Hyperscalers are scaling power demand by the gigawatt, and doing it weekly.

This isn’t theoretical futurism—it’s physical load growth, already being invoiced.

The kicker? NVIDIA’s GPU stacks and EQT’s gas turbines are converging—opposite ends of the same infrastructure trend. One is arming the gold rush. The other is supplying the fuel. Forget crypto volatility or hydrogen’s promissory notes—this isn’t a bubble. It’s a freight train with power purchase agreements.

So, the question isn’t whether AI-driven energy demand is real. The question is whether you’re content watching from trackside—or savvy enough to start laying rails ahead of the locomotive.

And maybe—just maybe—you’ll find yourself accidentally creating a unicorn along the way.

I”EEEEHHH”PA and OCTG

In a ruling last week, the U.S. Court of International Trade took an axe to the Trump-era “Liberation Day” tariffs—well, most of them. This wasn't shocking. The legal justification for these levies hinged precariously on IEEPA, an old-school Cold War statute granting expansive presidential authority during a "national emergency." That emergency? America’s chronic, decades-long trade deficit.

Yes, seriously.

The court sensibly concluded that a condition persisting for over thirty years hardly constitutes a sudden crisis. Even had IEEPA passed muster, the nondelegation doctrine posed another formidable hurdle. That leaves tariffs under Sections 232 and 301—covering steel, aluminum, and autos—as firmly entrenched realities. In other words, the inflationary fog enveloping U.S. supply chains isn’t clearing anytime soon.

Which inevitably leads us back to oil and gas.

Across basins, well designs vary significantly, yet a consistent and crucial figure emerges from the data: Oil Country Tubular Goods (OCTG) account for roughly 13% of total drilling and completion (D&C) costs. That’s not trivial—it's a direct hit to breakeven economics. Every policy ripple cascades directly into cash flow per lateral foot.

The Q1 earnings cycle wasn’t screaming this message, but if you listened closely, the signal was unmistakable.

Consider Tenaris, the OCTG titan, which delivered an EBITDA margin uptick to 24% driven by solid operational performance and higher volume absorption. Yet beneath the headline lurks complexity: despite higher volumes, Tenaris's sales dipped 15% year-over-year due to declining average selling prices driven by shifting product mixes and softened demand in key markets like Mexico and Saudi Arabia. Furthermore, Tenaris flagged a $70 million quarterly tariff impact on steel billet imports, squeezing margins even as international pricing remains robust.

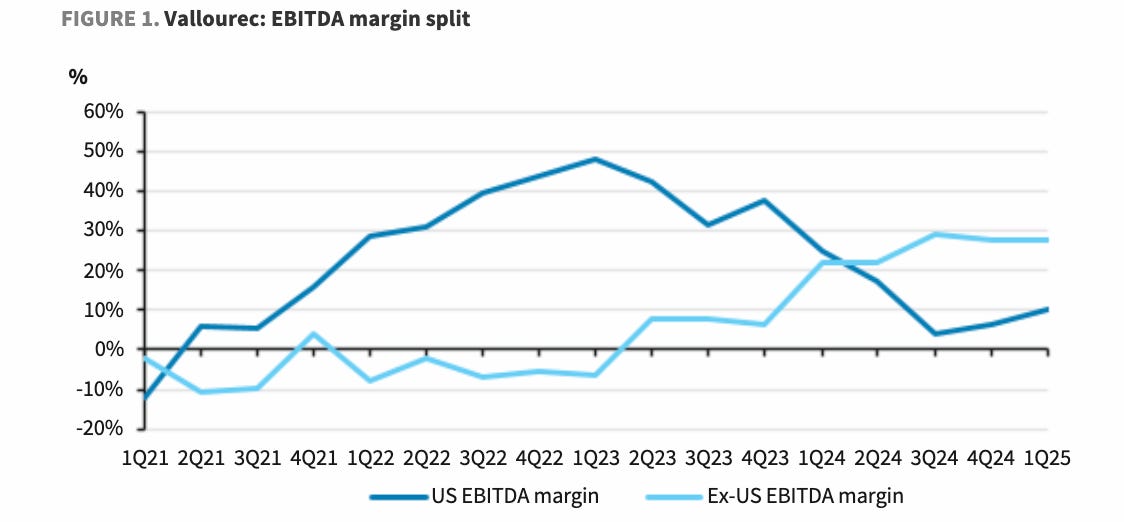

Meanwhile, Vallourec painted a similar narrative: EBITDA down 12% year-over-year, pressured by a 9% price drop in tubes despite higher shipments. Vallourec has strategically positioned itself by exiting lower-margin European markets and reinforcing premium segments in Brazil and Asia. Their robust Q1 free cash flow of €146 million and achieved net cash position ahead of schedule indicate strategic agility—but also underline the price pressures rippling through the U.S. market.

Why is this crucial? Because these tariff adjustments aren’t simply bureaucratic noise—they represent a tangible shift in pricing power. North American OCTG buyers, bound to Rig Direct models and long-term contracts, now face inflexible pricing structures precisely as input costs begin to climb and global supply pivots toward higher-margin offshore and LNG infrastructure projects in Africa, the Middle East, and Europe.

Indeed, Vallourec's recent emphasis on premium positioning—with average selling prices rising 16% to $3,153 per ton against a backdrop of a 40% drop in broader U.S. market pricing—reflects not just strategic execution but also a pivot away from commoditized onshore plays towards resilient, higher-margin segments.

Bottom line: OCTG dynamics have fundamentally shifted. The recent court decision wasn’t about completely rolling back tariffs; it merely relocated authority back to Congress, perpetuating uncertainty. Steel prices, however, are unforgiving of ambiguity.

Next week, we delve deeper: OCTG cost modeling, vendor leverage strategies, and concrete actions to optimize cash flow for the second half of 2025. Here's your key takeaway:

When tubulars consume more than a tenth of your D&C budget, tariff tremors aren’t mere background noise—they're crucial indicators of impending margin pressure. And this isn't about predicting every legal twist—it's about understanding how pricing power moves. Right now, it's migrating offshore and abroad, flowing into suppliers whose business models resemble premium tech more than traditional steel—think Apple rather than U.S. Steel.

More next week. Bring your casing specs.