Nominally Hedged | November 2025: Excel Rules Everything Around Me

How index funds, passive flows, and one little spreadsheet cell might be quietly rebuilding Standard Oil

When The Office premiered my junior year of high school, I didn’t get it. The awkward pauses and paper-company mundanity just seemed boring. Only after graduating from Penn State and joining ExxonMobil, where corporate quirks are not satire but lifestyle, did the show start to feel like a documentary.

Every workplace has that one person who genuinely enjoys the tasks everyone else avoids. (See Angela and her pathological enthusiasm for party planning.) Kalibr is no different. Keith finds serenity in scraping and cleaning obscure datasets for BATNA models. I read 10-Ks and academic finance papers for fun. We still have no Angela.

My favorite papers are the ones that reveal capitalism’s internal contradictions, the places where something can be both pro-market and quietly anti-market at the same time. Like saying you love football but being a Penn State fan.

Index funds are the purest version of that paradox. On one hand, they democratized investing: low fees, broad access, compounding for everyone. On the other, when BlackRock, Vanguard, and State Street collectively control roughly a quarter of the voting power in the S&P 500, competition starts to look more like coordination. The system that was meant to reward rivalry now owns all the rivals. Whether that counts as anti-competitive is a question best answered via séance with Adam Smith, but it raises another: what other side effects come from turning markets into indexes?

The investor’s nightmare is correlation, everything falling together. We pay up for assets that refuse to cooperate. That is why people buy pediatric dental practices in Utah, or gold bars, or Bitcoin. Not because they love molars or shiny rocks, but because they want their portfolio to misbehave. In theory, companies with uncorrelated returns should enjoy a lower cost of capital and more room to invest. In practice, ETFs tend to flatten those distinctions.

In 2025, the “ETFication” of everything means stocks move together not because their businesses do, but because their shareholders do. The market itself has become the benchmark.

That brings me to a clever paper by Christian Kontz and Sebastian Hanson, “The Real Cost of Benchmarking.” It shows what happens when everyone’s spreadsheet starts talking to each other.

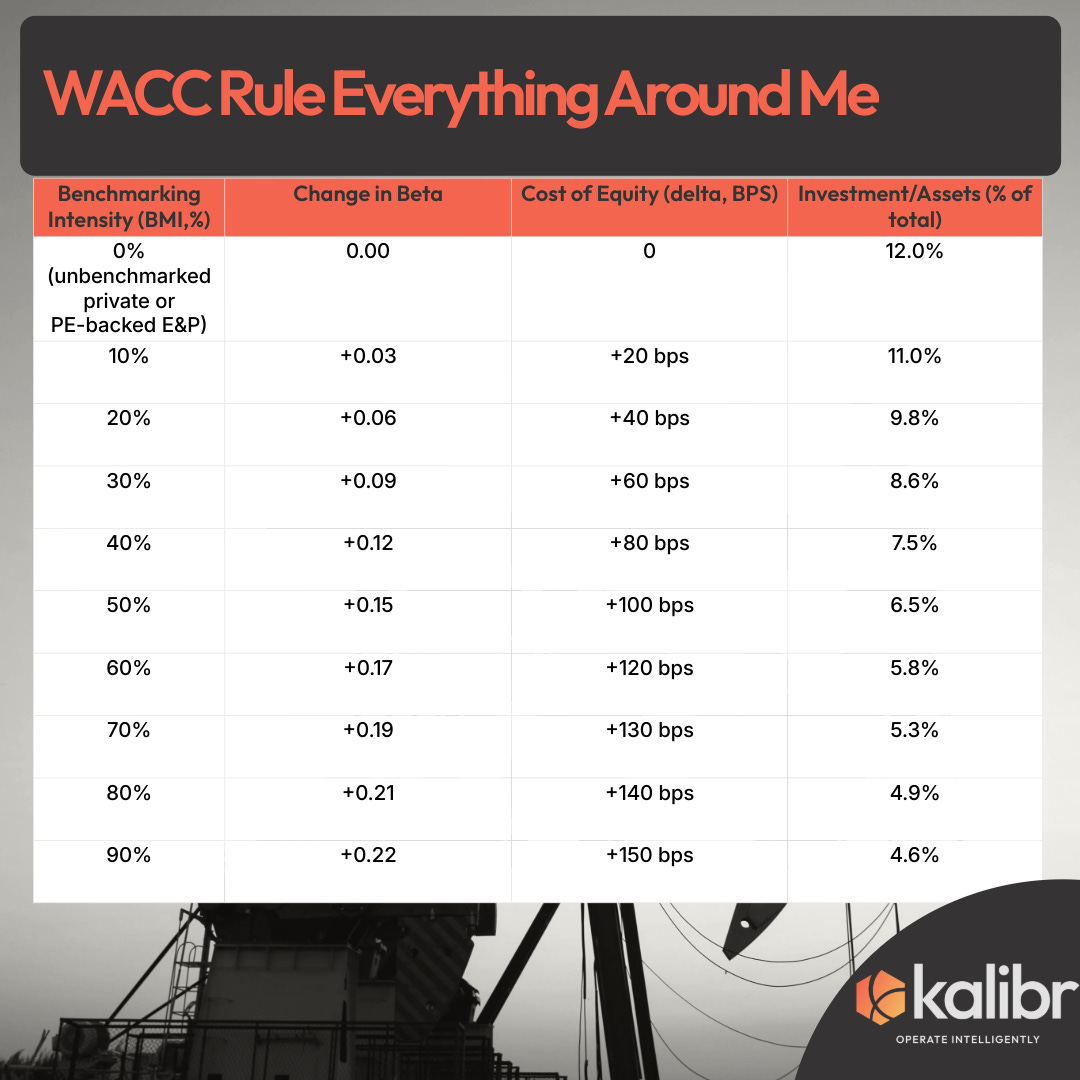

1. Benchmarking raises beta.

A ten-point increase in benchmark-linked ownership (ETF or index funds) mechanically lifts a company’s measured CAPM beta by 0.1 to 0.12. Translate that through the finance-bro spreadsheet and you get roughly 60 to 80 basis points higher perceived cost of equity.

2. Managers believe the spreadsheet.

CAPM never mentions index funds. It says cost of capital depends on the risk-free rate, the market premium, and beta. Nothing about Vanguard. But CFOs do not argue with Excel. When benchmarking raises beta, the model says capital just got more expensive. Kontz and Hanson find that a 20-point increase in benchmarking intensity corresponds to about a 25 percent decline in investment (CAPEX to assets) relative to peers.

As Wu-Tang once said, Excel rules everything around me.

3. Investment falls, payouts rise.

The same firms that cut CAPEX boost dividends and buybacks by roughly 250 basis points of assets over the next five years. Every extra dollar of benchmarking turns into a dollar of “return discipline.”

4. The effects linger.

The beta shock and investment drought last five to seven years after index inclusion. The one-time stock pop fades, but the CFO’s WACC cell stays haunted.

5. Capital-intensive sectors suffer most.

Energy, utilities, and manufacturing show the steepest decline. Benchmarking depresses investment most where long-cycle projects actually matter.

6. Regulators follow the same math.

Even in regulated utilities, the effect holds. A ten-point rise in benchmarking intensity leads to roughly 70 basis points higher allowed cost of equity in rate cases. The spreadsheet is steering regulators as well as CFOs.

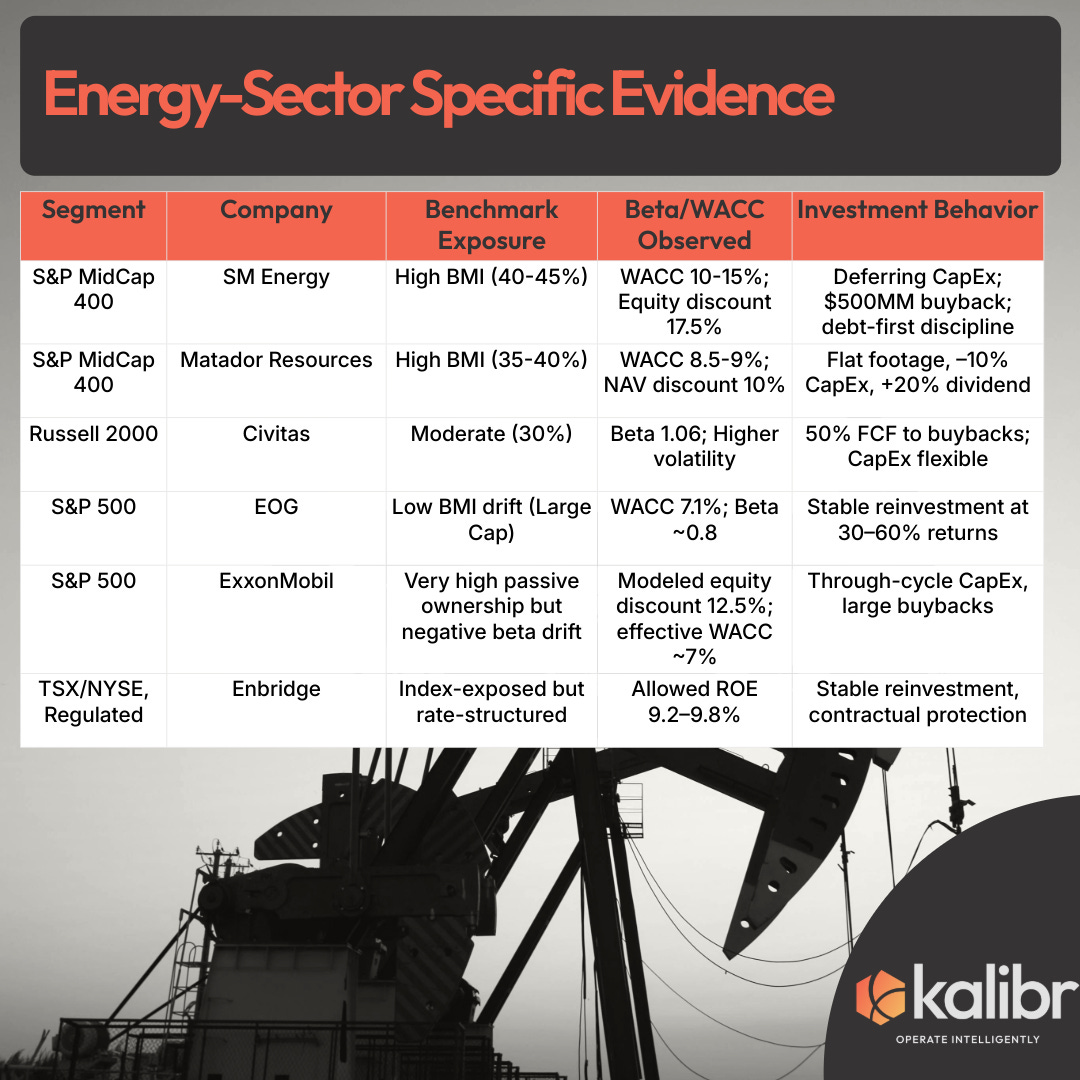

So what does this mean for energy?

Small and mid-cap E&Ps, especially those in indices, are being nudged toward short-cycle projects and higher payouts. Rising measured beta means a higher WACC, which means fewer projects clear the hurdle rate. Dividends and buybacks, conveniently, always do.

The majors can exploit this sameness. Their balance sheets and portfolio depth let them keep investing while everyone else worships the spreadsheet. It is not necessarily that their geology is better; it is that their covariance matrix is friendlier.

All this adds to the structural drag already weighing on CAPEX: geological decline, investor pressure for cash, and the slow erosion of long-cycle conviction. Indexation is the invisible hand that quietly presses the “merge” button.

My view: this is another accelerant toward consolidation in North American energy. The irony is neat. The same mechanism that made investing democratic is pushing us back toward concentration.

Indexing makes capital cheap but originality expensive. The median driller optimizes for being ordinary, because ordinary is what the index rewards and what the CAPM punishes the least.

The market is teaching companies to be generic, and charging them extra if they resist. And as long as CFOs cling to their WACC cells the way Angela clings to her party-planning rules, consolidation will keep winning.