Nominally Hedged | June 25th, 2025

RFPs, ROFRs, and Why HHI Isn’t Just for Antitrust Lawyers

Thinking in Options, Not Opinions

There’s a small stable of books I revisit each year. One of them is Thinking in Bets by Annie Duke. It’s full of useful mental models — from avoiding “resulting” to properly interpreting probabilities (a 3% chance doesn’t mean “never,” it means 3 out of 100 times, this should happen).

But the idea I come back to most is this: make bets, not assertions. In other words, if you want to know how likely something is, don’t ask for someone’s opinion — ask what they’re willing to wager.

That idea has gotten a lot more literal in 2025. Platforms like Polymarket let you see — in real time — what the crowd is pricing for events as serious as the presidential election and as speculative as the return of Jesus (3% odds, if you’re curious).

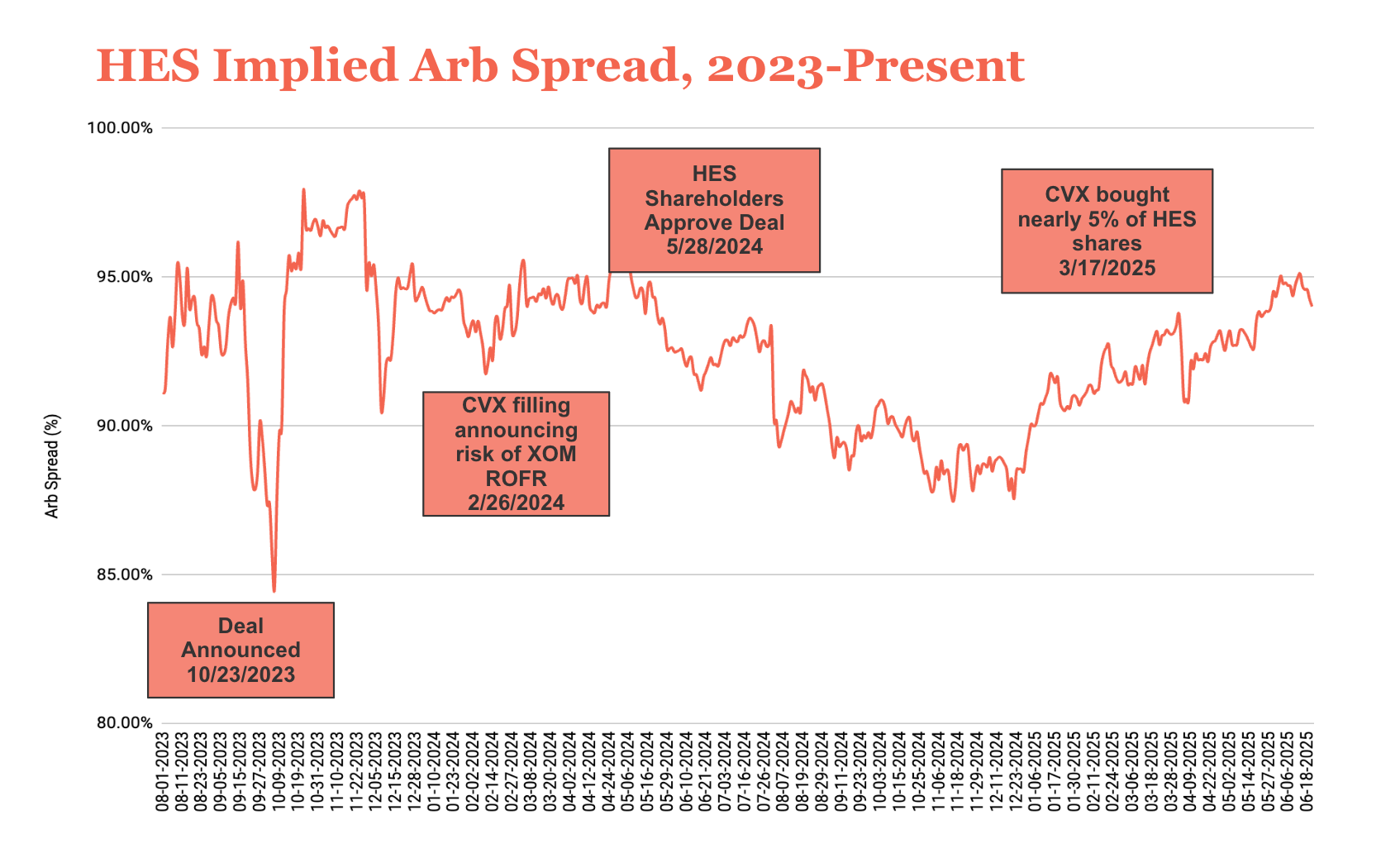

Financial markets offer the same insight, with higher stakes. Take the Chevron-Hess merger.

Back in May, both companies met in London for arbitration over whether Exxon’s ROFR in Guyana applies to full-blown corporate mergers. If the panel sides with Exxon, the deal dies. If not, it closes.

Here’s what I wrote on May 8th:

At the time, the spread on the CVX-HES all-stock deal hovered around 7–9%. That’s wide for a megacap merger with minimal regulatory overhang. Translation: markets were pricing in real disruption risk.

Let’s walk through the mechanics. The original deal offered HES holders 1.025 CVX shares — a 10.3% premium at announcement. So:

Bet deal goes: buy HES / short CVX

Bet deal fails: short HES / go long CVX

Interestingly, Chevron itself bought ~5% of Hess shares in March — a public show of confidence. And since then, the arbitrage spread has compressed. The market now leans toward a successful close.

But that doesn’t mean Exxon made a bad call. This is where Annie Duke’s concept of “resulting” comes in — judging decisions by outcomes rather than process.

To analyze it properly, we need another market metaphor: options.

What’s the cost of Exxon’s challenge? Legal fees and some reputational friction. That’s the premium.

What’s the payoff? Blocking a major rival acquisition and potentially buying Hess at a discount. That’s the upside. If the option was cheap — and it was — you take that trade every time.

The smartest companies treat contracts like portfolios — embedded with options that don’t pay out 99 times out of 100, but when they do, they’re asymmetric. You negotiate those options at time zero, when your leverage is highest.

We’ll have to wait until August to see how this one closes. Personally, I wouldn’t be surprised if Exxon extracts some value in arbitration even if the deal goes through — a concession, a precedent, or simply leverage cashed in later.

But the broader point holds: this industry is stretched thin — a mosaic built from hundreds of negotiated outcomes. Before you strike a deal, step back. Simulate a few scenarios that are high-value but low-probability. Then bake in the mechanism that lets you capture that upside if the ticket ever comes due.

It’s not about guessing the future. It’s about owning the option.

Kalibr helps oil & gas companies optimize Drilling, Completions, and Production operations to reduce cost, improve capital efficiency, and accelerate cash flow.

We combine engineering expertise with sourcing strategy and negotiation science to uncover hidden value across vendors, contracts, and execution plans — then partner with your team to capture it, fast.

RFPs Are for Leverage, Not Just Logistics

It’s nearly our favorite time of year at Kalibr: RFP season. That magical window when Oil & Gas companies begin 2026 planning and dust off their sourcing strategies.

We’ve led vendor selection and RFP processes across nearly every major energy vertical — and we have strong opinions. In fact, we’d argue most RFPs are designed for the wrong purpose.

Here’s the Kalibr view: RFPs aren’t about selecting a vendor. They’re about manufacturing a BATNA.

That framing changes everything.

Let’s start with segmentation. Every item on your LOE and AFE should be categorized — ideally through a structured vendor strategy lens. At Kalibr, we break these into strategic and non-strategic. Strategic categories — the “heavy hitters” like frac, sand, OCTG — demand a more advanced sourcing playbook. Why? Because cost isn’t the only variable. Strategic categories often drive operational uptime, safety, or productivity, which means your comparison set needs to normalize far more than price.

The mistake many teams make is treating RFPs like bid boards: send specs, collect responses, pick a winner. But when you use an RFP to award work instead of build leverage, you miss the biggest benefit of the process — optionality.

Let’s break this down:

The RFP is your sales pitch.

You’re not just evaluating suppliers — you’re marketing yourself as a buyer worth competing for. What’s your value prop? Payment speed, volume visibility, long-term partnership? Craft it like you would a term sheet to a JV partner.

It’s a tool for building actionable alternatives.

That word — actionable — matters. Alternatives aren’t helpful unless they’re credible. If one vendor is cheaper but carries QA/QC risk, use the RFP to get detailed on their equipment, uptime, redundancy plans. Turn a risk into a negotiable lever.

It’s a diagnostic tool.

You should be running your own vendor intelligence system (we call ours VSI), and the RFP is a way to confirm or challenge what you think you know. Have a hunch Vendor A is stretching capacity? Ask about crew allocation, lead times, failure rates. Make the ambiguity work for you.

This approach takes more effort upfront. You need to expand the funnel — include out-of-basin providers, new entrants, even the “long shots.” But in doing so, you create real choices.

When it’s time to negotiate, bring 2–3 vendors to the table. Sequence matters: start with the weakest, end with the incumbent. Each negotiation is not just about price — it’s about pressure-testing value. Can your low-cost vendor become credible with better uptime guarantees? Can your highest-quality provider compete on net value once you expose their peers’ pricing structures?

Our clients routinely find 10–15% more total cost savings — not just bid cost — by pushing past RFP selection and into structured negotiation.

The point isn’t to pick a winner. It’s to shape a game you can’t lose.

So before you hit send on that next RFP, ask yourself: Is this a selection tool — or a source of leverage?

Case Study: Unlocking $17.5M in Frac Savings Through Data-Driven RFP Strategy

Client: Leading Private E&P – Rockies Basin

Context: Heading into 2025 planning, the client intended to renew their incumbent frac provider based on historical performance and perceived reliability.

Challenge:

A sole-source mindset left the client blind to shifting market dynamics. Despite a rapidly softening frac market, internal teams lacked visibility into changing cost structures and competitive capacity — leaving tens of millions on the table.

Kalibr’s Approach:

Rather than rubber-stamp the renewal, Kalibr deployed a three-pronged intervention:

Market Intelligence Activation

Using proprietary vendor and market intelligence, Kalibr surfaced leverage the client hadn’t seen — including increased regional capacity and pricing compression among Tier 1 providers.

TCO Normalization via Custom RFP Design

Kalibr rebuilt the client’s RFP framework from the ground up, standardizing bids not just on cost, but also on safety, quality, and operational uptime — enabling apples-to-apples comparisons and exposing hidden inefficiencies.

Negotiation Sequencing with MESOs

Leveraging Kalibr’s Strength Index, we optimized vendor negotiation order and constructed Multi-Equivalent Simultaneous Offers (MESOs) that unlocked new value levers beyond price — including redundancy guarantees and performance metrics.

Results:

$17.5M in Total Savings (~25% of 2025 frac budget)

Performance-Based Contract with the lowest-cost vendor — without compromising service reliability

Data-Driven Deal Architecture that replaced heuristics and legacy bias with measurable, defendable commercial logic

Why It Matters:

This wasn’t a story of switching providers. It was a case of upgrading the process — turning an RFP from an administrative formality into a strategic asset. The result? A deal structure that expanded optionality, protected operations, and delivered material value to the bottom line.

Pressure Pumping: To RFP or Not to RFP?

When operators are satisfied with their incumbent frac provider, they often ask us: Should we RFP or just cut a deal directly?

At Kalibr, the answer is: it depends.

And that “depends” isn’t a shrug — it’s a score. Specifically, your Best Alternative to a Negotiated Agreement (BATNA), and more importantly, the vendor’s.

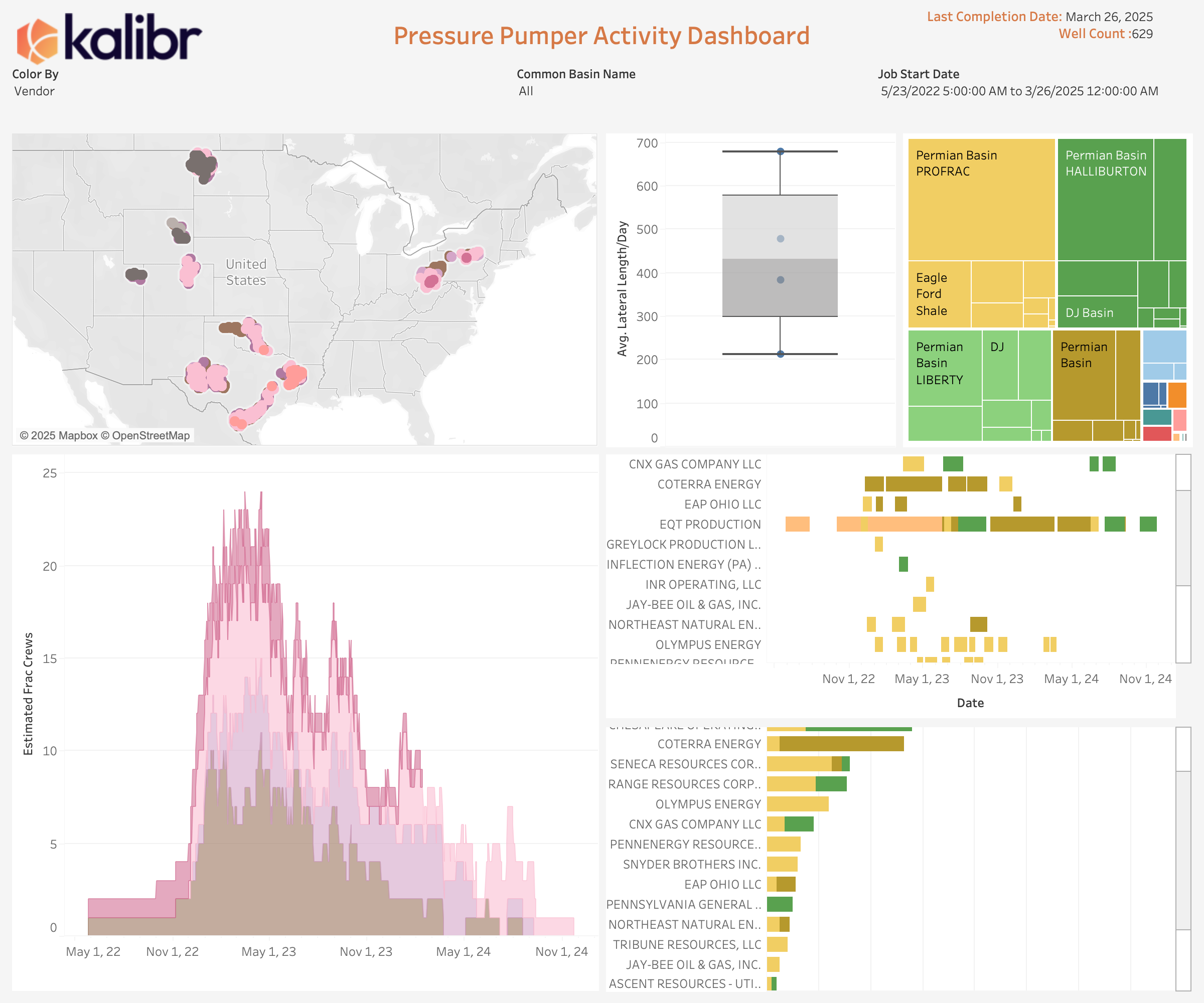

In pressure pumping, leverage is everything. Our market intelligence stack was built to quantify it.

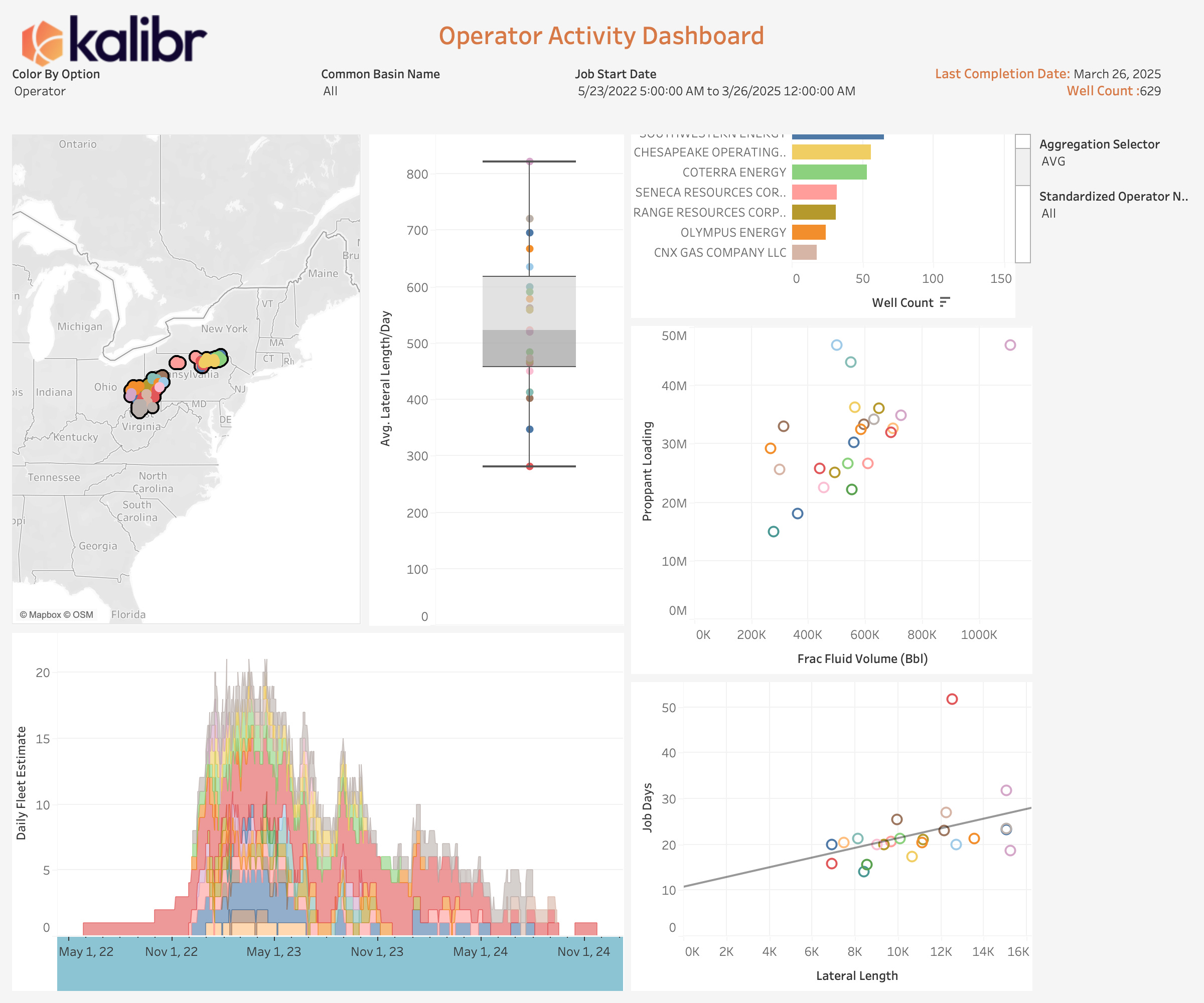

Step 1: How Valuable Are You to Them?

We start by assessing how strategically important your basin is to the vendor. Are they deeply entrenched? Are they running hot in your backyard or just passing through? The more they rely on your program to keep assets spinning, the stronger your hand.

Our Operator Activity Dashboard maps pumping intensity across time and space — pulling metrics like program stability, pumping days, and pad density to show how you stack up versus peers. Vendors don’t just want volume; they want predictability, pad complexity, and operational rhythm.

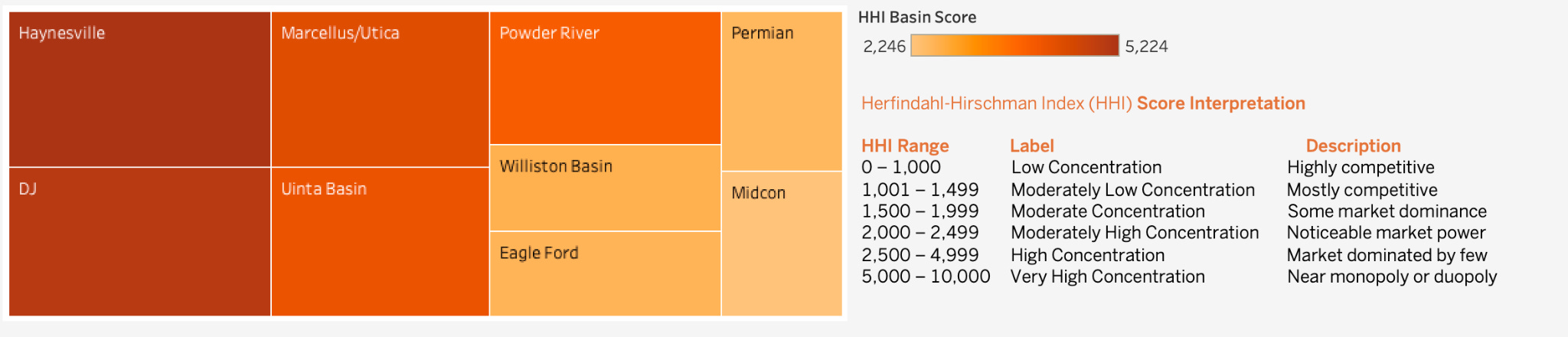

Step 2: How Competitive Is Your Basin?

Here we bring in the Herfindahl-Hirschman Index (HHI). A high HHI? Few vendors, limited options. A low HHI? Fragmented landscape, more room to play.

Haynesville and DJ? Concentrated.

Permian and Eagle Ford? More open.

Knowing where your basin falls tells you if competition will move the needle — or just waste your time.

Step 3: What’s the Macro Telling Us?

Even strong incumbents wobble under the right market pressure. We track vendor utilization, revenue exposure, and redeployment trends. Are fleets retiring or reactivating? Are vendors consolidating footprint?

If your vendor is stretched thin — or leaning heavily on your work to cover costs — you may not need an RFP to win concessions. You may just need timing.

Step 4: Are You a Buyer Worth Fighting For?

Do you bring stable demand, clean ops, and complex jobs that optimize crew hours? If yes, vendors will fight to keep you.

Our Vendor Strength Index (VSI) pulls it all together — scoring each vendor-basin pairing to show where you hold leverage and when to press.

If your incumbent has the lowest VSI in the mix? Go direct.

If others score lower? Time to run the playbook.

So no, the question isn’t “To RFP or not?”

The real question is: Do you have the data to know?

Thanks for reading.

We built Kalibr to arm operators with the data, strategy, and leverage to win — not just negotiate.

If this sparked a thought, challenged a belief, or made you want to run your own Vendor Strength Index…

→ Hit reply or drop a comment. We’d love to hear how you’re navigating pressure pumping decisions.

Until next time —

The Kalibr Team