Nominally Hedged: For Want of a Crankshaft

The compression industry’s engine problem isn’t a Caterpillar problem. It’s a metallurgy problem, and it’s not getting better for three years.

Suppose there is one engine and two buyers. The engine goes to whoever loses more by not getting it.

That’s it. That’s the whole mechanism behind 180-week lead times, tripled backlog, and the most dislocated equipment market in the history of gas compression. One engine, two buyers, and the uncomfortable math of what’s waiting on the other side of the purchase order.

Buyer one is a hyperscaler. The engine unlocks a GPU cluster that earns money by the hour the instant it switches on. TD Cowen estimates these buyers routinely pay $1 million to $2 million per megawatt for behind-the-meter generation, and up to $3 million to $5 million per megawatt for islanded configurations that bypass the grid entirely. The engine is a rounding error on a $10 billion campus.

Buyer two is a compression operator. Not the same engine, technically. The compressor driver and the generator set are different configurations. But they share the same block casting, the same crankshaft forging, the same production line at Lafayette, the same 18-month queue. Caterpillar decides how many of each to build on that line, and the decision follows the money. The compression variant unlocks a contract priced at $25-31 per horsepower per month. One buyer’s rounding error is the other buyer’s entire capital budget.

Same line. Different engine. Wildly different thing waiting behind it.

The auction never measures the engine. It measures what’s behind it. The compression operator can be the most disciplined, rational, well-run buyer on earth and still lose every single time. He isn’t being outsmarted. He’s being out-staked.

Kalibr tracks every compressor unit across the Lower 48. Of new compression sets above 1,000 HP permitted in 2025, 85.2% were Caterpillar. Waukesha placed 11%. Cummins placed less than 1%. Waukesha’s 11% is the rounding error. Cummins’s share is a rounding error on the rounding error.

The wait-and-see instinct that has served compression operators for twenty years (order when you have the contract, manage working capital prudently, don’t get overextended) is now structurally the losing move. Not because the operator got less disciplined. Because the other buyer’s mistake can only ever be warm: over-order and the balance sheet shrugs, you’ve got backup power anyway. The compression operator’s mistake bites from both directions. Order early and you’re bleeding capex against demand that hasn’t shown up yet. Order late and the engine is 180 weeks out, sitting in line behind a data center, and you can’t serve the contract you just won. Prudence stops being a strategy and becomes a way to lose slowly.

The demand numbers are public. Caterpillar’s large reciprocating engine backlog has grown more than 3.5x since January 2024, to a record $62.7 billion across the enterprise. Power generation sales surged 41% year-over-year in Q1 2026. That number is correct. It is also the less interesting half. The auction logic tells you who wins the engine. The supply chain tells you why there’s an auction at all. There are exactly 33 facilities on earth capable of forging a crankshaft for a Caterpillar 3600-series engine. Zero domestic U.S. foundry capacity for large engine castings. Turbocharger superalloys competing for the same inputs as Boeing and Airbus. The binding constraint on Caterpillar’s engine output isn’t Caterpillar’s assembly lines. It’s a network of foundries, forging houses, and turbocharger specialists scattered across Brazil, India, Finland, and Japan.

Here is the part that is not in the earnings deck.

The Production Reality

Caterpillar does not disclose unit-level production figures for its G3500 and G3600 engine families. It never has. So you have to build the number yourself.

Start from the bottom up. Kalibr’s data shows three engine models account for 90% of every Caterpillar engine going into compression above 1,000 HP: the G3516 (40.6%), the G3608 (28.1%), and the G3606 (21.3%). Everything else is rounding. The compression industry’s Caterpillar dependency is actually a three-engine dependency, which means the engine allocation question everybody is trying to answer really comes down to: how many G3516s and how many G3606/8s does the compression channel get?

Now work from the top down. Jefferies Research estimates that Caterpillar currently produces 1,500 to 2,000 large reciprocating engines annually, with the capacity expansion at Lafayette projected to push that figure above 3,200 by the end of the decade. RBC Capital Markets breaks the P&E segment revenue into its components: the 22% year-over-year growth in Q1 2026 was driven by a 14.5% increase in physical sales volumes and a 1.9% price realization premium. That 14.5% volume growth, applied to the Jefferies baseline, implies mid-single-digit unit growth in the trailing twelve months. Caterpillar is making more engines. The compression industry is getting fewer of them.

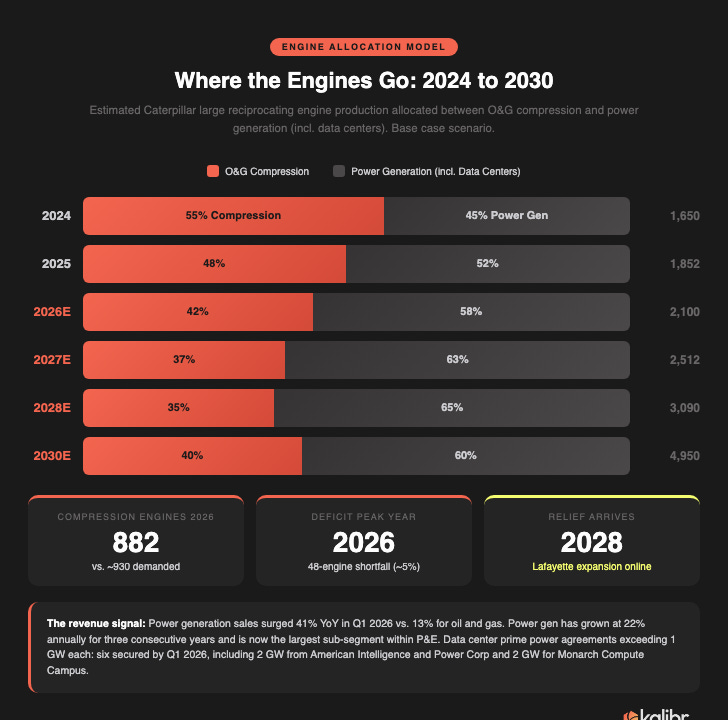

Our midpoint: 1,650 large reciprocating engines rolled off Caterpillar’s lines in 2024. In 2026, with the initial phases of the Lafayette expansion contributing efficiency gains (new automated crank milling equipment replacing 40-year-old machines, reducing operator requirements from 30 to 8 per station), that number rises to 2,100.

The question is where those 2,100 engines go.

The Allocation Shift

Historically, Caterpillar’s large engines were split roughly evenly between oil and gas applications (compression, well servicing, drilling) and power generation (prime power, backup, distributed). That balance has broken.

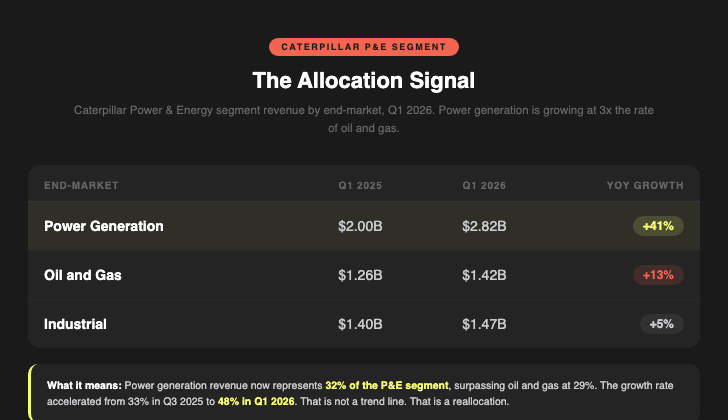

Power generation is growing at three times the rate of oil and gas. RBC Capital Markets reports that power generation has become the largest component of the Power & Energy segment, at 32% of total revenue in 2024, surpassing oil and gas at 29%. The trajectory is clear: in Q3 2025 the power gen growth rate was 33%. By Q1 2026, it was 48%. That is not a trend line. That is a reallocation.

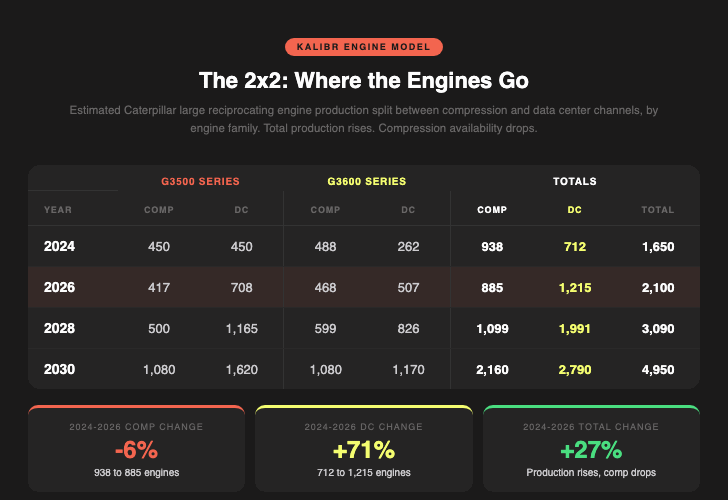

The allocation shift hits the two engine families differently. The G3500 series, particularly the G3516H (Caterpillar’s dominant 1.9 MW data center genset), sees its DC allocation rise from 50% to 70% at peak in 2028. The G3600 series crosses from compression-majority to DC-majority in 2026. It never fully tips back. USA Compression’s management confirmed this on their Q1 2026 earnings call: Caterpillar has no major plans to expand manufacturing for the 3600-series engines used in gas compression.

Our unit model estimates the 2x2 split:

Total production rises 27%. Compression availability drops 6%. The allocation shift eats the entire gain.

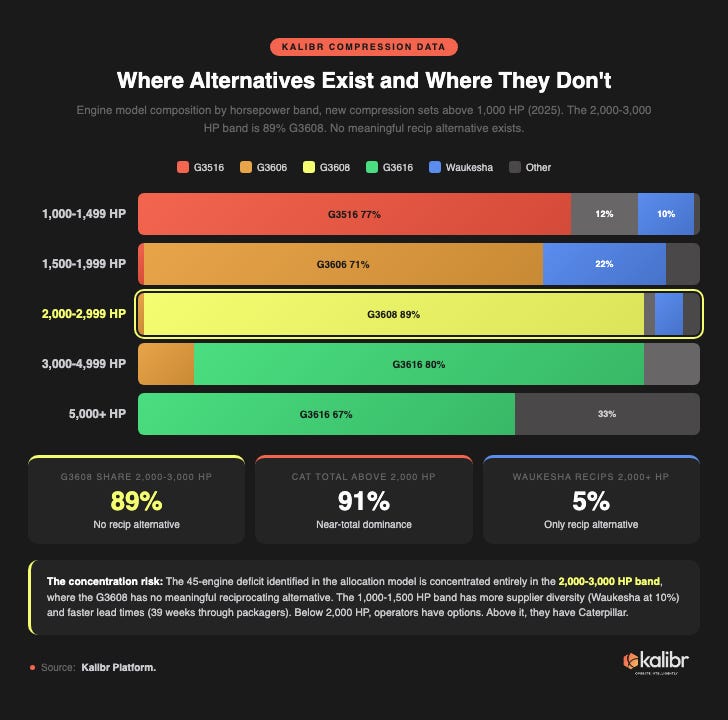

For the compression channel, the arithmetic is straightforward. If Caterpillar produces 2,100 large reciprocating engines in 2026, and 58% go to power generation, the compression channel gets 885 engines. Total compression demand sits around 930 engines. That’s a 45-engine deficit, roughly 5%, which doesn’t sound catastrophic until you realize that the deficit is concentrated almost entirely in the 3600 series, the 2,000 to 5,000 HP class that is the backbone of midstream compression.

Kalibr’s data shows why that concentration matters. In the 2,000 to 3,000 HP band, the G3608 is 89% of all new compression sets. Above 2,000 HP, Caterpillar’s total share is 91%. The only reciprocating alternative is Waukesha, at 5%. The 45-engine deficit is not spread across a market with substitutes. It is concentrated in the one horsepower band where substitutes do not exist. All the revenue triangulation and capacity estimates above come down to one engine model in one horsepower band. Whether those engines compress gas or generate electricity for a data center is not a Caterpillar decision. It is a price discovery. And the data center will always pay more.

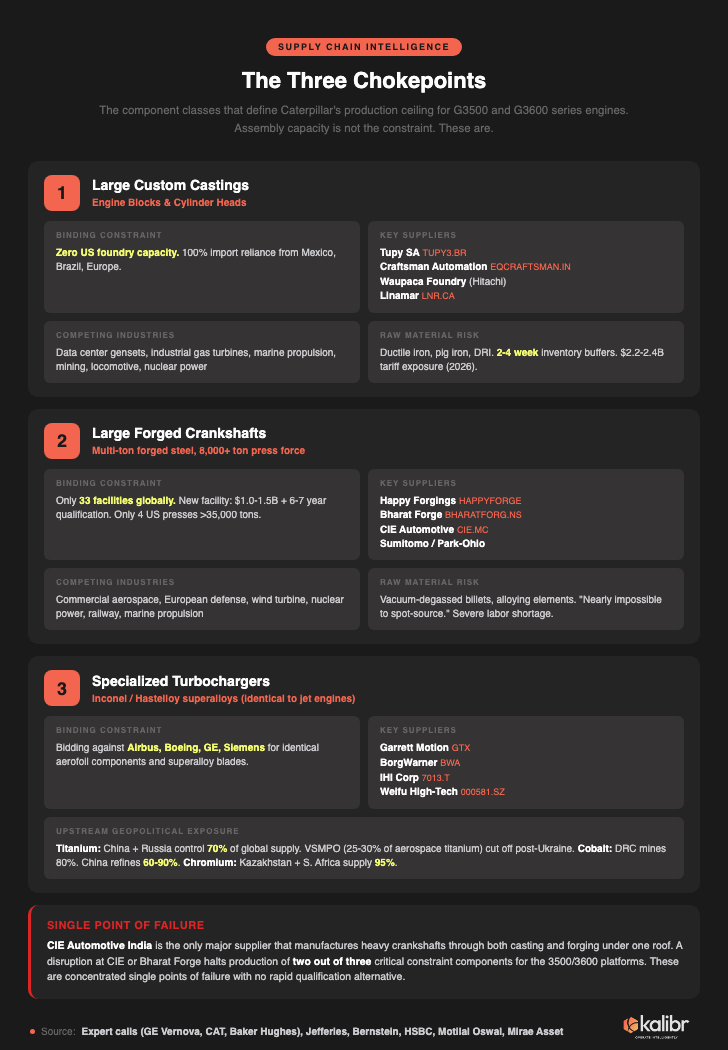

The Three Chokepoints

Caterpillar announced a $725 million expansion of its Lafayette, Indiana Large Engine Center. Wall Street celebrated. The stock moved. Then someone asked where the crankshafts come from.

Here is what $725 million actually buys. The Lafayette footprint is growing by about 400,000 square feet, a 30% increase to the existing 1.7 million square feet. The other 95% of the 125% capacity increase comes from replacing 40-year-old machining equipment with modern automated systems and debottlenecking internal production flow. Bernstein Research walked the facility and reported the details: new automated crank milling equipment that reduces the operator count from 30 to 8 per station, modernized boring equipment for cylinder blocks, upgraded quality control systems.

Caterpillar is not building a new factory. It is modernizing an old one. And the binding constraints on its output are not inside Lafayette. They are upstream, in the foundries and forging houses that supply the raw castings, forgings, and turbocharger components that Lafayette machines and assembles.

Caterpillar management has been explicit: increasing total throughput is “highly dependent on bringing the external supply base along” with internal facility expansions (which is a polite way of saying: we can build engines as fast as Brazil can cast engine blocks, and not one unit faster). They’ve dedicated significant resources to working with Tier 1 and Tier 2 suppliers on synchronized ramp-ups.

The three component classes that define the production ceiling:

1. Large Custom Castings

Every G3600 engine starts as a multi-ton iron casting: the engine block and cylinder heads. These castings require specialized ductile iron grades, massive high-precision vertical machining centers (only a handful of machine tool builders globally manufacture equipment large enough to process 3600-series blocks), and deep metallurgical expertise.

The United States has zero domestic foundry capacity for these parts. Zero. Every cast iron engine block and cylinder head that goes into a Caterpillar 3500 or 3600 series engine is imported, primarily from Brazil, Mexico, and Europe.

Tupy SA, the world’s largest iron foundry (748,000 tons per year across plants in Brazil and Mexico), is the dominant Tier 1 supplier. Bradesco Corretora estimates that 70% of the medium and heavy truck fleet in the United States uses engine blocks manufactured exclusively by Tupy. For large industrial engines, the supply base narrows further: Craftsman Automation in India, Componenta in Finland, Linamar in Canada, Anhui Yingliu in China. Five foundries, four continents, and zero domestic capacity. The entire domestic heavy truck fleet and the entire large engine industrial base, dependent on a single Brazilian foundry most Americans have never heard of.

Craftsman Automation is building out its Kothavadi foundry in India (it acquired Germany’s Fronberg Guss GmbH to scale from 100-kilogram to 3-tonne components). The new capacity comes online in FY2029. Three years from now. And the order book? Linked primarily to data center power generation demand. Not compression.

The competing demand for large engine block casting capacity: data center backup power generators (directly competing for identical castings), industrial gas turbines (consuming complex casting slots through 2028), marine propulsion engines, mining equipment, and locomotive engines. Every one of these industries is spending at record levels.

2. Large Forged Crankshafts

The crankshaft is the most mechanically stressed component in a reciprocating engine. For the 3600 series, these are multi-ton forged steel assemblies produced on hydraulic or mechanical presses exceeding 8,000 tons of force.

The entire global capacity for large hydraulic forging presses capable of producing these components: 33 facilities. If you decided today to build a new one, you would need $1.0 billion to $1.5 billion for three additional press lines, two years of feasibility studies, and a 6-to-7-year qualification process before a single production crankshaft ships. That puts you in 2034. You would be making crankshafts around the time the current supply crisis has already resolved itself. In the United States, Howmet Aerospace has noted that only four presses exceeding 35,000 tons exist in the entire country.

The key suppliers: Happy Forgings in India (commissioning a new 14,000-ton press, one of only a handful globally with this specific capability), Bharat Forge (large open-die presses, recently diversified into casting via its JS Autocast acquisition), Sumitomo Corporation of America (leading North American supplier), and Park-Ohio Industries (specialized finishing and machining).

CIE Automotive India is the only major supplier capable of manufacturing heavy crankshafts through both casting and forging processes simultaneously. Which makes it either impressively efficient or terrifyingly concentrated, depending on whether you are writing a supplier brochure or a risk assessment. A power grid failure, labor strike, or regional scrap steel shortage affecting either CIE or Bharat Forge would immediately halt production of two out of three critical constraint components for the 3500/3600 platforms.

The competing demand: commercial aerospace programs (monopolizing critical press time for landing gear and structural forgings), surging European defense spending, wind turbine components, nuclear power industry, and railway. All of these industries are fighting for the same finite set of heavy forging presses. All of them are in upcycle. Nobody is waiting.

A former Caterpillar marketing professional told an expert network that critical components like crankshafts have become “nearly impossible to source in the spot market, creating a fragile environment where any minor disruption causes compounding delays.”

3. Specialized Turbochargers

Turbochargers for the 3500 and 3600 series engines operate in an environment most machine shops refuse to enter. The hot section (turbine wheel and housing) is exposed to extreme exhaust temperatures and immense rotational speeds, requiring specialized superalloys: Inconel 718, Hastelloy, Waspaloy. These are the same materials that go into jet engine turbine blades. That is not a metaphor. It is the same alloy, the same specification, and in many cases the same foundry.

The turbocharger supply base is dominated by Garrett Motion (which recently launched its “MEG” very-large-frame turbochargers for industrial and marine applications) and BorgWarner (global market leader, now expanding into stationary power applications), with Japan’s IHI Corp and China’s Weifu High-Technology rounding out a supplier list that counts its members without needing a second hand.

Caterpillar’s turbocharger suppliers must bid against Airbus, Boeing, GE, and Siemens Energy for the exact same aerofoil components and superalloy blades. The rapid expansion of AI data centers has triggered what HSBC Global Investment Research calls a “super-cycle” for heavy-duty industrial gas turbines, and these turbines rely on the identical specialized inputs. Every turbocharger that goes into a Cat 3608 is a turbocharger that didn’t go into a GE gas turbine or a Pratt & Whitney overhaul kit.

China and Russia dominate the raw inputs. Russia’s VSMPO, which historically provided 25% to 30% of the aerospace industry’s titanium, has been effectively cut off since the invasion of Ukraine, forcing the Western industrial base onto Japanese sponge producers already running at capacity. Every turbocharger has a geopolitics problem baked into the alloy.

Garrett Motion’s experience is instructive. When the company attempted to source cast turbine wheels from an $80 billion global aluminum caster in China, the supplier “initially lacked the technical know-how to produce the part.” Garrett spent multiple years teaching the supplier-specific alloy recipes and machining techniques. Eventually, Garrett built its own captive casting facility to ensure supply continuity. An $80 billion company couldn’t make the part. That is the turbocharger supply chain.

What the Model Says

We built a model for Caterpillar’s G3500 and G3600 series engine production that starts from the only thing we can actually observe (P&E segment revenue) and works backward through four independent proxies to get to a number Caterpillar won’t give anyone.

The CAPEX Cross-Check

Caterpillar does not disclose unit shipments. But the public compression companies do disclose capital expenditure and HP additions. This proxy validates the model.

These four companies represent about 25% of the U.S. contract compression market by fleet horsepower. Scaling to the full market implies 872 engines of total compression demand. The model’s base case produces 885 compression engines for 2026. That’s a 1.5% delta to the packager proxy. Close enough.

The Raymond James cross-check arrives from the other direction. Their estimate of 26 Bcf/d of incremental natural gas production growth through 2030 implies 15 million additional horsepower, a 25% increase to the installed compression fleet. At 2,000 HP per engine average, that’s 1,500 engines per year. Our model assumes 1,050 engines of annual demand by 2030. If Raymond James is right, the compression deficit is deeper and longer than our base case projects. That is the model’s most conservative assumption.

The public packagers’ ordering behavior tells you who has already priced this in. USA Compression’s management has noted that their future orders are heavily weighted toward the G3600 series (Kalibr’s vendor-attributed permit data shows zero G3600-class units for USAC in 2025, consistent with Caterpillar’s reallocation away from compression). Kodiak has secured Caterpillar engine deliveries through 2028. Archrock has pre-contracted 85% of its 2026 new-build program.

The demand underpinnings are structural.