Nominally Hedged | DJ Basin Analysis: The Basin Nobody Wanted

Turns out you can't rationalize geology

There is a concept in corporate finance called the conglomerate discount. A company that owns a collection of unrelated businesses trades at a lower multiple than each business would command independently, because investors don’t trust management to allocate capital as well as the market would. The prescription is simple. Sell the non-core assets. Return the capital. Focus.

For the past decade, the Street has applied conglomerate discount logic to the Denver-Julesburg Basin.

Colorado was the non-core asset. Senate Bill 19-181 rewrote the state’s mandate from fostering energy development to aggressively regulating it. 2,000-foot setback rules. “Severe” ozone nonattainment classification. Permitting timelines of seven to eight months while Texas secured equivalent approvals in three days. Investors applied a “Colorado discount” to every DJ-weighted producer, demanding higher risk premiums and lower multiples. The prescription was the same one every activist gives every conglomerate: sell the DJ. Focus on the Permian. Simplify.

The echo for portfolio rationalization hasn’t stopped. Kimmeridge released a letter to Devon’s board just this week demanding “an accelerated program of non-core asset divestitures.” The playbook is evergreen. The logic is clean.

The conclusion might also be wrong.

The thing about conglomerate discount logic that nobody mentions in the activist presentation: the prescription assumes fungibility. Sell the “bad” asset, redeploy into something “better,” watch the multiple expand. This works precisely as long as “something better” exists. The Permian is running out of Tier 1 rock. Not catastrophically, but in the way that matters to anyone building a five-year drilling program: the next well is slightly worse than the last one. Bernstein called it in early 2026. Eagle Ford growth is unlikely through 2030. The Bakken is price-sensitive and declining. Delaware Basin productivity declined 6% year-over-year broadly, 15% for specific operators.

When the “better” alternative is deteriorating, the discount thesis collapses. The DJ isn’t dragging down your multiple because it’s a bad asset. It’s dragging down your multiple because the market hasn’t recalculated what “better” means in a world where everyone is running out of good rock at roughly the same time.

I’ll be honest: I thought Chevron and Civitas would eventually exit the DJ. Two deals changed my mind.

SM Energy acquired Civitas for $4.6 billion not because SM loved Colorado (SM’s CFO cited “comfort with Colorado” at the Bank of America conference, which is the kind of thing you say when you’re trying to convince yourself as much as the audience). SM bought Civitas because SM’s Midland inventory was severely depleted. Devon acquired Coterra for the same structural reason. Not synergy. Inventory duration. When your Delaware Basin reserve life is 8.1 years against an 11.5-year peer average, you’re not buying efficiency. You’re buying time.

These aren’t synergy deals. They’re admissions that the replacement hypothesis failed. The Street demanded asset rationalization. The geology demanded inventory preservation. The geology won.

And the DJ Basin (the asset everyone was told to sell) produces 40 barrels of water per well compared to 400 in the Permian. Recent vintage wells show slight productivity increases versus the seven-year average, bucking degradation trends across every other major play. 75% of Chevron’s DJ locations break even below $50/barrel. Laterals have lengthened 29% since 2018. The economics aren’t aspirational. They’re proven, improving on the margin, while the Permian’s marginal well gets slightly worse every quarter.

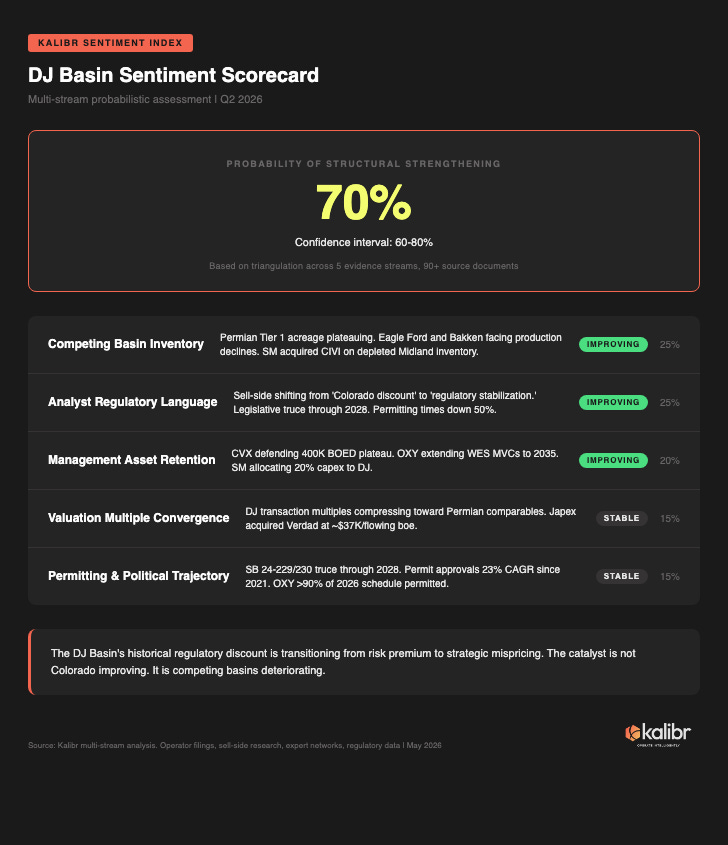

We score this probabilistically. Across five evidence streams, our assessment is that DJ Basin sentiment is structurally strengthening at 70% probability (confidence interval 60-80%). Three of five dimensions trending “improving.” The catalyst is not Colorado getting better. It is competing basins getting worse.

The legislative truce helps. Senate Bills 24-229 and 24-230 paused anti-drilling ballot initiatives through 2028. Permitting times declined 50% in two years. Colorado permit approvals grew at 23% CAGR since 2021. The “Colorado discount” is still priced in. The regulatory risk that justified it is largely gone (for a couple of years, atleast).

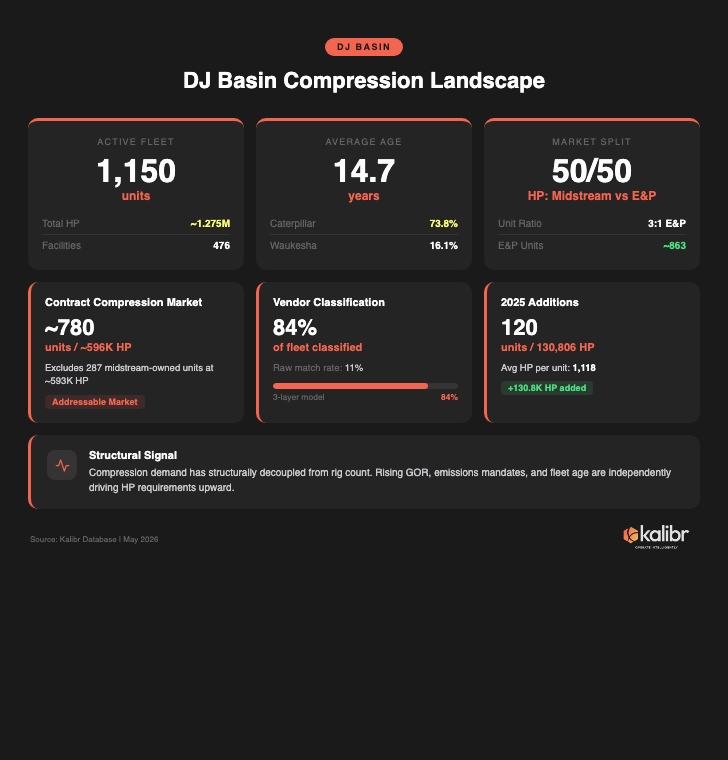

This is Kalibr’s first basin-level compression intelligence report. We mapped every active compressor in the DJ: 1,150 units, 476 facilities, ~1.275 million HP. We classified the fleet by vendor. We built a bottom-up demand model showing 177,000 HP of new demand in 2026. What we found is a market where compression demand has structurally decoupled from rig count, and where the four largest vendors are positioned very differently for what comes next.

The Part Where We Count the Compressors

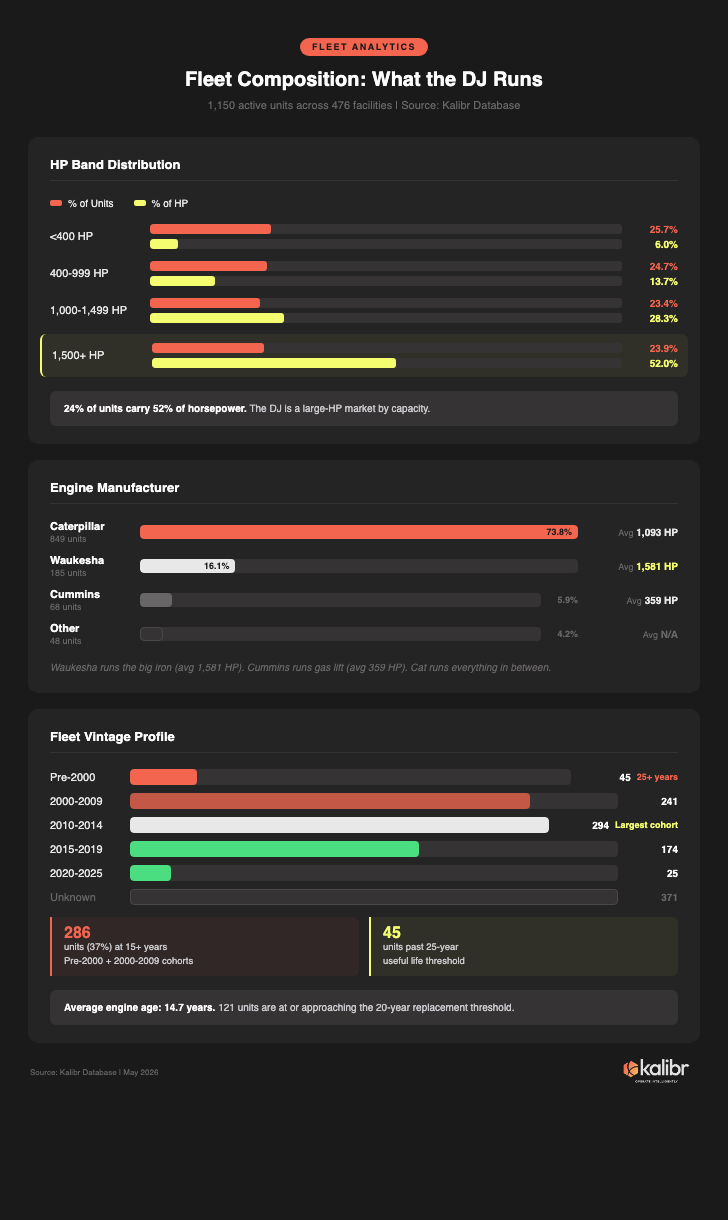

1,150 active units. 476 facilities. ~1.275 million HP. Average engine age: 14.7 years.

Context: KGS’s entire national fleet is 4.5 million HP. AROC runs 3.7 million. USAC, 3.9 million. The DJ represents 5-7% of the US contract compression market, concentrated in a single state with the most stringent emissions regime in the Lower 48. The Permian has more iron. The Haynesville has bigger units. No basin has Colorado’s air quality rules.

The fleet has a split personality. Unit counts are eerily even across HP bands (~25% each), but the 1,500+ HP band carries 52% of all installed horsepower from 24% of units. If you think of the DJ as a “small wellhead compression” market, you’re missing that half the basin’s capacity sits in centralized stations with 5+ compressors per facility (10% of sites, 48% of HP). Caterpillar powers 73.8% of the fleet. Waukesha runs the big iron at 16.1% (averaging 1,581 HP per unit). Cummins handles gas lift at 5.9% (averaging 359 HP).

The fleet is old, and that’s not an accident. When operators view a basin as temporary (the “we’ll exit Colorado eventually” thesis), they redeploy older units and run them until the contracts end. That logic persisted for a decade. Now the contracts aren’t ending. The fleet is still old. 294 units from the 2010-2014 horizontal boom are approaching major overhaul economics. 121 units have already crossed or are approaching the 20-year replacement threshold.

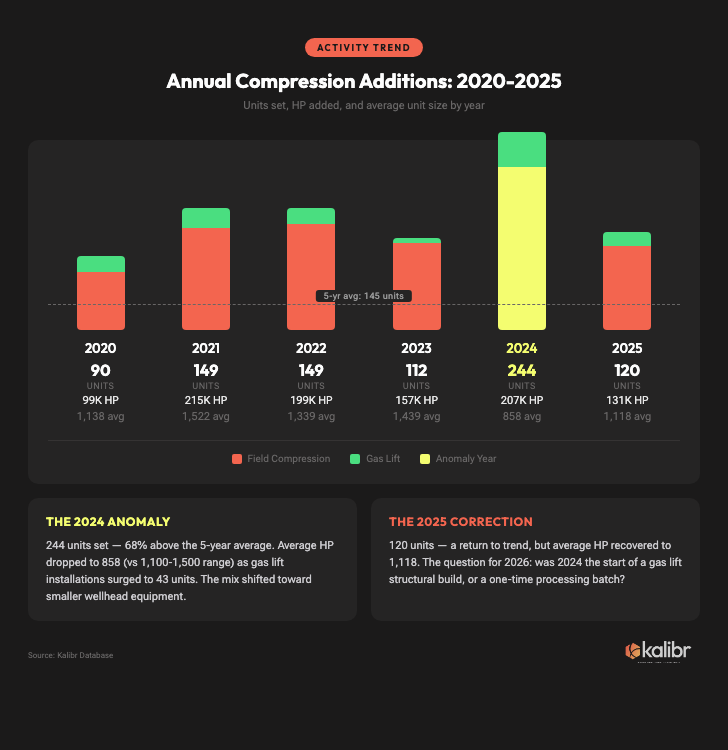

The annual additions data shows a market in transition. 2024 saw 244 units set (68% above average) but average HP collapsed to 858 as gas lift installations surged to 43 units. 2025 corrected to 120 units with average HP recovering to 1,118. The question: was 2024 an anomaly or the front edge of a structural gas lift build cycle as the 2018-2019 vintage wells (1,200-1,400 spuds/year) enter the decline phase where artificial lift becomes economic?

The basin splits 50/50 on HP between midstream-owned and E&P-contracted equipment, but the character is completely different: 313 midstream units averaging 2,105 HP versus 837 E&P units averaging 768 HP. The 287 midstream-owned units (~593,000 HP) sit permanently outside the contract compression market. Which means the market AROC, KGS, and USAC actually compete in is roughly 780 units and 596,000 HP. Smaller than it looks.

Who Wins That Market

The most valuable piece of intelligence in compression is the one nobody has: which vendor operates which unit, at which facility, for which operator. Every basin-level analysis you’ve seen treats the fleet as one undifferentiated pool because that’s as far as the data gets them.

Kalibr’s proprietary classification model resolves this. We’ve built a machine learning system that attributes vendor identity across compression fleets using facility-level spatial patterns, operator relationship signatures, and equipment configuration data. In the DJ, the model classifies 84% of units by vendor. This is the foundation that makes everything else possible: market share, runtime associations, contract term exposure. Without vendor attribution, you have a fleet count. With it, you have a competitive intelligence map.