Nominally Hedged: Buybacks, Bad Counterparties and the Index That Won't Drill

How shareholder alignment, passive concentration, and retail capital flows could reshape oilfield reinvestment—and what smart operators should do next

The Yale Model Goes Suburbia

When asked the (occasionally wine-fueled) dinner-party hypothetical about which historical figure I'd dine with, Lincoln and Da Vinci don’t make my cut. Give me John von Neumann: mad genius, father of game theory, and the spiritual template for Dr. Strangelove.

Or maybe David Swensen.

Yes, that David Swensen—the father of the "Yale Model," who transformed Yale’s endowment from a stodgy collection of stocks and bonds into a high-octane blend of private equity, venture capital, hedge funds, and real assets. By allocating 30–40% to PE, 20–25% to hedge funds, and another chunk to real assets, Swensen didn't just generate alpha; he ignited a financial revolution. If you've ever noticed your dentist aggressively upselling crowns or seen your local HVAC company suddenly monopolize the Google results, congratulations: you've experienced Swensen’s legacy via PE-backed rollups.

Cap Table Reality Check

Here’s PE’s poorly kept secret: It’s not billionaire yacht-owners bankrolling this show—it's institutional capital. Public pensions (~65%), sovereign wealth (~12%), insurers (~8%), endowments (~7%), and family offices (~5%) patiently tie up billions chasing illiquidity premiums and 15–25% IRRs. They fund the engines of capitalism with a calendar marked in decades, not quarters.

PE capital once turbocharged the shale boom, aggregating land and flipping assets to public E&Ps eager for PUD-to-PDP conversions. But now? Energy PE capital plummeted from 24% of sector fundraising in 2019 to a mere ~11% by 2023. ESG headaches, mediocre returns, and volatile hydrocarbon pricing sent pension funds fleeing for cleaner, greener pastures.

Add in new political pressure on endowments —MIT’s bill potentially ballooning from $27M to a staggering $411M—and the Yale Model faces its own denominator problem. LPs must find new ways to manage liquidity, likely steering deeper into PE for deferred realizations while maintaining a cash hoard to service both capital calls and Uncle Sam’s demands.

Retail Enters the Chat

Which brings us neatly to the quiet push to unlock your 401(k) dollars for private equity. This isn’t altruism or some noble experiment in access—it’s the next phase of financial engineering. Public markets long ago recognized retail investors as "steady access to the opposite of Warren Buffett". Professional traders don't prize retail for insights but rather for predictability (see: Citadel and Virtu monetizing your Robinhood trades).

Private equity now seeks the same dynamic. Orlando Bravo of Thoma Bravo candidly explained the strategy: "Retail could end up saving companies that people cannot sell." Evergreen funds, continuation vehicles, and 401(k)-accessible PE packages essentially redistribute institutional leftovers into retail-friendly packaging, with secondary-market evergreen vehicles paying premiums of up to 4% over institutional bids. It’s financial recycling—bad inventory wrapped in longer lockups.

The Exit Problem

In theory, post-consolidation shale assets—divested PDP bundles and undercapitalized non-core assets—should be PE catnip. But math and geology disagree. Buying PDP with PE’s 20–25% IRR over a five-year hold looks dubious at best. Add geological reality—most Tier 1 assets are already stripped—and suddenly good PE projects become scarce.

Smart money is pivoting internationally. Kimmeridge, a pivotal first mover and thought leader in the space (and maybe a firm I wrote my B-school application on?) set up shop in Abu Dhabi. It’s not just strategic diversification—it’s a quiet admission that the Lower 48 simply isn’t enough anymore.

Retail 401(k) flows into PE won’t fix this fundamental scarcity. They'll just make eventual exits even messier.

Passive Concentration

I like paradoxes.

Carl Jung said they're the only things that approach the fullness of truth. Mine aren’t quite so existential; they’re dinner party material. Consider index funds.

On one hand, index funds are profoundly American—low fees, broad exposure, frictionless accessibility. They’re the Costco hotdog of finance: democratic, efficient, and beloved by the 401(k) generation, financial advisors, and your HR portal alike.

On the other hand, what if index funds are quietly un-American?

This isn't a punchline—it’s a serious (and increasingly litigious) question. When three firms collectively own 15%, 20%, or even 30% stakes across every competitor in a concentrated industry, they aren’t betting on specific winners. They're betting on the sector itself. And what’s good for an industry isn’t always good for competition.

Common ownership isn't new. Back in business school, this was a reliably provocative topic after two IPAs: if Vanguard holds large positions in both Delta and United, does it prefer brutal fare wars, or does it quietly root for stable, profitable coexistence? Some research found common ownership increased apparent market concentration tenfold versus traditional HHI analyses. Other studies showed prices inflating by 3–12%. Fascinating theory.

Then theory became practice.

The Case Law Is Coming

So this happened. State attorney generals accused BlackRock, Vanguard, and State Street of quietly coordinating coal producers to restrict output, aligning with shared climate agendas. The DOJ and FTC joined in with a rare, emphatic statement: if common owners influence rival companies to collectively reduce output and inflate prices, it’s effectively collusion.

If you read my previous piece on retail capital flooding into private equity, this should resonate. We're entering an era where portfolio-level incentives outweigh firm-specific strategies. "Owning the market" has become more valuable than betting on outperformance, and the roles of influential allocators—public or private—are now under scrutiny across industries.

Coal might be just the appetizer.

Upstream Implications

Follow the logic.

The Big Three—BlackRock, Vanguard, and State Street—together own 22% of ExxonMobil. Similar patterns appear with Chevron, ConocoPhillips, and throughout midstream and services. A significant chunk of the industry shares identical incentives, risk models, and proxy policies.

Now imagine this: gasoline hits $4.00, inventories plummet, and political pressure intensifies. Your crazy uncle starts ranting on Facebook.

Suddenly policymakers ask: why aren’t we drilling more?

We know the arguments: geological degradation, lack of Tier 1 acreage, uneconomic Tier 2 resources, constrained labor, and supply chain bottlenecks. And, critically, "capital discipline."

But what if “discipline” isn’t purely about balance sheets but rather shareholder alignment?

Because we know shareholder priorities: dividends, buybacks, and historically low reinvestment rates. Exxon announced $20 billion in buybacks through 2025. Chevron followed suit. Post-2020, shareholder religion revolves around capital returns—not growth.

This works well—until someone asks whether this disciplined behavior might resemble coordinated action.

Final Takeaway

Coal made an easy target—few players, legacy industry, clear climate agenda. But oil & gas presents a more intriguing test case.

Unlike coal, oil remains politically potent. Think: "Drill, baby, drill," Strategic Petroleum Reserve releases, and voter sensitivity to pump prices. What happens if future administrations demand production increases that fail—not due to geology, but due to unified shareholder incentives?

That’s where things get slippery.

If prices spike and firms with overlapping shareholders hold back drilling Tier 2 assets, eventually someone will ask: Is this corporate strategy—or is it passive-aggressive coordination?

We’re not quite there yet, but the coal lawsuit tees up precisely this argument.

Common ownership has evolved from academic abstraction to legal liability, pricing risk, and a potential structural obstacle for policymakers treating energy like a policy lever.

In my last piece, I argued retail capital flowing into private equity might unintentionally become the buyer of last resort for industry's hardest-to-sell assets. The paradox? Retail investors, intended as democratizers, become the industry's favorite counterparty.

This indexing paradox is the flipside. The very mechanisms designed to protect investors—diversification, low-fee passive investing—may create incentives that depress competitive behavior and frustrate policy objectives.

Vanguard doesn't pick stocks. But maybe that’s exactly the issue.

Baseball Bats, Game Theory and the Number You’re Not Guessing

Ok, back to talking about things I get paid to consult on.

Last week I spent a good amount of time doing a deep dive into the third-party compression market and what it could mean for our E&Ps. This is what we call first-order leverage. It proves the value of putting yourself in the mentality of the counterparty. In trainings I like to show this strategic and negotiation advantage through a game.

You have 6 guesses to find a number I’m thinking of between 1 and 100. If you guess it, you win $100.

I talked about this briefly earlier this week. Nine times out of ten, the first guess is 50. Then 25. Then 75. All rational—if the number were chosen randomly. It’s basically the Newton method for solving a bounded search problem.

But if you take a minute and think about me—my incentives, my context—you realize something: I don’t want to pay you. I got a 6-year old in competitive baseball and I need the $100 to pay for a 1/5 of his new bat. I know you’ll guess 50-25-75. So I pick something like 61, because that’s my kid’s jersey number and it’s juuuust outside the range you’re conditioned to explore.

Now you’re doing second-order thinking.

Let’s do the same with compression vendors. Not the ones you negotiate with. Their suppliers.

Market Mechanics

Let’s start with the fundamentals. If you’re negotiating with a compression vendor—Archrock, USA Compression, Kodiak—you’re not really negotiating with them. You’re negotiating against their relationship with Caterpillar or Cummins.

These OEMs dominate the high-horsepower compression world. Think CAT’s 3600/3500 engines or Cummins’ growing Power Systems lineup. They are the platforms most compression service providers have built their fleets and their service economics around. And in Q1 2025, both of these OEMs sent loud signals to Wall Street:

Cummins’ is doubling capacity for its 78L and 95L engines.

Caterpillar’s Solar Turbines division is expanding production to serve growing compression and power gen demand.

This isn’t “healthy demand.” This is “overcommitted buildout in anticipation of an energy-tech land rush.” If the data center buildout slows or compression CAPEX slips downstream, they’re sitting on a lot of expensive metal.

So guess what? You now have leverage. Because your vendor’s supplier is quietly getting nervous.

OEM Signals Flash Yellow

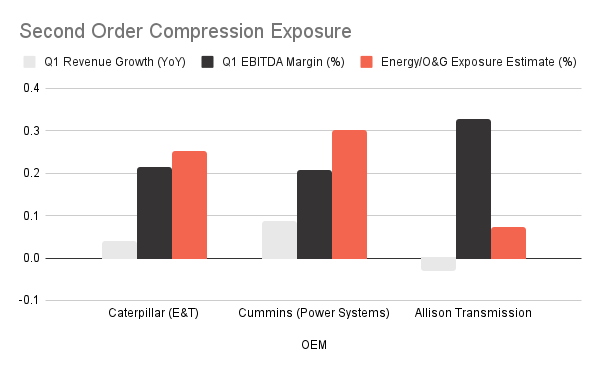

Below is a chart summarizing Q1 2025 financials for the OEMs feeding your compression vendors:

Revenue growth in O&G-relevant segments

EBITDA margins (because net income is for amateurs)

Estimated exposure to energy and compression use cases

Two key points:

Cummins and CAT Power Systems margins are up YoY, even as other segments (like on-highway trucks) soften.

Allison’s margins are elite, but energy is a much smaller piece of the pie (think frac pumps, not central plant compression).

Profit Map

Compression vendors love to sell you a “turnkey solution.” You pay one number, they handle runtime, fuel, maintenance. One throat to choke.

But here’s the trick: the throat they’re offering is already wrapped around a Caterpillar exhaust manifold. Your vendor can’t swap platforms, even if CAT jacks parts pricing or stretches lead times.

Their OEM lock-in becomes your margin unlock—if you push back.

Here’s how:

Refuse to be platform-specified in RFPs. Mandate multi-OEM compatibility.

Break out pricing for runtime, maintenance, and equipment amortization.

Ask how much of their day rate is eaten by OEM inflation.

You don’t have to rip out the whole model. Just poke it where it hurts.

Tactical Playbook

Here’s the kicker: CAT built a mountain of finished goods inventory in Q1, pulling forward production ahead of tariff hikes and demand uncertainty.

Why should your compression vendor be the only one taking those discount calls from CAT Financial?

If you’re an investment-grade E&P, you could:

Buy compression equipment directly

Finance it through CAT Financial or GE Capital (Or someone else)

Contract your preferred vendor for O&M only

Suddenly, you’re no longer buying a black box. You’re leasing a cost-plus asset with a fixed O&M backend. That’s how airlines buy engines. Why shouldn’t we?

Final Compression Ratio

This isn’t about saving 2% on compression day rates. This is about flipping the script. If the OEMs are overcommitted, and your vendors are locked into them, you get to ask new questions:

Why are we paying full freight for amortized assets?

What risk are we underwriting that we’re not charging for?

Can we own the asset and hire the runtime?

This is second-order leverage. Play the game like you picked the number.