Nominally Hedged - 4.19.2026 | The Problem With Winning

In which Kodiak walks through a $675 million door, the leverage ceiling does not move, the dividend does not move, and we find the one thing that does.

A quick programming note. The free edition of Nominally Hedged is moving to Sundays, because that is when I catch up on my own newsletter reading and I assume you do the same. On the paid side, two articles dropping this week: first, a deep dive into the remaining public compression operators (FlowCo, NGS, and Enerflex), and then our first basin-level report (DJ), covering horsepower setting trends, vendor performance benchmarking, and which compression providers are actually winning on the ground. Paid subscribers, your inbox is about to earn its keep.

There is a specific problem that only successful companies have, and it does not look like a problem when it is happening. It looks like success, which is why it is so easy to misread.

Suppose you run a business that does one thing extremely well. Every quarter, the business generates a pile of cash. The first few years, the pile disappears back into growth: more units, more customers, more of the thing you are good at. This is healthy. This is what you want. But the core business has a size, and you do not. Eventually the rate at which you generate cash exceeds the rate at which the core business can absorb it, and you are left with a pile of money and nowhere inside the business to put it.

You have three options. Give it back to shareholders, which is honest but concedes that you have become a terminal-value company. Hoard it on the balance sheet, which your shareholders will punish you for. Or find a new market adjacent to the core, where the company’s existing capabilities give it an edge and the next dollar has a better home than a brokerage account. If the CEO has any ambition at all, door number three is the only door. The incentive structure guarantees it.

In 1997, Boeing walked through door number three. Commercial aerospace had a size, Boeing had outgrown it, and McDonnell Douglas offered a defense adjacency that used the same airframes, the same engineering, and the same customer logic. The pitch book was immaculate. The deal was not stupid. It was the textbook answer to the textbook problem of excess capital in a bounded market.

What Boeing did not price into the deal was what happens when a single-answer capital committee becomes a two-answer capital committee. Before the deal, every quarter the committee had one question: what does commercial aerospace need? After the deal, it had two. And the second question was always reasonable, always had a pipeline behind it, always had executives in the room making a perfectly defensible case for why this quarter’s marginal dollar should fund their program. No single decision was wrong. A rebuild on the Renton line gets deferred six months because defense has a tooling deadline. A component interval gets stretched from eighteen thousand hours to twenty-two thousand because the data says you can probably get away with it. Each trade is defensible in the meeting. It is only in the aggregate, over twenty years, that you see what happened, which is that the discipline of the single-answer committee (the one that had produced the fleet that had produced the franchise) had been quietly liquidated one capital allocation decision at a time. The 737 MAX was not a single failure. It was the terminal installment on a bill that had been accruing since 1997.

I want to be precise about what I am saying here, and what I am not. KGS just walked through door number three. The DPS acquisition is a genuinely smart deal in a genuinely attractive market. I admire almost everything Kodiak has built, and I think their AI-driven maintenance program is the most sophisticated thing happening in compression right now. What I am saying is narrower than “this will go badly.” I am saying: the arithmetic of a two-question capital committee creates a specific corridor of risk, and the most likely place that risk materializes is a line item most people are not watching.

Let me show you the math.

The Winning

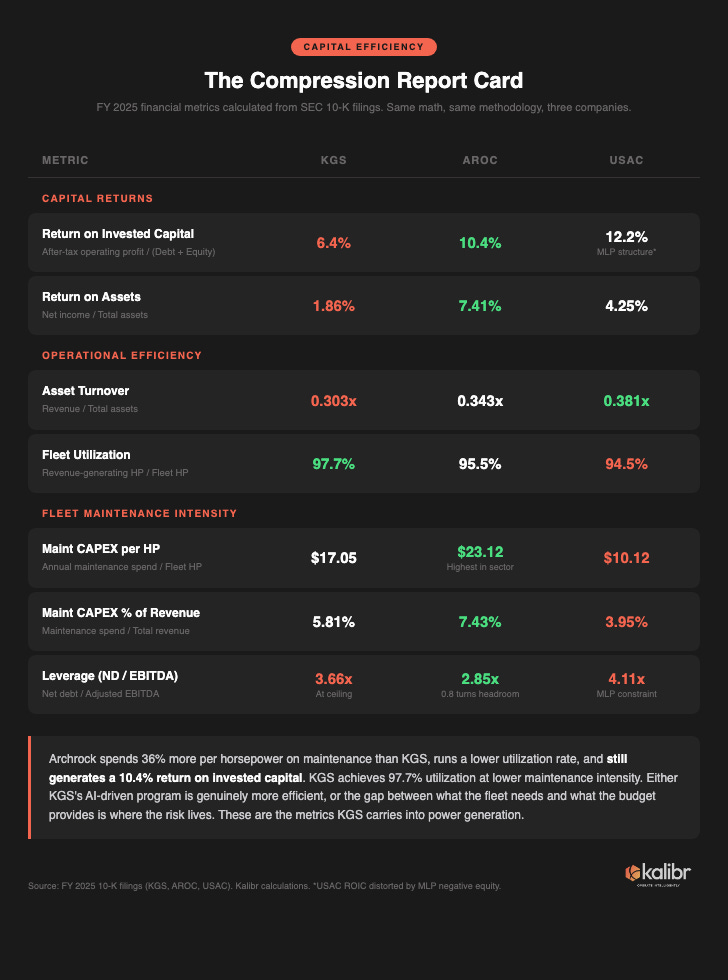

Here is what winning looks like in contract compression: $1.308 billion in revenue, $715 million in adjusted EBITDA, and a 69.2% Contract Services adjusted gross margin that represents a 247 basis point expansion year-over-year. Fleet utilization at 97.7%, with the large horsepower units (which account for 80% of the fleet by horsepower, because KGS figured out years ago that big iron on long-term contracts is where the economics compound) running north of 99%. Revenue per horsepower per month at $23.10, with management guiding toward $24 by year-end 2026. Free cash flow of $230 million, up 87.7% from 2024. Discretionary cash flow of $462 million, up 23.7%.

The EQT AB private equity sponsor fully exited its 76% stake during 2025. That is the kind of detail people skim over, but it matters: the PE overhang that once gave E&P negotiators a talking point about “sponsor pressure” is gone. The leverage ratio hit the long-stated 3.5x target. The company issued compression’s first 10-year bond at 6.75% and left $1.5 billion of ABL capacity undrawn. The balance sheet has never been cleaner.

And the AI-driven maintenance program, the one I am going to spend considerable time discussing in the context of risk, deserves credit. KGS has shifted from time-based 90-day service intervals to condition-based intervals of 120 to 150 days using a Fleet Reliability Center that monitors units in real-time and custom LLMs that provide field support. This is not marketing language. They are running fewer touches per unit per year, maintaining higher utilization, and doing it at a lower maintenance cost per horsepower than any peer in the sector. We will get to what that means in a moment. First, the report card.

I pulled the data and calculated the same metrics the same way. No adjusted-adjusted numbers, no investor deck cherry-picking. The accountants’ math.

The number that jumps out is not the one you expect. KGS’s 6.4% ROIC trails Archrock’s 10.4% by a wide margin, but that is largely a function of leverage (debt is a denominator, and KGS has more of it). The Contract Services margin is best-in-class, and fleet utilization leads the sector. Those are genuinely impressive operating results.

The number that matters for this article is the maintenance CAPEX row. KGS spends $17.05 per horsepower annually. Archrock spends $23.12. That is a 36% gap. On similar-sized fleets serving similar customer bases in similar basins. Archrock’s approach is the traditional one: spend more, overhaul more frequently, maintain buffer. KGS’s approach is the technological one: spend less, use AI to extend intervals, trust the data. One of these approaches is right and the other is wrong, or (more likely) both are defensible within their respective capital structures, and the question is what happens when the capital structure that supports the lower-spend approach gets stretched by a second mandate.

The Door

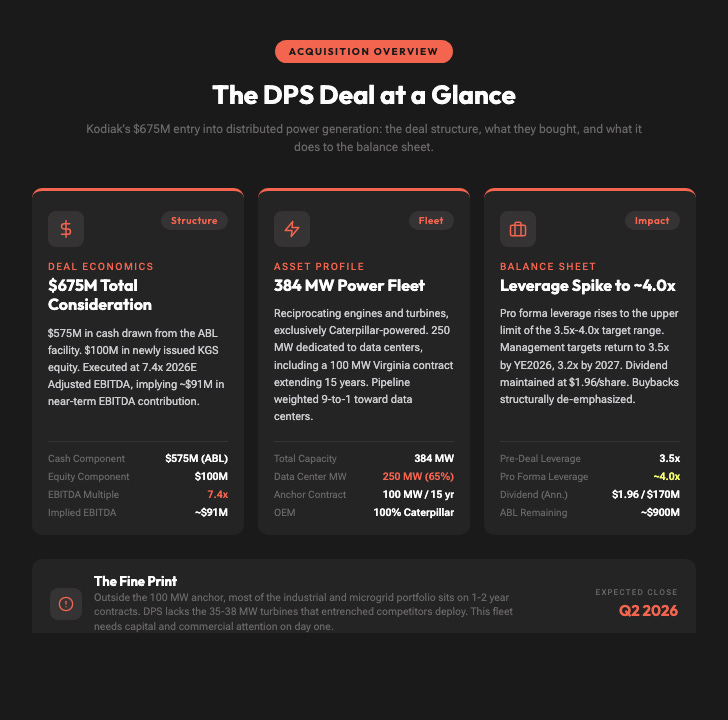

On February 5, 2026, KGS announced the acquisition of Distributed Power Solutions for $675 million: $575 million in cash drawn from the ABL facility and $100 million in newly issued stock. DPS brings a 384-megawatt fleet of reciprocating engines and turbines, exclusively powered by Caterpillar, serving data centers, midstream operators, and industrial microgrid customers.

I want to say this clearly: this deal makes sense. The Caterpillar 3516J engine that powers KGS’s compression fleet shares mechanical DNA with the 3516H generator set engine. The 700-plus Cat-certified technicians already know the platform. The spare parts inventory overlaps. The customer adjacency (Permian operators who need behind-the-meter power because the grid will not show up for seven years) is real. RBC raised its price target from $45 to $64. The market cap expanded by $420 million. Northland Securities noted the market is capitalizing the acquired EBITDA at a premium 12x multiple, which is the market’s way of saying: we like this.

The deal was executed at 7.4x 2026 estimated adjusted EBITDA, implying roughly $91 million in near-term earnings. Of the acquired 384 megawatts, 250 are dedicated to data centers, including a 100 MW Virginia contract extending 15 years. Management’s demand pipeline is weighted 9-to-1 in favor of data centers over traditional oil and gas. In a world where grid interconnection queues stretch five-plus years and hyperscalers will pay almost anything for reliable behind-the-meter power, this is a market where the demand curve is doing the selling for you.

But (and there is always a but, this is a newsletter about compression, not a pitch book) there are specifics worth noting. The DPS fleet is concentrated around 16.5 MW Caterpillar SMT130 units. It lacks the larger 35 and 38 MW turbines that entrenched competitors use for utility-scale data center work. Much of the industrial and microgrid portfolio sits on one-to-two-year contracts requiring immediate repricing and extension upon closing. Piper Sandler flagged this directly: outside of the primary 100 MW data center agreement, the portfolio needs urgent commercial work on day one. And pro forma leverage, per Seaport Research Partners, spiked to roughly 4.0x.

This is a fleet that needs capital on arrival. The question is where the capital comes from, which requires meeting the neighbors.

The Neighbors

Here is something I want people to understand about the distributed power generation market, because the analyst coverage treats it as a homogenous growth opportunity and it is not. The companies already operating at scale in this space are not middling operators collecting a tailwind. They are extremely good at what they do, with structural advantages that took years to build and cannot be replicated by writing a check.

Liberty Energy is the one I keep coming back to. Liberty’s power business (Liberty Power Innovations, through the LAET subsidiary) does something that no other oilfield power entrant does: it manufactures its own equipment. The Forte modular scalable generation systems and Tempo power quality systems are built in-house. When Caterpillar lead times for reciprocating gas gensets stretch past 100 weeks and OEMs are enforcing strict customer selection on allocation slots, Liberty is not standing in the queue. It is running its own factory.

That manufacturing integration matters more than most people appreciate. Liberty has 1.3 gigawatts of power agreements in place, a 400 MW reservation with Vantage Data Centers on 10-to-15-year energy service agreements, and a 3 GW capacity target by 2029 supported by an $813 million 2026 CAPEX budget. Piper Sandler notes that up to 70% of that budget can be funded through project-specific financing, which is a polite way of saying Liberty can build power gen capacity without putting the core frac balance sheet at risk. And the balance sheet: Total Debt to Total Stockholders Equity between 0.14x and 0.30x. I want to make sure that registers. Kodiak is running at 3.5x net debt to EBITDA. Liberty’s leverage ratio has a decimal point in front of it.

Liberty’s 14-year average Cash Return on Capital Invested runs 23%. In 2025 it compressed to 13% as completions activity softened (commodities do that), but 13% on a 0.30x levered balance sheet is a company with the margin of safety to absorb a bad quarter, a pricing war, or a new competitor who wants to buy their way into the neighborhood. The ROIC-to-WACC spread (the gap between what the business earns and what the capital costs) is wide enough to fund mistakes. KGS, at 6.4% ROIC on a 3.5x levered capital base, does not have that same width.

The rest of the power gen field is not empty either. Solaris is targeting 2.2 GW by early 2028 with $300,000 in annualized EBITDA per megawatt. ProPetro’s PROPWR division has a 60 MW hyperscaler contract and hybrid gas-battery systems. Atlas signed a 1.6 GW Global Framework Agreement with Caterpillar at high-teens IRR targets. These are not pilot programs. They are funded businesses with contracted cash flows.

None of these companies are better than KGS at running compression. I am not saying that. What I am saying is that KGS’s compression excellence was built over a decade of single-answer capital allocation, where every dollar was a compression dollar. These power gen competitors have been building their own version of that single-answer discipline in their own market. KGS enters as the new entrant against incumbents who have the fleet scale, the contract relationships, and (in Liberty’s case) the manufacturing capability that KGS will need to spend capital to match.

The risk is not that KGS will be bad at power generation. It is that being competitive might cost more than the capital structure can comfortably absorb. And when you are trying to close a gap against operators who have a 500 basis point CROCI advantage and a leverage ratio with a decimal point in front of it, each incremental dollar of investment feels more urgent than the last.

The Rigid Triangle

I have been circling the arithmetic. Let me land the plane.

KGS operates under three financial commitments that management has publicly treated as non-negotiable. I believe them on all three, which is precisely the problem.

The leverage ceiling. 3.5x consolidated net leverage or below. The DPS acquisition pushes pro forma leverage to approximately 4.0x, with Goldman projecting a return to 3.5x by year-end 2026. This is not guidance you can quietly revise. The 3.5x target underpins the midstream-like valuation multiple the market assigns KGS, the pricing on $2.6 billion in outstanding debt (including compression’s first 10-year bond), and $1.5 billion of undrawn ABL capacity. Breach it and you are not just missing a target. You are repricing the equity.

The dividend. $0.49 per share quarterly, $1.96 annualized, recently increased 20%. Approximately $170 million per year. Dividend coverage at 2.6x (versus Archrock’s 4.9x, which is the financial equivalent of never having to worry about your rent). Cutting the dividend in this sector is like a restaurant failing a health inspection: technically survivable, but the customers remember.

The growth mandate. 150,000 new large horsepower per year in compression, 750,000 total through 2030. Growth CAPEX guided at $235 to $265 million for 2026 compression alone, before DPS power gen spending. The 2026 new-build order book is 100% pre-contracted. Engine deliveries are being secured for 2027 and 2028 at 100-plus-week lead times. You do not call Caterpillar and cancel because your Q2 EBITDA came in light. This capital is committed.

Three immovable objects. One budget. If growth costs more than planned (because power gen scaling requires incremental capital, or because Cat raises prices again, or because the macro softens and EBITDA undershoots guidance), the money has to come from somewhere.

You cannot borrow it (leverage ceiling). You cannot redirect shareholder returns (dividend). You cannot slow the new-build pipeline (committed).

Maintenance CAPEX, guided at $75 to $85 million for 2026, is the line item with give. It is, if you want to be clinical about it, the only remaining degree of freedom in the capital allocation framework.

Maybe it does not need to give. Maybe KGS’s technology-optimized maintenance approach is genuinely sustainable at $17.05 per horsepower while Archrock’s $23.12 represents structural over-spending. The AI is real. The efficiency gains are documented. KGS management has earned the right to that benefit of the doubt.

But the margin between “everything works” and “something has to give” is narrower than I would like. So I built a model.

The Model

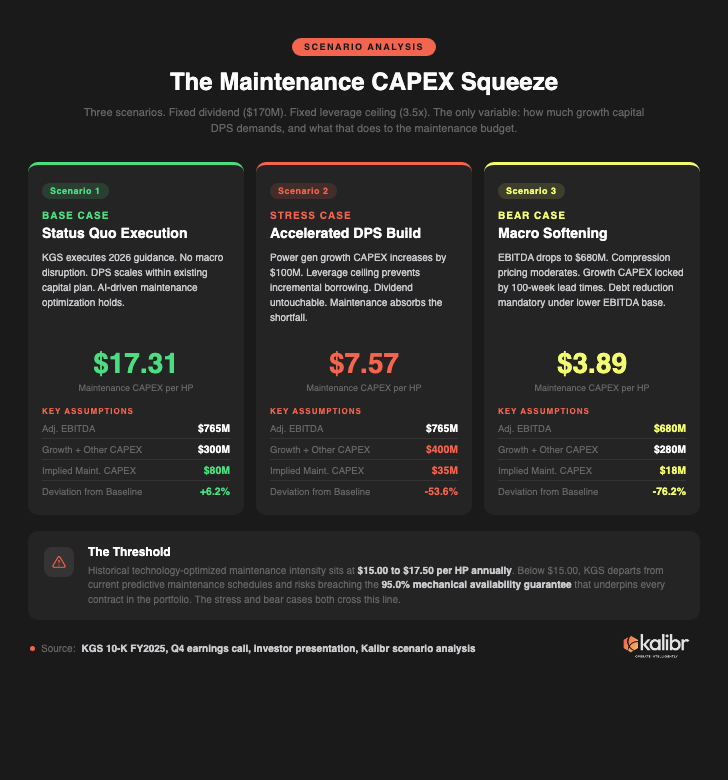

Three scenarios. All three hold the dividend at $170 million and the leverage ceiling at 3.5x. Fleet: 4.62 million horsepower.

Base Case. Guidance met. EBITDA: $765 million. Growth and other CAPEX: $300 million. Implied maintenance CAPEX: $80 million ($17.31 per horsepower). This is within baseline. Overhauls on schedule. AI extends intervals without degradation. Everything works. I think this is the most likely outcome.

Stress Case. KGS leans into the data center opportunity (management described the behind-the-meter market as “vast” and expressed intent to deploy “as much capital as is reasonable”). Growth CAPEX increases $100 million for power gen. Leverage ceiling prevents ABL borrowing. Dividend is sacred.

Maintenance CAPEX absorbs the shortfall: $35 million, $7.57 per horsepower. A 53.6% deviation from baseline. At this intensity, major engine overhauls get deferred. Spare parts pools deplete. The Fleet Reliability Center keeps monitoring, but the budget to act on its findings is not there. The technology still works. The budget does not.

Bear Case. Macro softens. Archrock’s CEO has already noted that repricing increases going forward will be “more modest,” which is the compression sector’s version of saying the pricing cycle has peaked. EBITDA drops to $680 million. Growth CAPEX, locked by 100-week-lead-time commitments, cannot flex. Maintenance CAPEX is forced to $18 million, $3.89 per horsepower.

At $3.89 per horsepower, you are not optimizing maintenance schedules with artificial intelligence. You are hoping nothing breaks.

Now here is the layer that connects the competitive landscape to the budget. If KGS’s power gen ROIC comes in at 10% (versus Liberty’s 13% incumbent benchmark, which is itself a down year), the EBITDA gap on the initial $675 million investment is approximately $23.5 million. Closing that gap at degraded unit economics requires $235.8 million in incremental capital.

That is 51% of KGS’s annual discretionary cash flow. On a balance sheet that is already at 3.5x leverage. With a dividend that cannot be cut.

I do not think this is the most likely outcome. But I note that the distance between “base case” and “we need more capital” is uncomfortably short, and the consequences of landing in that corridor are disproportionate to the probability.

The Part Where the Contract Becomes the Story

I spend a lot of time reading compression contracts (someone has to, and based on the redlines I see, it is not always the people signing them). The availability guarantee is the clause that matters here, and it is worth understanding precisely because the mechanism is a sequence, not an event.

Every KGS contract contains a mechanical availability guarantee: 95.0% to 98.0%, calculated against all downtime including mechanical shutdowns, routine repairs, and scheduled overhauls. Three consecutive months below threshold and the customer can terminate. That is not ambiguous language buried in a rider. It is the core commercial term.

Deferred maintenance does not produce a dramatic failure. It produces a slow erosion that nobody notices until everyone notices.

First, spare parts pools thin out. The localized inventory that enables a three-to-five-hour field cylinder head swap starts getting allocated instead of stocked. Second, the Fleet Reliability Center keeps flagging potential issues (the AI works regardless of the budget), but when the money for parts and labor is not there to act on the flags, response shifts from proactive to reactive. Third, minor issues that were same-day fixes stretch into multi-day outages because the part is not on location and OEM components have their own lead-time queue. Fourth, unplanned downtime hours compound. The 98% number softens.

Industrial software specialists note that even the best predictive dashboards miss roughly 5% of sporadic failures. When budgets are healthy, that 5% gets absorbed by spare inventory and rapid field response. When budgets tighten, the 5% becomes the leading edge of a reliability decline. And KGS has already pushed intervals from 90 to 120-150 days. The buffer is thinner than it used to be.

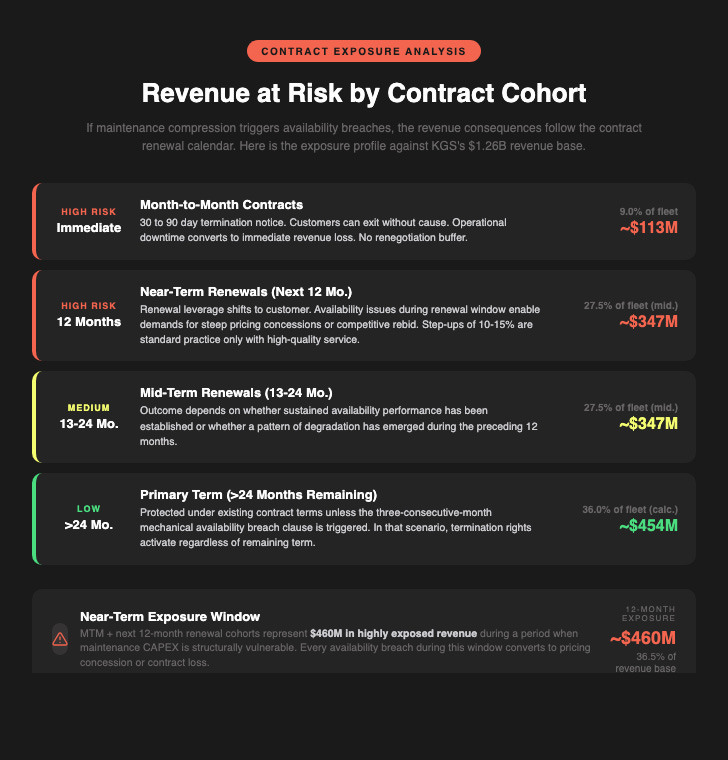

The revenue exposure: approximately 9.0% of KGS’s fleet sits on month-to-month contracts (30-to-90-day termination). Management indicates 25% to 30% comes up for renewal annually. Against the $1.26 billion 2026 Contract Services revenue midpoint, roughly $460 million is exposed over the next 12 months.

$460 million in revenue governed by availability guarantees that are directly connected to a maintenance budget that is the designated relief valve for a two-front capital strategy. Maybe the technology holds. But if I had $50 million in annual KGS spend and a contract rolling in 18 months, I would want to understand this math.

How the Peers Solve This

The question is not whether dual-growth strategies work. Baker Hughes pivoted into power and data center infrastructure and the market rewarded it with a premium multiple. SLB is building a billion-dollar data center solutions business. Companies that can fund adjacencies without straining the core tend to be rewarded handsomely.

The question is whether KGS’s specific capital structure has the flexibility to fund both mandates without one cannibalizing the other.

Archrock stayed home. No power generation entry (explicitly declined; assets did not meet return and quality criteria). The result: 2.69x leverage with 0.8 turns of headroom below target, $110.7 million in maintenance CAPEX ($23.12 per horsepower, highest in sector), 4.9x dividend coverage, 6.0% senior notes (lowest coupon in compression history), no maturities until 2032. Archrock’s capital allocation answer is: grow the core, protect the maintenance budget, let the balance sheet absorb shocks. It caps the upside. It also structurally bounds the downside.

Liberty walked through door number three with a fundamentally different balance sheet. 0.14x to 0.30x debt-to-equity. When Liberty needs power gen capital, it decelerates frac growth CAPEX, slows buybacks, and uses project-specific financing. RBC notes explicitly: Liberty has outlined a clear funding path that preserves the estimated $200 million annual frac maintenance budget. Liberty never touches maintenance. Its release valves are everything else.

The difference is not about management quality. Mickey McKee at KGS is as good as anyone running a compression business. The difference is structural. Archrock and Liberty have release valves that are not their core fleet. KGS, at its maximum stated leverage with a recently increased dividend, has fewer options. The capital structure funnels any variance from the base case toward the one budget with flex.

And that budget is the one that produces the uptime that produces the revenue that produces the cash flow that funds the dividend that cannot be cut.

What to Watch

Five metrics. All leading indicators of whether this thesis is playing out.

Maintenance CAPEX per horsepower. Baseline: $15.00 to $17.50. Below $15.00 signals departure from predictive schedules. Context: Archrock runs $23.12 per horsepower and generates a 10.4% ROIC. KGS runs $17.05 and generates 6.4%. The AI narrative has to keep working.

Capital classification shifts. KGS split growth CAPEX into “growth” and “other” in Q1 2025. If maintenance activities migrate into “other” while the headline maintenance line stays flat, the accounting is doing the work that the spending is not.

Operating expense per horsepower. Management credits AI for lowering engine repair costs and lube oil consumption. If per-horsepower OPEX rises sequentially, deferred maintenance is surfacing as reactive field cost. Technology delays maintenance. It does not eliminate it.

Large HP utilization language. KGS cites 99%+ for large units. If the descriptor shifts from “operating” to “contracted” or “revenue-generating” utilization, mechanical downtime is entering the fleet. Words are leading indicators.

The AI efficiency narrative. If management’s emphasis on AI-driven maintenance intensifies precisely as per-horsepower budgets flatten or decline, ask yourself: is the technology supporting the budget, or is the narrative substituting for it?

What This Means for Operating Teams

I want to end where I started. KGS has built something exceptional. The utilization numbers are real. The Cat relationship is the deepest in compression. The AI maintenance program is genuine competitive advantage, and it may be the thing that makes this entire article a theoretical exercise. I would not bet against this management team.

But I would not bet my contract terms on a capital structure, either. The rigid triangle (leverage, dividend, growth) creates a corridor where the maintenance budget absorbs variance. That corridor may never be entered. If it is, the consequences compound through a specific mechanism: deferred overhauls, thinning spare parts, lengthening response times, softening availability, and eventually, customer leverage during $460 million in near-term renewals.

Operating teams with KGS contracts in the renewal window should be doing three things. First, structuring escalating performance credits tied to trailing three-month mechanical availability (not just the headline guarantee, the running average that triggers termination rights). Second, building month-to-month conversion clauses that activate if trailing availability drops, preserving optionality without forcing premature vendor changes. Third, documenting insourcing economics (replacement at current lead times: approximately $1,250 per horsepower, 7-year payback on new, shorter on opportunistic used 3516s) and surfacing the analysis in renewal discussions. Not as theater. As a BATNA.

This is the analysis that moves from interesting to actionable when you map it against your specific contracts, basins, and renewal timelines. The Leverage Matrix was built for exactly that purpose.

The 737 MAX was not a design flaw. It was what happens when a two-question capital committee defers one small decision per quarter for twenty years.

KGS is not Boeing. The deal is smart, the team is excellent, and the AI-driven maintenance program may genuinely solve the problem I have spent 4,000 words describing. I hope it does. Permian compression is better because KGS is in it.

But the arithmetic of a two-question capital committee is the same arithmetic regardless of who is running it. And when the margin between “everything works” and “something gives” narrows to the width of a single line item on a quarterly filing, someone should be watching that line item.

Watch the line item. Not the headline.

Nominally Hedged goes out to a small list. If you know someone running compression negotiations this cycle — or who should be — forward it. That's the whole ask.