Nominally Hedged | 2.6.2025: Curb Your G&A

Larry David, the HOV lane, and the billion-dollar industry habit of adding overhead to reduce overhead.

There is an episode of Curb Your Enthusiasm that I think about every time I sit through an enterprise AI pitch.

Season 4, Episode 6. Larry David needs to get to a Dodgers game. Traffic is terrible. The HOV lane is wide open, but you need two people in the car to use it. The rational solutions are obvious: leave earlier, take a different route, accept the drive. Larry does none of these things. He picks up a stranger to sit in his passenger seat so he technically qualifies for the carpool lane.

This is a very Larry David solution to a problem. He has not reduced his travel time through any structural change. He has not altered his route, his departure time, or his driving habits. He has paid someone to sit next to him so that he can access a lane reserved for people who have actually solved the transportation problem. The appearance of efficiency, purchased at a premium, layered on top of a system that remains completely unchanged.

And, predictably, the shortcut creates more problems than it solves. The passenger becomes a subplot. The subplot becomes a catastrophe. Larry arrives at the game having spent more time, more money, and more emotional energy than if he had just sat in traffic like a normal person.

This is enterprise AI spending in oil and gas.

Most companies right now are Larry David in the carpool lane. They have an efficiency problem. Too many people doing manual, repetitive work across procurement, finance, operations, engineering, regulatory. The real solution is to build internal AI capability that automates those workflows and right-sizes the team. But that is uncomfortable. It means making hard org design decisions, restructuring staff, and doing the unglamorous work of rearchitecting how the business actually runs.

So instead, they pay a vendor to sit in the passenger seat. They license an AI platform, bolt it on top of existing workflows, keep the same headcount, and call it digital transformation. The vendor shows up in the investor deck. The conference panel gets a talking point. The HOV lane sticker goes on the bumper.

Meanwhile, the car has the same number of people in it, costs more to operate, and is not moving any faster.

The reason this matters is specific to where oil and gas sits right now, and to understand that, you have to understand the decade that just happened.

From Body Shop to Factory Floor

I talk a lot about the commoditization of the technical fields in Oil and Gas, which, like the commoditization of anything, is generally bad for the thing being commoditized (in this case, my fellow engineer).

This long journey started with the rise of unconventional development around the 2010s but amplified in the period of 2015 to 2019 and was precipitated by the commodity price collapse of 2014-2016. Kimmeridge wrote a lot of great stuff on this (hell, I wrote my MBA application on their model). E&P operators pivoted from “growth at all costs” to strict capital discipline and efficiency. This fundamentally altered G&A cost structures and workforce compositions, moving the industry toward a manufacturing model of standardized processes and reduced reliance on bespoke technical oversight.

The simplest way to understand what happened is this: oil and gas used to be a custom body shop. Every well was a bespoke project. Different geology, different casing programs, different completion designs, different problems that required different expertise to solve. You needed people who could think on their feet because the work genuinely required it. Casing seat hunts, gravel pack designs, true exploratory drilling where you were not sure what you were going to find at total depth.

Then unconventional development turned it into a factory. The wells started looking the same. The completion designs converged. The drilling programs became statistical exercises in repeatability. And when the work looks the same, the inputs become narrower, simpler, and easier to switch out. You do not need an artisan when you are running a production line. You need an operator. And operators, by definition, are more interchangeable than artisans.

The G&A reduction that followed plays out in four stages, and each one made the next one inevitable.

Stage 1: Standardization (2015-2019). The entire industry converged on the same factory model. Cube development. Standardized well designs. Pad drilling. The language varied by operator but the economics were identical: make the wells the same, make the people interchangeable, make the G&A per barrel go down every quarter. Pioneer’s G&A journey from 2015 to 2017 tells the story in three numbers: $4.39 per BOE, $3.80, $3.28. Management’s stated strategy? “Not replacing personnel who have left the Company.” Production volumes climbed 15-16%. Headcount didn’t. The math was elegant and merciless. Continental hit $1.57 per BOE by 2019. Extraction collapsed from $4.85 to $3.05 in a single year.

From a negotiation and BATNA perspective, this was bad for technical engineers and generally good for companies. If I need an engineer to drill an extended reach well off the coast of Sakhalin Island, there may be a handful of people I can call (and I got a buddy if you need it). But if you need someone to run a rig in North Dakota, there are generally more people to switch out for that.

Stage 2: Capital Discipline (2020-2023). This really took off post-COVID, as companies fought relentlessly against the flight of stockholders to more ESG-friendly stocks and the general appeal of technology companies. Remember, when you buy a stock, you are buying the discounted cash flows into the future, and if folks are uncertain of that industry’s future, you don’t want to own the stock. The industry combated this through dividends and buybacks: “Don’t worry about the cash 20 years from now, we are going to give it to you now.” Cash for dividends had to come from somewhere. Executive compensation structures got scrutinized. “Right-size G&A” became a boardroom mantra. More jobs out.

Stage 3: Consolidation (2023-present). This chapter starts when my old mothership, Exxon, bought Pioneer. That was the shot that started the race. And what followed was the most concentrated wave of upstream M&A in modern history. Chevron-Hess. Diamondback-Endeavor. ConocoPhillips-Marathon. Oxy-CrownRock. The synergy math on every single one of these deals started with G&A, because G&A is always the first and easiest thing to cut. It is certain and the ramifications are felt later. Clear books on salary. Cut this, save this. The number shows up in your next quarter. The industry has eliminated $2.0 to $2.5 billion in pure annual corporate overhead through this cycle, within a broader total synergy pool exceeding $8 to $10 billion annually. Exxon doubled its Pioneer synergy target from $2 billion to $4 billion. ConocoPhillips doubled Marathon from $500 million to over $1 billion. Chevron hit its Hess target six months early and raised it. Every single acquirer guided conservatively and then beat and raised. This is not coincidence. This is a playbook.

Stage 4: The Build. All of this adds to a more than 100% increase in wells per engineer between 2015 and 2025. The low-hanging fruit for G&A reduction has been harvested. Standardization, consolidation, headcount attrition. The next horizon in G&A reduction is a bit more complicated. It is building new capability on top of what is now one of the leanest operating foundations of any capital-intensive industry in the country.

And this is where AI actually matters. But for it to matter, it has to respect the direction of the trend. It has to continue driving G&A down. Not sideways. Not up. Down.

That turns out to be a very specific constraint, and it is the one that almost every AI vendor currently fails.

The Passenger Seat Has a License Fee

Let me come back to Larry.

The reason the carpool lane scheme fails is that Larry has added a cost to the system without removing one. He still has the car. He still has the commute. He still has himself. Now he also has a passenger he is paying for, a passenger who creates complications, and a net increase in the total cost of getting to Dodger Stadium. He is in the fast lane. He is spending more to be there.

AI software sold to an E&P company works the same way. It sits on the G&A line. The license fee is G&A. The implementation cost is G&A. The internal resources dedicated to managing the vendor relationship are G&A. And the person whose work the software was supposed to automate? Still there.

Here is why that person is still there. The work that AI currently automates well in oil and gas tends to be partial. It handles a slice of a role, not the whole thing.

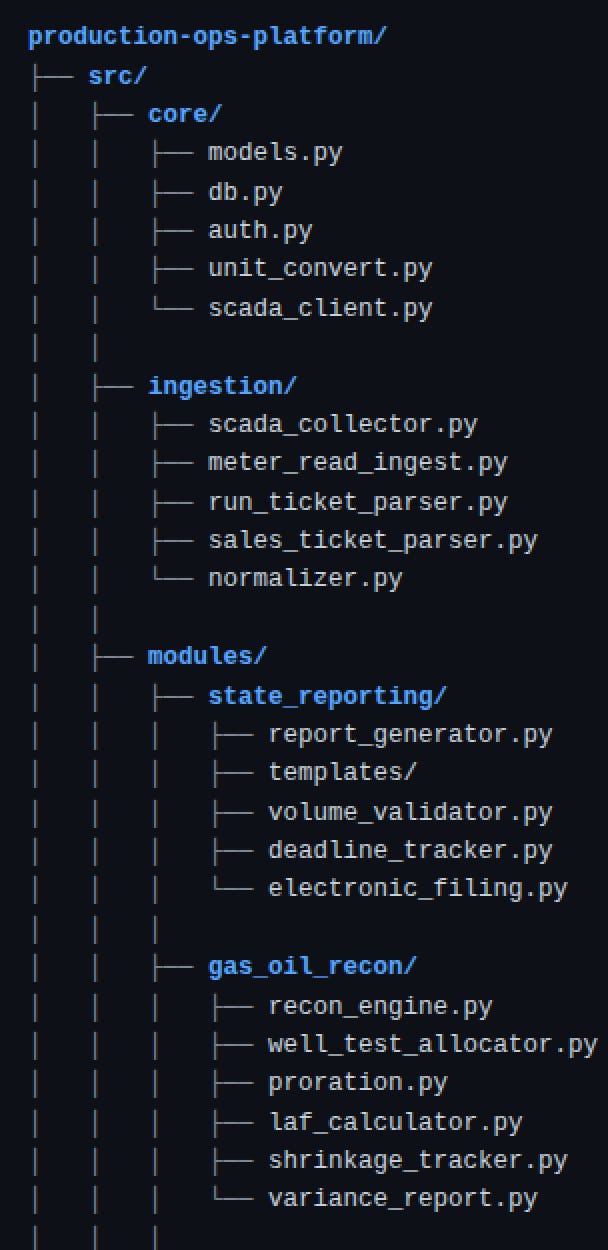

Take gas and production reconciliation (we built something around this last year). An agent can pull statements from the buyer, cross-reference production against the E&P’s internal data, map contractual agreements with midstream counterparties, and generate a reconciliation report with automated state submission. That is real, functional automation. It works.

In most cases, that task is handled by a production tech or production accountant making roughly $150K all-in. But reconciliation is maybe 25% of their job. So you are automating $37,500 of addressable labor. The other 75% of that person’s role is untouched.

You are not going to reduce staff and show an ROI on the investment over $37,500 of automated work. The person does other things. You are going to want a human reviewing the output before it goes to the state, because the downside of a bad filing is regulatory, not cosmetic. So the person stays. The software gets added. G&A goes up.

This is the structural problem with selling AI. The roles that are easiest to partially automate are the roles where the person does multiple things, the salary is moderate, the addressable slice is small, and the output still requires oversight before it is done. At every step, the math pushes you toward G&A addition, not G&A reduction. The vendor’s business model requires a license fee that exceeds the value of the automated slice. The operator’s risk tolerance requires a human check on the output. The result is a passenger in the seat, a sticker on the bumper, and a larger G&A number than you started with.

The companies writing seven-figure checks to AI vendors without reducing staff are not transforming anything. They are paying someone to sit next to their existing problem so they can say they are in the fast lane. And yes, there are AI applications improving cycle time, production optimization, and reservoir characterization that live outside the G&A line entirely. I will touch on those next week. But for the current wave of enterprise AI sold against the overhead budget, the arithmetic is what it is.

And just like Larry, they are going to end up spending more, causing more chaos, and arriving no faster than if they had done the hard thing from the start.

Fewer People in the Car, No Vendor in the Passenger Seat

The company that actually captures AI value is the one that skips the carpool lane gimmick entirely. No vendor riding shotgun. No inflated software line item. Just fewer people in the car and lower cost per mile.

The way you get there is by shrinking the distance between the subject matter expert and the coder to a single node. Not replacing the SME. Not bolting a chatbot onto their workflow. Collapsing the two roles into one person who builds and runs the automation themselves, with no vendor in the middle. This is relatively straightforward for most O&G technical personnel who graduated in the 2010s with some background in Python and data.

The vendors are selling separation: “Your engineer does engineering, our product does the automation, you pay us a license fee.” That is three nodes. That is more G&A, not less. I am arguing for convergence: “Your engineer does engineering and the automation, you pay nobody a license fee, and you reduce headcount with a clear ROI.” That is one node. G&A goes down. The trend continues.

The separation model is a product. The convergence model is a capability. Products are G&A. Capabilities are not.

Let’s set a target. Average wells per engineer is somewhere around 16 to 18 today. Diversified Energy is the industry proof of concept for what technology-driven asset management looks like when you build it internally. DEC runs approximately 75,000 wells with 1,589 total employees, yielding a wells-per-engineer ratio somewhere between 530:1 and 750:1. DEC is a fundamentally different animal. No-drill model, 10% decline rates, mature conventional assets, 99.9% held-by-production acreage. They built a proprietary platform called SAM that decouples well count from headcount, pushes decision-making to field operators via handheld diagnostics, and monitors 75,000 wells through Integrated Operations Centers using management-by-exception. Their lease operators manage roughly 150 wells each versus the industry standard of 50.

DEC is not the comp for an active driller. But it is the proof of concept that the gap between 16 wells per engineer and 500+ wells per engineer is not a technology problem. It is an architecture problem. DEC did not buy SAM from a startup. They built it because they understood their own operations better than any third party could.

My hypothesis is that with the right AI stack and a subject matter expert who knows what to build, you can replicate something approaching DEC’s ratio in an active development context. Not by buying software. By building agentic workflows that couple technician, regulatory, and entry-level engineering tasks with AI agents: automated state reporting (Quad O-A, SPCC, stormwater), production surveillance and exception-based alerting, lease revenue reconciliation, decline curve screening, and regulatory compliance tracking. The goal is: how many assets can a single engineer and limited staff manage effectively, with no vendor overhead and continued downward pressure on G&A per BOE? This, of course, is an optimization problem. Building these things in AI is not void of cost, so one must factor that in. But an example of a base REPO that we have worked on looks something like this:

Small Companies, Big Leverage

Engineers at small companies and startups will have a leg up for three reasons.

First, breadth of exposure. If you have been part of a startup, you are keenly aware of the early days filling state reports yourself, handling production accounting, managing regulatory submissions. You know the full surface area of operations because you had to do all of it. At big companies, that work gets siloed. The engineer who has never filled Air Emissions report does not know it can be automated.

Second, it is much easier to start lean and never hire than to restructure an existing workforce. ConocoPhillips is cutting up to 3,250 people to capture its Marathon synergies. Chevron is reducing headcount by 15-20% globally. That is brutal, expensive, and operationally disruptive. Starting with a small team and agents on day one is not.

Third, large companies are largely constrained to CoPilot AI through Microsoft enterprise agreements, and these are meaningfully behind the alternatives in the market.

Table Stakes and the Three Buckets

Everything I have outlined above gets you a first mover advantage. It is real and it matters. But it is also replicable. Like most D&C techniques, once someone proves it works, others copy it. The 530-to-750 wells-per-engineer ratio becomes table stakes the way the extended lateral became table stakes.

The true competitive moat comes from something different: having a differentiated subject matter expert view that no one else has, and building a tool that repeats that view at scale. Not generic automation of generic tasks. Proprietary insight embedded in proprietary workflow. The person who understands both the domain and the tooling does not need a vendor. They are the vendor.

I think that moat has to fall into three specific buckets. Next week I will go into detail on what those are, the incentive case for building them (both for fundraising and running an asset), and an actual product we have built and deployed.

The next version of the oil and gas company might be a $500MM PDP machine run by a small group of people. They will not be interchangeable. They will be interdisciplinary. Fluent in reservoir economics, capital planning, procurement, and AI workflows. When talent is commodity, the edge becomes synthesis.

This industry did not spend a decade getting lean because it lacked ambition. It spent a decade getting lean because it is pathologically good at adapting to constraints. The companies that survived are the most operationally disciplined firms in any capital-intensive sector in this country. That is not a customer base that needs a vendor in the passenger seat. That is a customer base that needs fewer people in the car, moving faster, at lower cost.

Larry paid for a shortcut and ended up with a longer, more expensive trip and a story he would rather not tell. The companies that skip the gimmick, build the capability internally, and actually reduce the headcount and the overhead?

They’ll be….Pretty, pretty, pretty good.