Nominally Hedged | 1.6.2026: The Conveyor Belt Problem in Oil and Gas

Why outsourced compression earns 70 percent margins, looks suspiciously like infrastructure, and is quietly forcing E&Ps to rethink who should really own the factory

Imagine you’re building a manufacturing plant and, after months of capex discipline and process optimization, you decide not to own the conveyor belt. You outsource it. The third party controls uptime, throughput, and response time, earns a 70 percent margin, and cannot be easily replaced without redesigning the plant. This is not a best practice. It is a thought experiment designed to make a board uncomfortable.

Now imagine the plant is an oil well.

Every well is a purpose-built factory. You choose the architecture up front, and that choice locks in how the system behaves for years. In unconventional oil, the critical fork in the road is artificial lift. ESPs can deliver high rates, but they pull you toward larger casing strings and more steel in the ground. The industry, in pursuit of capex efficiency and free cash flow, has been moving the opposite direction. Slimmer designs push operators toward gas lift, and gas lift pushes you, inevitably, toward compression. These are not modular decisions. They are factory design choices.

Which is why outsourced compression is such a strange equilibrium. Compression is not an accessory. It governs backpressure, stabilizes lift performance, and determines whether production hums or stumbles. Switching it is not like swapping a pump. It is like changing the conveyor belt after the plant is already running. Historically, outsourcing made sense because early unconventionals were uncertain. You did not know what the factory would produce, so you rented flexibility.

That uncertainty is mostly gone. What replaced it is something more interesting. Since 2020, compression providers have culled fleets, consolidated, and rediscovered a lesson E&Ps learned earlier: scarcity plus discipline equals distributions. The result is a business earning roughly 70 percent margins on equipment that is operationally critical and structurally sticky.

That dynamic has accelerated consolidation, particularly around large, electric, high-horsepower fleets. Archrock and Kodiak have been explicit about this playbook. Fewer units. Higher utilization. Cash returned to shareholders. Compression, it turns out, wants to be an E&P when it grows up.

Which brings us to USAC and J-W. The deal has the same family resemblance, but the value creation tightens a different part of the system. That distinction matters more than it looks at first glance.

Let’s briefly put on the investment banking hat.

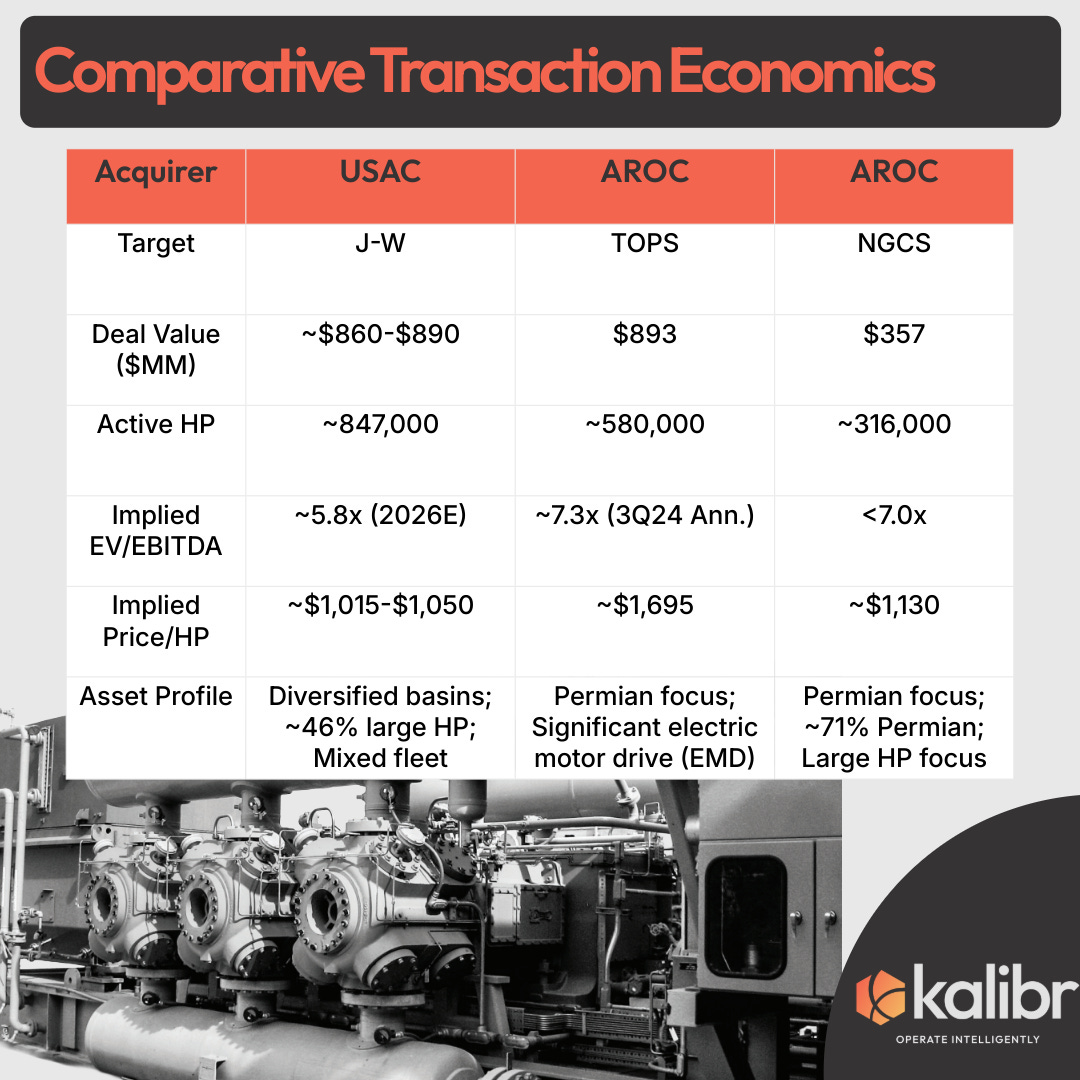

The transaction values J-W between $860 million and $890 million, split evenly between cash from the revolving credit facility and new common unit issuance. The implied valuation is roughly 5.8x 2026E EBITDA and approximately $150 million of adjusted EBITDA in 2026. That multiple sits meaningfully below recent compression comps.

USAC effectively arbitraged its own 9.0x trading multiple to acquire assets at 5.8x, creating immediate balance sheet accretion and supporting a path to sub-4.0x leverage. Part of that discount reflects J-W’s mixed fleet composition, only 46 percent large horsepower versus roughly 75 percent for USAC, and its geographic diversity across the Rockies, Mid-Continent, Northeast, and Gulf Coast.

That difference is critical. Most recent third-party compression consolidation has been tightly focused on large horsepower, electric motor drive, and the Permian Basin. This deal is not.

So what does this mean for E&Ps?

Kalibr takeaway #1: The “Permian pricing power” story is about to get less Permian and more everywhere else

The market has grown comfortable with a tidy narrative. Consolidate large horsepower in the Permian, keep utilization tight, push price. Archrock and Kodiak have executed this well, particularly around large horsepower and electric-drive adjacencies, and the returns reflect it.

USAC’s acquisition of J-W is a reminder that pricing power cannot stay bottled up in one basin and one product class. The deal clears at roughly 5.8x 2026E EBITDA and about $1,015 to $1,050 per horsepower, a clear discount to Archrock’s recent transactions. TOPS transacted at roughly 7.3x and about $1,695 per horsepower. NGCS cleared below 7.0x and around $1,130 per horsepower. That discount is not just asset quality. It is also geography and mix.

J-W is only 46 percent large horsepower and carries meaningful medium and small horsepower exposure. It expands USAC’s footprint well beyond the Permian. If compression pricing is increasingly a function of scarcity and discipline, then USAC just bought the mechanism to export that dynamic into basins and horsepower classes that historically cleared on shorter contracts, higher churn, and more vendor substitution.

The Permian will not lose pricing power. It may lose exclusivity. Operators outside the Permian, and operators with smaller horsepower needs, should assume the Permian experience is coming to a basin near them.

Kalibr takeaway #2: This is not a horsepower acquisition. It is a contract repricing acquisition disguised as M&A

The headlines will focus on triopoly dynamics. The real economics sit inside J-W’s contract book, which reads like a list of correctable terms.

J-W’s average contract tenor is roughly 15 months, versus USAC’s preferred 30 months. Gross margins are about 60 percent at J-W versus roughly 69 percent at USAC. That nine-point gap does not come from a secret operational trick. It comes from pricing, contract structure, and inflation protection that actually works. USAC management has already noted that CPI pass-throughs have historically lagged market rate increases. Translation: the next contracts will look different.

The strategy is straightforward. Acquire a fleet where contracts roll quickly, then migrate those contracts to longer tenor and higher margin under USAC’s standard form. That is value creation you can model without heroics. Layer in the operational option value. The deal includes approximately 50,000 horsepower of idle capacity that can be redeployed with minimal capital, roughly $100 to $300 per horsepower. In a tight market, cheaply deployable horsepower is not an accounting detail. It is a pricing lever.

For E&Ps, this is how consolidation shows up in practice. Not as a dramatic price reset on day one, but as a steady conversion of short-duration, more negotiable contracts into longer, stickier agreements with tighter escalators and higher base rates. Vendor choice does not disappear overnight. Leverage erodes quietly, at renewal.

Kalibr takeaway #3: USAC is positioning itself as the dry gas compression utility, and that pressures peers where they least want pressure

Most observers will frame this as USAC simply getting bigger. The more interesting point is what USAC is becoming.

Pre-deal, roughly 74 percent of USAC’s exposure was Permian. J-W is only about 21 percent Permian. Pro forma, the combined company is meaningfully less Permian-concentrated and far more present in the Northeast, Rockies, Mid-Continent, and Gulf Coast. The deal positions USAC as a go-to provider for dry gas compression, aligned with investor focus on gas supply growth outside the Permian.

This matters because electrification is real, but the grid is not always cooperative. Electric compression offers lower maintenance and emissions, but power availability and reliability remain binding constraints. USAC’s dual-drive approach monetizes the reality that electrification is uneven and infrastructure arrives on its own timeline. That flexibility is commercially valuable in non-Permian basins where power buildout can be a gating factor.

The broader implication is subtle but important. Pricing power does not disappear. It diffuses. It spreads into other basins, into smaller horsepower, and into a more utility-like model where the largest players do not need to win every Permian bid to win the pricing cycle. Meanwhile, the mid-tier and fragmented end of the market becomes structurally more vulnerable. The removal of J-W as an 850,000 horsepower standalone bridge widens the gap, leaving the next cohort of roughly 500,000 horsepower players and an estimated 2.7 million horsepower fragmented private fleet operating in a world where scale, service infrastructure, and cost of capital matter more than ever.

For operators, the trade-off is familiar. Potentially better reliability and availability from scaled providers, paired with fewer credible alternatives when pushing back on price or terms. Compression was already sticky. This deal makes it stickier and extends that stickiness well beyond the Permian.

Which brings us to the practical question this transaction forces back onto the table. What, exactly, is your plan?

Kalibr’s New Year’s resolution for every oil and gas operator is simple and uncomfortable. Run a serious insourcing analysis. Not because you should immediately own compression, and not because outsourcing is wrong, but because without a quantified inflection point you are negotiating blind. You do not know where ownership begins to win on total cost, reliability, or operational control. In a market where credible third-party alternatives are shrinking, ignorance is not neutral. It is a pricing signal.

At a minimum, an insourcing framework creates leverage. It clarifies which horsepower classes matter, where reliability actually drives value, and how switching costs compound across drilling, completions, and production. It forces answers to basic questions. Do you start with smaller horsepower at the edge of the system, or large horsepower on the critical path? What utilization threshold makes ownership rational? What does incremental uptime actually buy you in barrels, not anecdotes?

Over the coming weeks, we will explore how other capital-intensive industries pulled critical infrastructure back in-house, run the math on different insourcing entry points, and outline strategies operators can use to respond to the growing pricing power of third-party compression. This is not theory. It is arithmetic.

Because in a world of tightening geological runway and relentless scrutiny on LOE, a 70 percent margin on a mission-critical conveyor belt stops looking like a service and starts looking like an opportunity. At some point, rational operators do what manufacturers have always done when a supplier becomes too essential and too profitable. They bring the conveyor belts home.