Nominally Hedged | 1.28.2026: Birkin Bag Economics in the Permian Basin

Your compression vendor is approaching Hermès margins. You are not getting a handbag.

Last week, I made a simple suggestion: run a serious insourcing analysis on compression. Not because you should immediately own compression. Not because outsourcing is inherently wrong. But because without a quantified inflection point, you are negotiating blind.

Someone on LinkedIn disagreed.

The pushback went something like this: compression providers have economies of scale, specialized labor, and OEM purchasing power that E&Ps cannot replicate. Insourcing is a distraction. Stick to your knitting.

This is a reasonable-sounding objection. It is also the exact objection your compression vendor hopes you find persuasive. They have, after all, spent considerable effort making sure it sounds reasonable. Their investor decks are filled with reassuring charts about “customer stickiness” and “barriers to entry.” I would be worried about barriers to entry too, if my business model depended on customers not doing arithmetic.

Since I lean contrarian on almost everything, let’s do the arithmetic.

The Part Where We Establish That Something Funny Is Going On

Here is what we know. USAC reported average rental rates of $21.46 per horsepower per month in Q3 2025, up 4% year-over-year. Natural Gas Services Group, which focuses on high-spec fleets, reported $27.08. Jefferies uses $25.00 as their base modeling assumption. Kalibr typically pegs large unit rentals at $40,000 to $45,000 a month for 1,500-2,000 HP packages.

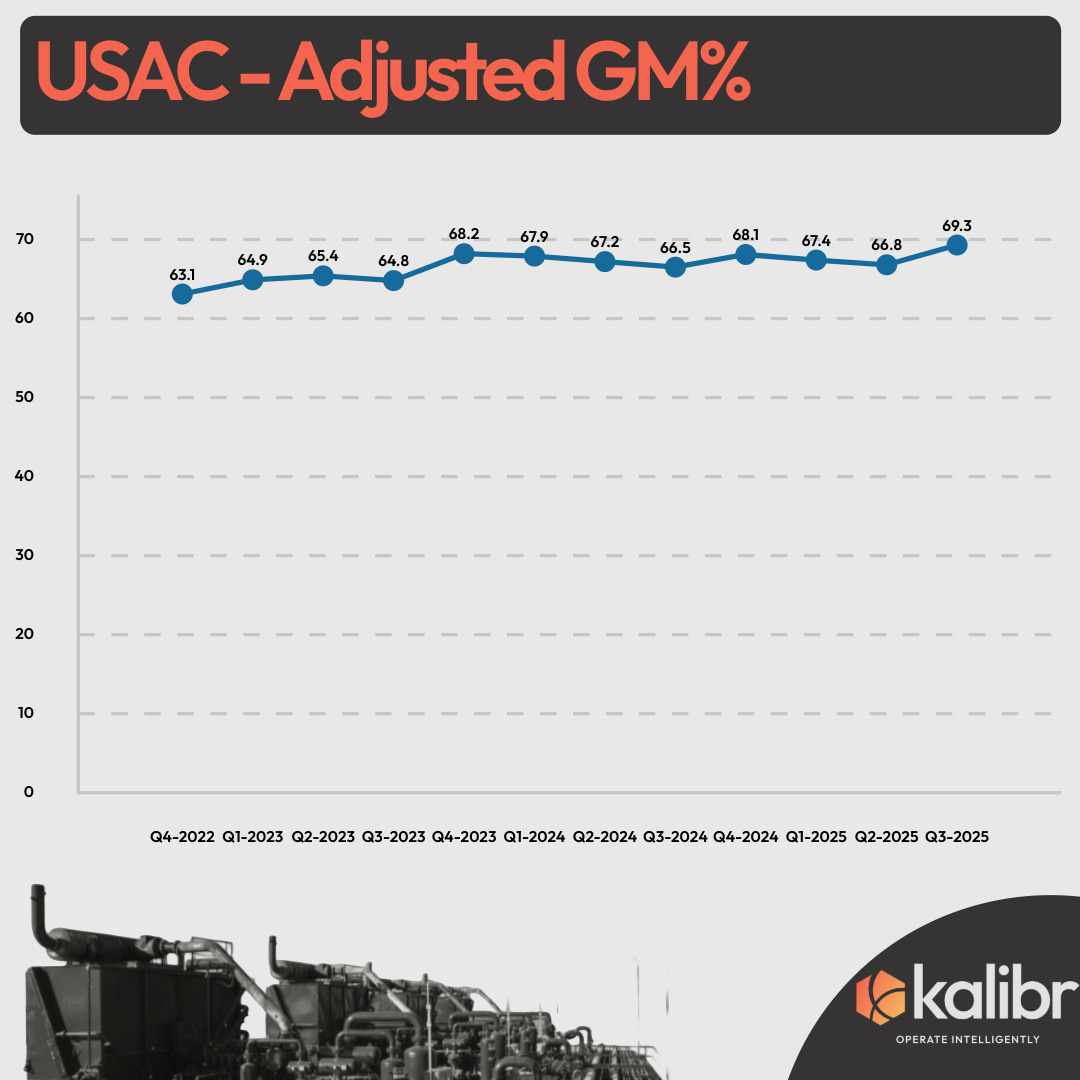

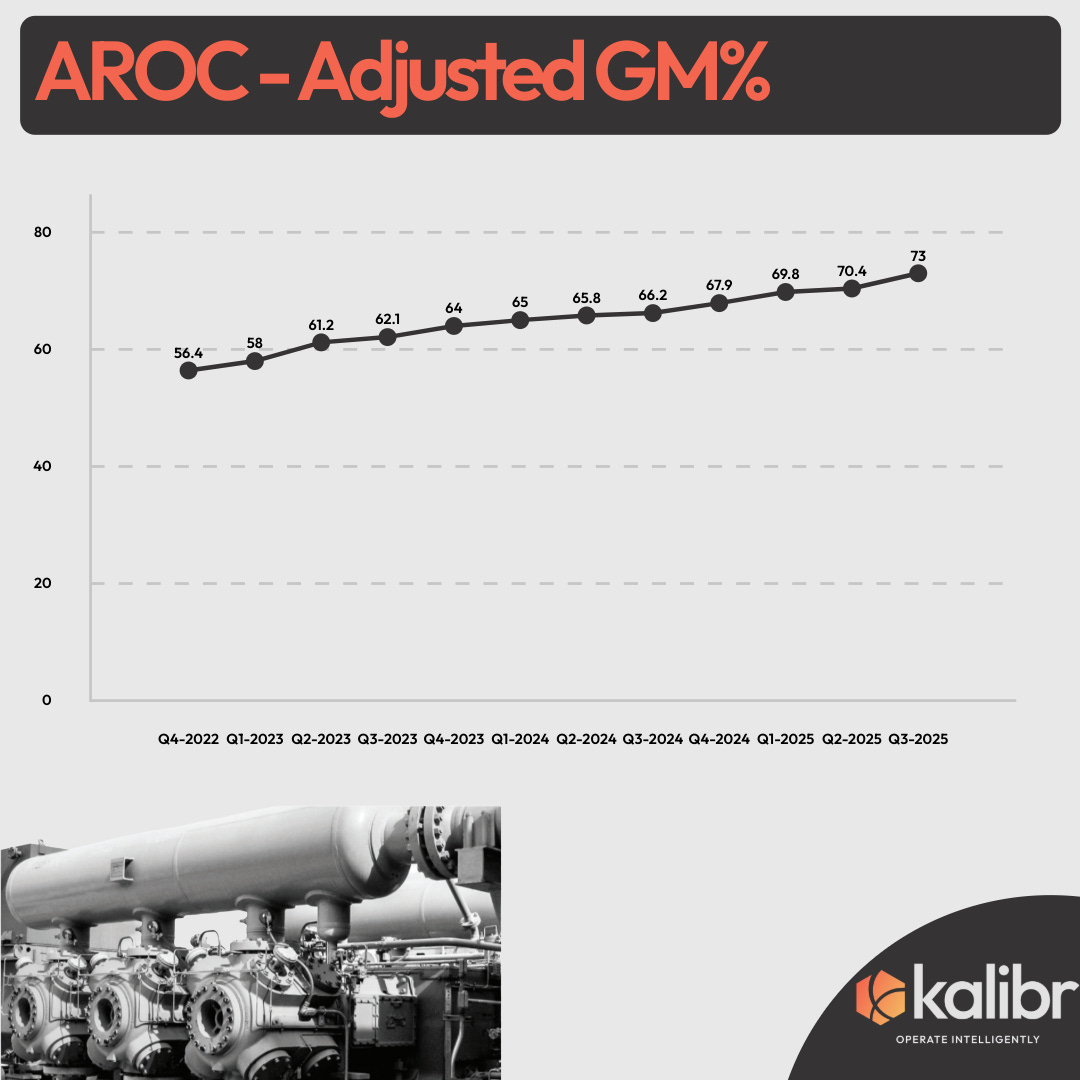

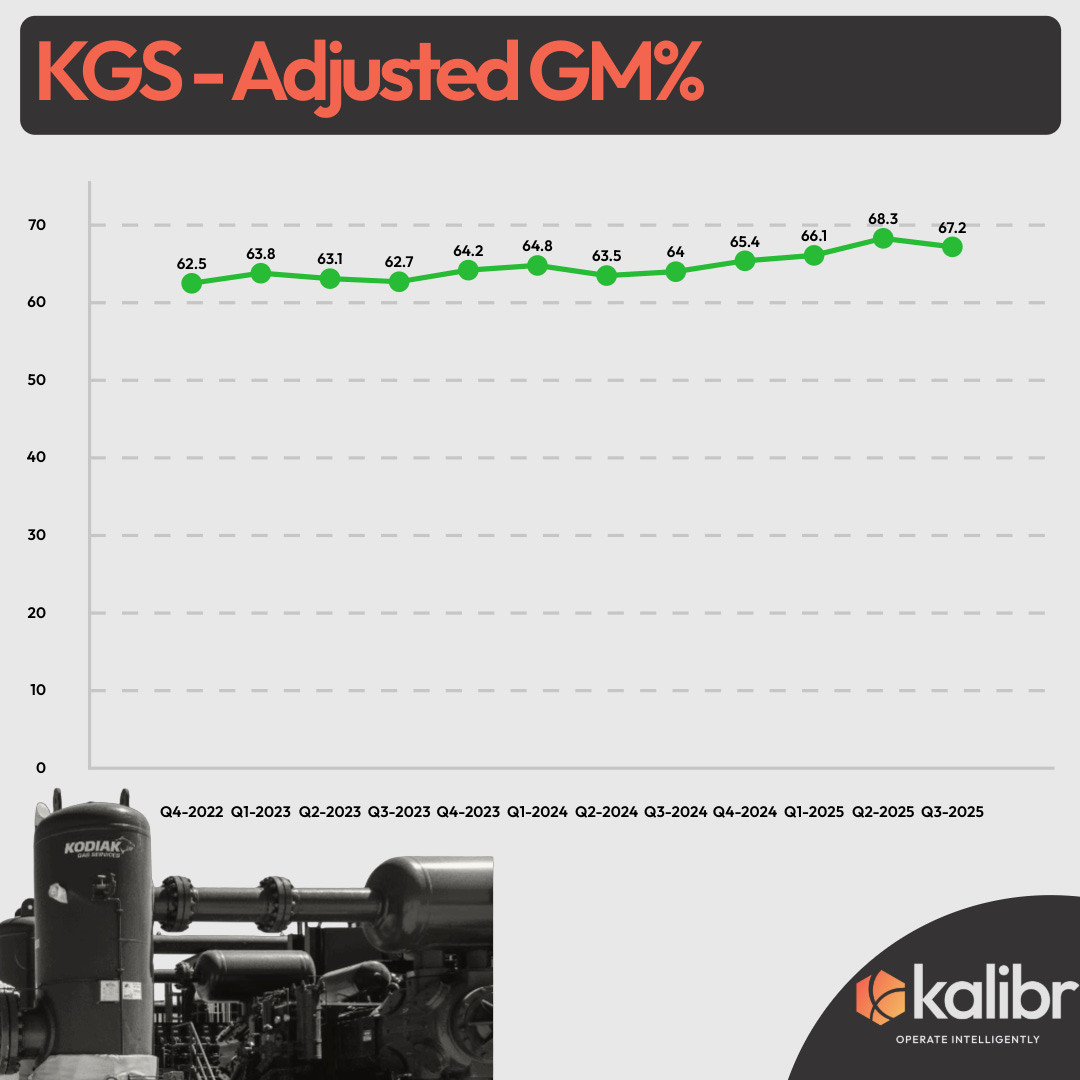

Meanwhile, Kodiak Gas Services achieved an adjusted gross margin of 68.3% in its Contract Services segment. USAC reported 69.3%.

I want to dwell on this for a moment. Sixty-eight percent gross margins. In a business that involves owning steel and sending technicians to remote locations. For context, Apple’s gross margin is 46%. Hermes, the luxury goods company whose customers pay $10,000 for a handbag because it has a horse on it, runs 72% gross margins. Your compression vendor is approaching Birkin bag economics.

Large horsepower utilization is running at 97% to 99%. Lead times for new Caterpillar 3600 series engines have stretched to nearly 60 weeks. Kodiak management has explicitly referenced a 15% to 20% premium for new unit deployments, reflecting what they call the cost of “excess optionality.” That is a nice way of saying “you need this, you need it now, and we both know you have no alternative.”

Put differently: you are paying record rates, your vendor is earning record margins, and there is no credible supply response coming anytime soon.

The question is not whether compression providers have built a good business. They obviously have. The question is whether that good business is built, in part, on the assumption that you will never pull out a calculator.

The Part Where We Pull Out a Calculator

Let’s build a baseline. A standard 1,000 HP compression package at current newbuild costs runs approximately $1,200 per horsepower, or $1.2 million per unit. Electric motor drive packages are cheaper still: $2.0 to $2.2 million for large units versus $2.5 million for gas-fired equivalents, a $300,000 to $500,000 savings because electric motors are simpler than Caterpillar engines.

Operating costs for owned compression vary by drive type. A safe, Kalibr assumption pegs direct operating cost for large gas-fired units at approximately $30,000 per month. Electric units run $15,000 to $20,000 per month because you eliminate engine oil changes and reduce mechanical complexity. Here is the fun part: in the first few months of operation, electric unit OpEx can run as low as $3,000/month. The $30,000 figure is a lifecycle average that includes major overhauls in Years 5-7. Year 1 is considerably more profitable than Year 7.

Now let’s talk about what you are actually paying to lease. Kalibr’s market standard is around $25.00 per HP per month. And here is the detail that most models miss: KGS management explicitly noted that CPI pass-throughs have historically lagged market rate increases. Real escalation has been running 4-5% annually, not the 3% your contract nominally references. Your Year 7 rate is not what your spreadsheet says it is. It is worse.

The comparison:

Lease Scenario (10 years, 1,000 HP)

Monthly rental rate: $25.00/HP/month

Annual escalator: 4.0%

Total undiscounted cash outflow: $3.6 million

Buy Scenario (10 years, 1,000 HP)

Upfront CapEx: $1.2 million

Operating cost: $6.50/HP/month (electric/blended fleet assumption)

Residual value at Year 10: 40% of initial CapEx ($480,000)

Total undiscounted net cash outflow: $0.78 million

The Net Present Value of “Buy” versus “Lease” at a 10% discount rate:

7-year horizon: $285,000 — Buy wins comfortably

10-year horizon: $580,000 — Buy wins decisively

12-year horizon: $820,000 — At this point you’re just lighting money on fire by leasing

The Internal Rate of Return on the insourcing investment:

7 years: 16.2%

10 years: 19.4%

12 years: 21.1%

Simple payback: 4.8 years. For operators running 10,000 HP or more, that is $2.8 million in NPV capture at 10 years. Scale that to a 50,000 HP program and you are looking at $14 million of value creation. For a 100,000 HP program, $29 million.

This aligns with Jefferies’ analysis of Kinetik Holdings, which estimated a roughly 6x build multiple on owned compression, saving approximately $30 million per year on $180 million of CapEx. That is a 16.7% return on compression capital. In perpetuity. Achieved by a company with concentrated Delaware Basin acreage and a long development runway.

Now, I can already hear the objections forming. “But Ian, surely it can’t be that simple. Surely the compression providers have thought of this.” They have. They think about it constantly. The word “insourcing” has appeared over 200 times in compression industry earnings transcripts since 2023. It is the monster under their bed. They mention it because their investors keep asking about it, and their investors keep asking about it because the math is becoming obvious to everyone except, apparently, the people writing the checks.

What the People Who Actually Know Things Say

The provider economics are interesting. But what do the people who run these businesses think about insourcing?

Start with the industry rule of thumb. Per a VP in the Compression Industry'; “It’s typically looked at on a seven-year model. If it’s over seven years, the owner would want to buy the compression because that’s going to be the most economical for them.”

Seven years. Not ten. Not twelve. Seven. That is the compression industry’s own internal benchmark for when ownership wins. It is a fascinating number because it is not in any investor deck. It is just something everyone inside the industry knows.

On operating costs, the numbers are more favorable to ownership than headline figures suggest. The $30,000/month figure is a lifecycle average incorporating major overhauls. For new equipment, costs are a lot lower. Year 1 operating costs for a well-maintained unit run closer to $18,000-22,000/month before the first major PM cycle.

Electric motor drive units change the math entirely. The research pegged electric operating costs at $15,000 to $20,000 per month over the lifecycle, versus $30,000 for gas-fired. If you have grid access and can deploy electric motor drive compression, your NPV advantage versus leasing is not $580,000 per 1,000 HP. It is closer to $820,000. The spread widens because you are saving on both CapEx and OpEx simultaneously.

On switching costs, the data cuts both ways. Mobilization runs $40,000 to $100,000 depending on the unit. All-in swap costs approach $120,000 when you include crane, crew, and downtime. This stickiness is the core of the provider business model: once you are in, you are in. But the same stickiness protects owned assets from competitive displacement. Every month you operate past the mobilization sunk cost is pure margin capture. The switching cost that traps you in a lease is the same switching cost that protects your owned equipment from being swapped out.

Where the Critics Are Right, Where They Are Wrong, and Where They Are Arguing in Bad Faith

The LinkedIn skeptic raised three objections. Two are reasonable. One is something your vendor’s IR team crafted specifically to sound reasonable.

Objection 1: “Providers have superior purchasing power and supply chain access.”

This is true. Kodiak noted that lead times for new engines have stretched to 60+ weeks, creating a barrier to entry for individual buyers. But this objection assumes E&Ps cannot plan ahead. Kinetik successfully secured deposits for incremental compression delivery in 2026-2027 by integrating procurement into their long-term infrastructure planning. If your development model is a “manufacturing model” with multi-year visibility, you can plan ahead. You are not buying a compressor for next Tuesday. You are buying it for 2028.

More importantly, the supply chain constraint cuts both ways. If you cannot get equipment quickly, neither can your vendor. The scarcity premium embedded in rental rates is the same scarcity premium that would protect the value of your owned assets. Scarcity is not a reason to lease. Scarcity is a reason to own.

Objection 2: “Owned assets distract from core drilling returns (ROIC dilution).”

This is the standard corporate finance objection, and it holds if the E&P is capital constrained. If you have $100 million and can only either drill wells or buy compressors, drill the wells. Wells are your business.

But for investment-grade operators, the lease-versus-buy spread has widened to the point where the implied payback on ownership is approaching 5 years. That is a viable infrastructure return profile for operators with long-life inventory. Devon Energy allocates $100 to $115 million annually solely for compression and gathering infrastructure in the Delaware Basin. At some point, you stop being capital constrained and start being margin constrained. At 68% vendor margins, you are margin constrained.

And here is the thing that gets surprisingly little airtime: buy versus lease is not binary. There is a third path.

Some operators work with equipment financing groups or bank leasing structures that essentially outlay capital and rent back at cost. The financing entity takes the depreciation, the operator gets a fixed monthly rate without the 68% margin baked in, and the residual risk is shared or transferred. Think of it as synthetic ownership without the balance sheet impact. It is the DEC playbook applied to oilfield equipment: turn a capital purchase into a structured finance product, fund at investment-grade rates, and capture the spread between your cost of capital and the provider’s required return.

Another strategic pathway in the gray is co-investment. Kodiak Gas Services disclosed a recent agreement with an investment-grade E&P to co-invest in a new compressor station under a 50/50 ownership structure. The E&P preserves capital while Kodiak operates the entire facility. The E&P gets ownership economics without full operational burden. Kodiak gets contracted utilization and a committed customer. Everyone wins except the pure-play outsourcing model.

The point is that capital structure creativity exists. If your CFO is framing this as “own it or rent it,” the analysis is incomplete. The correct framing is “own it, rent it, finance it, co-invest it, or some combination thereof.” The worst option is not knowing which one is right.

Objection 3: “Technical complexity requires specialized 24/7 support.”

Providers cite the shortage of skilled technicians as a persistent operational risk they are better equipped to manage through centralized training academies.

This is the validity check. And it is fair. Kinetik asserts they have achieved a scale where they possess the mechanics, capability, and spares to maintain high uptime internally. But that narrative only works for E&Ps with concentrated geographic footprints where technician travel time is minimized.

Here is what the critics miss: the counterargument to insourcing assumes you are replicating the provider’s entire business model. That is the wrong frame. The question is not whether you can become Kodiak. The question is whether you can own the baseload horsepower required for your core production wedge while leasing the variable peak horsepower required for flush production and new pad bring-online.

Own the minimum. Lease the surge. Capture the margin on what you know will run for a decade, and preserve flexibility on what might not. This is not “insourcing versus outsourcing.” It is more portfolio optimization.

The Utilization Sensitivity Is More Forgiving Than You Think

The base case assumes 95% utilization, consistent with current tight market conditions. At that level, the Buy scenario saves approximately $220/HP/year versus leasing.

But here is the counterintuitive finding: the break-even utilization is far lower than most operators assume.

At 90% utilization: Buy still wins with positive NPV at 7 years

At 85% utilization: Buy breaks even at 8 years, wins thereafter

At 80% utilization: Buy breaks even at 10 years

The reason the threshold is so forgiving is the margin embedded in rental rates. When your vendor is earning 68% gross margins, you have a lot of room to operate less efficiently and still come out ahead. You do not need to run compression like Kodiak runs compression. You need to run it 80% as well, and you win.

This is where the manufacturing model becomes operationally determinative. The shift to multi-well pads allows a single, owned central compression station to service 10-20 wells. Even if individual well variance exists, the aggregate pad volume remains stable enough to justify ownership.

EQT’s “Combo-Development” strategy exemplifies this: contiguous acreage drilled in large-scale pads generating 600+ MMcfe/d of volume impact. That operational density allows shared infrastructure planning and long line-of-sight on logistics. When you know what your gas volumes will look like in 2032, you can own the compression that will move them.

The risk framework is straightforward: concentration de-risks utilization. If your development model has shifted from wildcat delineation to industrial-scale harvesting, you have already built the production wedge that makes ownership rational.

The Hybrid Playbook for Operators Who Actually Think About This

The most sophisticated operators are not choosing between lease and buy. They are choosing both.

Kodiak’s 50/50 co-investment structure is one example. But the hybrid playbook extends further.

Base-Load/Peak-Shave Model: Own the minimum continuous horsepower required for your core production wedge. Lease the variable “peak” horsepower required for flush production and new pad bring-online phases. This aligns capital commitment with production certainty and insulates your base volumes from rental rate inflation. It is also the structure that most resembles how you already think about hedging commodity exposure.

Bank Leasing Structures: Work with equipment financing groups that outlay capital and rent back at cost-plus. The financing entity takes depreciation, you get a fixed monthly rate without the 68% provider margin, and residual risk is transferred. This is synthetic ownership for operators who cannot or will not carry compression on the balance sheet. It is also the structure most likely to make your compression vendor nervous, because it unbundles the financing from the operating margin.

Managed Services with Owned Assets: Buy the equipment but outsource maintenance to a provider under a fixed-fee contract. Comprehensive maintenance contracts are typically priced at 4% to 8% of the unit’s ex-works price annually. That is $48,000 to $96,000 per year for a $1.2 million unit, compared to $90,000+ in embedded margin you pay in a full-service lease. You capture the ownership economics while outsourcing the operational complexity.

The purest expression of the insight is not “insource everything” or “outsource everything.” It is to own the infrastructure whose utilization you control and can predict, and to lease the infrastructure whose utilization depends on factors outside your control.

For a Permian operator with concentrated acreage, rising GORs, and a decade of development runway, baseload compression looks like infrastructure. Own it.

For a Haynesville operator with steep decline curves and commodity-sensitive drilling activity, variable compression looks like a service. Lease it.

For most operators, the answer is some of each. The wrong answer is not knowing where the line is.

The Kalibr Takeaway

The math has shifted. At current rental rates, escalation trends, and provider margins, insourcing compression is no longer a niche strategy for integrated midstream players. It is a legitimate capital allocation decision for any operator with concentrated acreage, predictable production profiles, and a 7+ year development horizon.

The numbers are stark: 19% IRR at 10 years, $580,000 NPV per 1,000 HP, and a break-even utilization threshold below 85%. For a 50,000 HP program, that is $14 million in value creation. For a 100,000 HP program, $29 million. At some point, this stops being a negotiating tactic and starts being fiduciary negligence to ignore.

But the more interesting point is strategic. Running a serious insourcing analysis is not the same as committing to insource. It is about knowing where the line is. It is about understanding which horsepower classes matter, where reliability actually drives value, and how switching costs compound across your system.

At a minimum, the analysis creates leverage. Your vendor should not assume you are captive. They should believe you have a Plan B. And if the Plan B pencils out at 19% IRR, maybe it should be Plan A.

Because here is what the compression providers know that you might not: at 68% margins and 98% utilization, every incremental point of market share lost to insourcing costs them real money. They mention “insourcing” on every earnings call. It is keeping them awake at night.

Maybe it should keep you awake too. Not because insourcing is the answer, but because not knowing the math means you are negotiating with one hand tied behind your back.

And in a market where the conveyor belt costs more every quarter, ignorance is not neutral.

It is a pricing signal your vendor reads every time you sign a renewal.