Nominally Hedged | 1.21.2026: Running Out of Red

Devon, Coterra, and the Strategic Logic of Aggregating Depletion

The Red Widget Problem

Say you start a business manufacturing widgets. You survey the landscape to evaluate which widgets are in the market: red, blue, green, yellow. Rather than make all of them, you decide to focus on one. Red widgets. This is good. The market tends to reward specificity, so they like you focusing on a color. Index funds want “pure-play red widget exposure.” Analysts write initiations with “Red Widget” in the title. Your stock gets a ticker symbol. Things are going well.

You focus extremely hard on driving down the unit cost of that red widget compared to other red widget makers. You make the widget better. Cheaper. Faster. Wall Street loves this. Your multiple expands. Everything is great.

Except.

There’s a large caveat to your manufacturing process versus most others. There is not an infinite amount of raw material to make your red widget. The stuff you need? It’s finite. And you’ve been using the best stuff first, because of course you have. Year one, you make widgets from premium-grade raw material and each widget comes out perfect. Year five, you’re still technically making red widgets, but you’re using slightly worse raw material, and the widgets are measurably, quantifiably 6% less good than the widgets you made in year one. By year ten, you’re down 15% from peak widget quality.

So a natural first step might be to go to other red widget makers and combine. Now you have more red widget raw material to show investors. “Look, we can make widgets for longer now!” you announce on the earnings call. Additionally, you have more scale to drive down your cost to make the red widget. Merge the supply chains, fire duplicate widget inspectors, buy your widget-making machines in bulk.

This doesn’t solve your red widget scarcity problem. But it does buy time. You’ve extended your runway.

Eventually, you’re at a fork in the road. Do you continue the strategic focus you’ve been rewarded for, making red widgets, or do you decide to get into the blue widget business? After all, people need widgets. And isn’t it better to have red and blue widgets than no widgets at all?

Wall Street hates this. “You’re a red widget company,” the activists yell. “Divest blue! Return to core competency! Simplify the story!” But you know something they don’t. The red widget raw material is running out faster than anyone wants to admit. And when it runs out completely, you’d rather be the company making multiple colors than the company making nothing.

This is obviously oil and gas I’m talking about. Devon Energy and Coterra Energy. Barrels instead of widgets. Tier 1 Delaware Basin rock instead of premium raw material.

And look, the past few years have been exactly that first-step playbook. Red widget makers calling other red widget makers. Exxon-Pioneer. Chevron-Hess. Diamondback-Endeavor. Consolidating contiguous positions, eliminating duplicate costs, drilling longer laterals across combined acreage. Classic operational harvest of the best remaining rock.

But something shifted. SM Energy and Civitas Resources was the inflection point. That deal wasn’t about contiguous acreage or operational synergies. SM was Permian and Eagle Ford. Civitas was Midland and DJ Basin. Geographic complexity that activists hate. Most analyst called it achieving scale at a steep cost with “imited operational synergies. But SM did it anyway, because standing alone with inventory questions was worse than adding basins to the map.

Now we’ve got Devon-Coterra merger talks. Different companies, slightly different basins, but the same underlying thesis. It doesn’t sing exactly like SM-Civitas. But it rhymes. And the rhyme scheme is: we’re running out of the good stuff faster than efficiency gains can offset, so let’s combine piles of progressively-less-good stuff and call it duration.

The market is starting to notice the raw material is depleting. And the strategic playbook is changing in response.

Kicking The Can Down A Longer Road

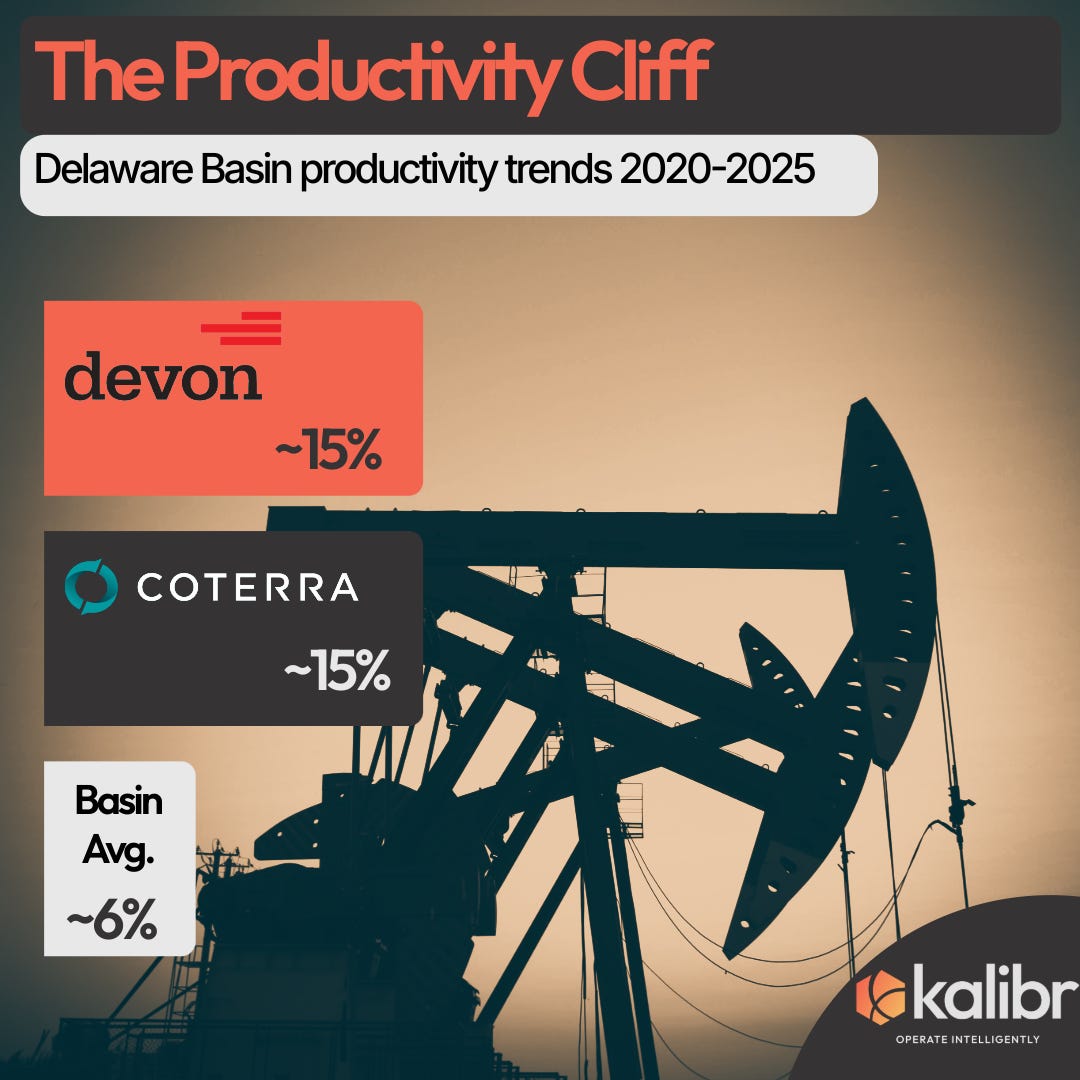

Jefferies published research in January 2026 quantifying what everyone in the Delaware Basin already understood intuitively. Basin-wide productivity declined 6% year-over-year. Operator-specific? Both Devon and Coterra clocked roughly 15% productivity declines in their Delaware assets between 2024 and 2025.

If you’re in the industry, this isn’t news. You’ve seen it in your own well results. You’ve watched EUR guides get quietly revised downward. You’ve sat in engineering meetings where the pressure depletion maps look progressively worse and the parent-child interference is no longer a variable you can model around. It’s just the reality of developing a mature basin.

But here’s what matters. The gap between what the Street thinks is happening and what’s actually happening in the subsurface keeps widening. Sell-side models still assume something close to flat productivity with modest efficiency gains offsetting geological degradation. That worked in 2019. It worked in 2021. It stopped working somewhere in 2023, and by 2025 the math just doesn’t close anymore.

Same rigs. Same or better completion designs. Longer laterals. Bigger fracs. Simul-frac, trimul-frac, every optimization technique that completion engineers spent the last decade perfecting.

The wells are just worse.

This isn’t an execution problem. It’s the rocks. The Tier 1 sweet spots got drilled first because they were the highest-return intervals. High permeability, thick pay, minimal water, no parent-child interference because you were drilling parent wells. What’s left is everything else. Tighter rock, thinner zones, more water, wells that interfere with each other, locations that clear your hurdle rate on a spreadsheet but deliver 15% less oil in practice.

Coterra CEO Tom Jorden acknowledged this in August 2025 when he talked about the industry entering the “final chapter of Tier 1 inventory.” He positioned Coterra as hitting that wall later than peers. But the acknowledgment itself matters. CEOs don’t typically announce their primary product is depleting unless the internal forecasts leave them no choice.

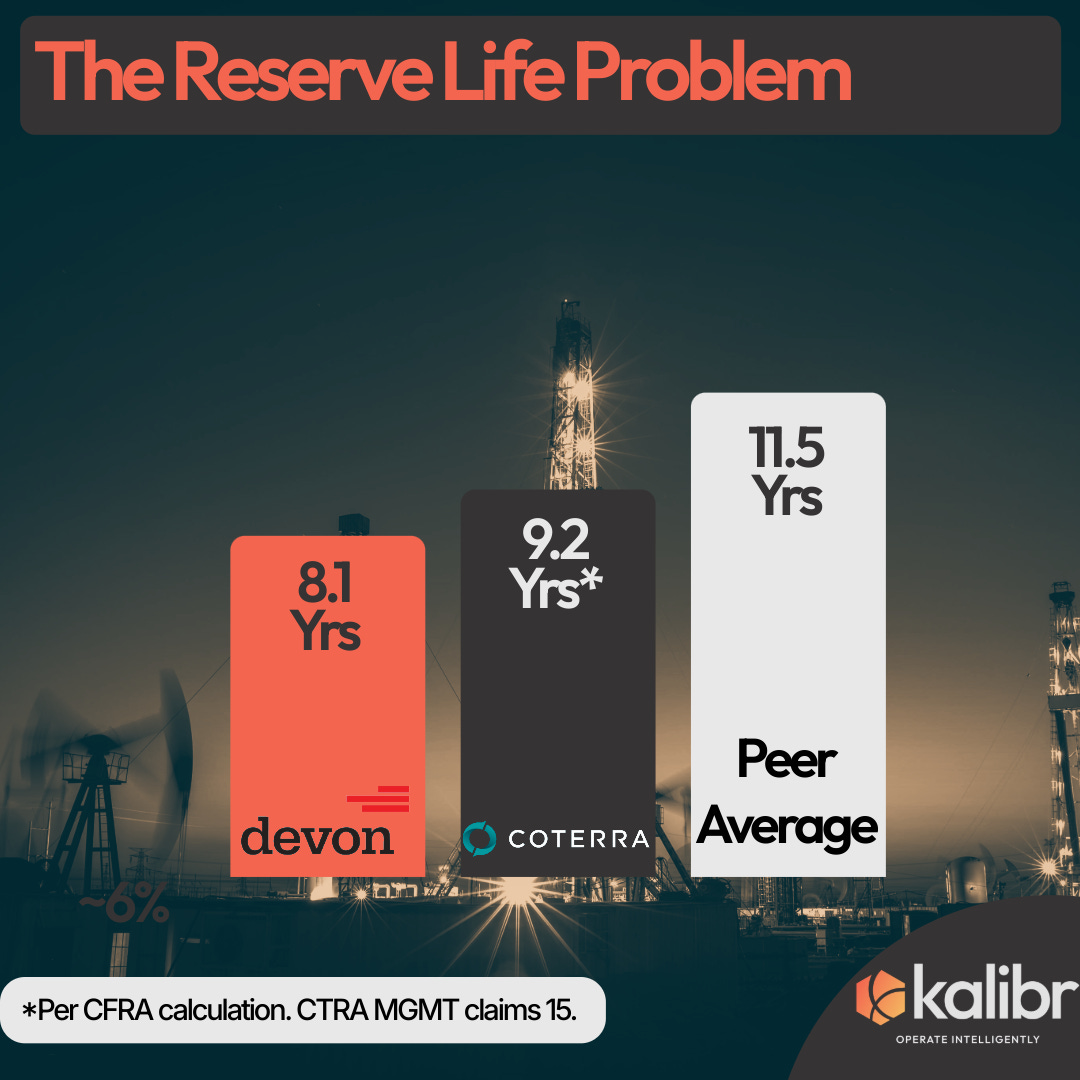

The numbers tell the story. Devon’s reserve life sits at 8.1 years. Peer average is 11.5 years. Coterra claims 15 years in investor decks, but most analysts calculate it at 9.2 years based on actual 2024 production levels.

Both below average. Both acquiring externally to fill gaps. Devon spent $5 billion on Grayson Mill in the Williston, explicitly to extend oil inventory. Coterra spent $3.9 billion on Franklin Mountain and Avant in the northern Delaware, explicitly to boost oil weighting.

When you’re buying externally what you used to develop internally, you’ve crossed a threshold. You’re not growing organically anymore. You’re managing depletion. And the playbook changes.

Balance Sheet Engineering for the Geologically Constrained

So what do you do when organic replenishment can’t keep pace with depletion?

You call your neighbor who has the exact same problem and propose combining countdown clocks.

Devon has 8.1 years of reserve life. Coterra has 9.2 years (Although management claims 15-years). Neither can extend that runway organically at the pace Wall Street expects. Wall Street wants flat-to-growing production and 10% free cash flow yields. The math doesn’t work if you’re drilling progressively worse wells each year.

So they merge. Not to drill monster laterals across newly contiguous acreage. Not to eliminate duplicate finance teams or consolidate gathering contracts. Those savings exist but they’re rounding errors. The actual strategic value is portfolio duration extension through asset aggregation.

This is balance sheet engineering masquerading as industrial logic. You have an 8-year bond. Your neighbor has a 9-year bond. Stapling them together doesn’t create a 17-year bond. But it does create a blended maturity profile that looks more durable than either standalone, especially to investors who don’t stress-test your reserve replacement assumptions every quarter.

This deal would be less about operational synergies and more about securing remaining Tier 1 resource life.

To be clear, I am not knocking the deal. That’s reality. When the constraint shifts from capital to geology, the strategic response shifts from optimization to aggregation. You’re not buying synergies. You’re buying time. And in a depleting resource business, time measured in years of drilling inventory might be the only asset worth acquiring.

The Strategic Value of Complicated (Ask SM Energy)

Devon-Coterra isn’t unique. SM Energy and Civitas Resources announced their merger in November 2025 with the same fingerprints all over it.

Many analysts called it “achieving scale at a steep cost” and noted “limited operational synergies” because there’s virtually no contiguous acreage. SM’s positions were Permian and Eagle Ford. Civitas was southern Midland and DJ Basin. The deal added geographic complexity, the thing activist investors spend entire presentations screaming about.

SM did it anyway. Because standing alone with compressed inventory depth and fielding quarterly questions about how many Tier 1 locations you really have left is worse than adding the DJ Basin to your map and buying 18 months of narrative breathing room.

Both deals have identical architecture. Geographic complexity over simplification. Inventory aggregation over operational synergy. Duration extension over growth creation. Scale as defense over efficiency as edge.

It is clear current M&A prioritizes absolute scale over substantial operational synergies.

That’s the shift. The 2022-2023 consolidation wave was about operational harvest. Exxon-Pioneer, Chevron-Hess, Diamondback-Endeavor. Those were deals where companies bought their neighbors, eliminated costs, drilled longer laterals across combined acreage, and printed cash from premium rock.

This wave is different. This is inventory accumulation when the inventory itself is degrading. You’re not optimizing red widget manufacturing anymore. You’re buying other red widget companies because everyone’s running out of premium red widget material at roughly the same rate, and having two piles of mediocre material sounds better than one pile.

Rational adaptation to a binding geological constraint.

The Venezuela Cost Curve (Under New Management)

Now let’s talk about the external threat that every E&P CFO is modeling privately but nobody discusses on earnings calls.

January 3, 2026. U.S. forces capture Nicolás Maduro. Trump’s response comes in two parts. First, impose a total blockade on Venezuelan oil tankers. Short-term supply tightness, WTI spikes briefly, everyone feels good. Second, signal intent to restore Venezuelan production under U.S. oversight. Long-term supply threat, prices compress, Permian margins evaporate.

The economics matter because they’re structural, not cyclical.

Venezuelan lifting costs run $20 to $30 per barrel once infrastructure gets operational. Permian Tier 1 costs, back when Tier 1 actually existed in meaningful quantities, were $45 to $55 per barrel. Permian Tier 2 costs today run $65 to $75 per barrel. Marginal Permian locations push $75 per barrel and higher.

Trump’s stated price target to combat inflation? $50 per barrel.

Restoring Venezuelan production to meaningful levels isn’t immediate. It requires an estimated $100 billion in infrastructure investment. The country’s oil sector has been decaying for two decades. You don’t flip a switch and produce 2 million barrels per day. Early projections are modest. Maybe 0.5 million barrels per day growth over three to five years. Not a flood. But not nothing either.

Here’s the thing though. Firms don’t plan for base cases. They plan for tail risks. And the tail risk here is that Venezuelan barrels currently flowing to China via shadow tankers redirect to U.S. Gulf Coast refiners, creating a new anchor point on the global cost curve at $25 per barrel just as North American operators are nursing marginal costs toward $80 per barrel.

You can’t hedge that operationally.

You can’t complete-optimize your way out of a structural cost curve disadvantage.

You can’t drill your way to profitability if the global marginal barrel costs $30 and yours costs $75.

The only hedge available is balance sheet scale and durability. Build an entity large enough to survive multi-year commodity price compression if international supply dynamics shift unfavorably.

A combined Devon-Coterra at $53 billion enterprise value provides that buffer. Two separate $25 billion entities don’t.

Many estimate that if WTI hits $45 per barrel, cash flow revisions hit 21% across the E&P sector. Companies with $20 billion market caps and 8-year inventory runways get picked apart by activists or acquired at distressed multiples. Companies with $40 billion market caps and blended 10-year runways survive, retrench, and live to drill another cycle.

You can argue this is pessimistic. Maybe Venezuelan restoration takes longer. Maybe Trump’s $50 target is rhetoric. Maybe Chinese demand growth offsets any new supply. All plausible. But if you’re running an E&P company in 2026 and you’re not modeling the downside case where your marginal cost of production sits $40 per barrel above a credible new supply source, you’re not doing your job.

Scale isn’t just about procurement leverage or index inclusion. It’s about surviving scenarios where the rules change and the cost curve shifts beneath you.

The Service Provider Put

There’s another angle here that matters directly to the bottom line, and it’s the mirror image of what compression providers have been doing to E&Ps for the last three years.

A combined Devon-Coterra controls $6.4 billion in annual capital spend. That’s 9 rigs from Coterra and 14 to 16 from Devon in the Permian Delaware alone. Call it 23 to 25 active rigs. Add 6 to 8 dedicated frac crews across the basin. Plus consolidated Anadarko activity, currently fragmented across two separate 1-rig programs.

That is what we at Kaligr like to call monopsony leverage. The ability to influence market rates through concentrated buying.

Coterra management noted in August 2025 they were witnessing “reductions in market rates driven by increased rig and frac availability leading to competitive pricing in our bids.” Strip away the earnings call language and here’s what that means: as E&Ps consolidate into fewer, larger buyers, service providers face customers with real negotiating leverage.

Devon’s strategy with it’s cost reduction initiatives has been to decouple bundled services to utilize a diversified vendor universe. Operational translation: bypass service integrators. Maybe buy tubulars directly from mills at volume pricing. Or perhaps source sand directly from mines. Use that $6.4 billion buying power to extract concessions from providers who can’t afford to lose a customer that size.

For compression providers, pressure pumpers, drilling contractors, this is the nightmare that started in 2022 and keeps getting worse. Your largest customers are merging into entities with enough scale to dictate terms while your cost structures remain fixed. You’re selling a commodity service to a concentrated buyer base.

For Devon and Coterra, it’s margin defense when you can’t control the revenue line. If you can’t control WTI because some guy in Caracas might decide to start producing again, at least control your well costs. If revenue is threatened from above, squeeze costs from below.

You can’t expand the pie. Fight harder for every basis point of what’s left.

Market Capitalization as Competitive Moat

Devon’s current market cap sits around $22.4 billion. Coterra’s around $19.2 billion. Combined equity value hits roughly $42 billion. Enterprise value pushes $53 billion.

That $50 billion threshold matters. A lot. It’s the difference between “regional mid-cap E&P that requires conviction from active managers” and “investable large-cap with S&P 500 Energy index relevance that attracts passive flows automatically.”

Passive capital flows into energy ETFs and index funds get allocated based on market cap weighting. A $42 billion equity entity pulls materially higher passive inflows than two separate $20 billion entities. The capital doesn’t evaluate rock quality or reserve replacement ratios or inventory depth. It just buys the index weight and rebalances quarterly.

Scale the size of CTRA/DVN would highlight the valuation difference versus large caps, potentially closing Devon’s multiple gap. The company currently trades around 4.7 times EV to discretionary cash flow. Large-cap peers trade closer to 5.5 to 6.0 times.

Is that multiple expansion justified by better operations? No. It’s justified by size as a quality factor in a financialized market. Larger companies aren’t necessarily better operators. But they’re easier to own at institutional scale, more liquid for large position sizes, less volatile for passive strategies, more likely to stay in indices through rebalancing.

This is oil and gas financialization in its purest form (and was at play for SM-CIVI too). When organic growth is constrained, you optimize for capital markets’ structural preferences. And capital markets structurally prefer scale. They prefer names they can put $500 million into without moving the stock. They prefer constituents that won’t get kicked out of indices. They prefer companies large enough that analyst coverage is mandatory, not discretionary.

None of that has anything to do with how good your rocks are or how efficiently you drill wells. But it has everything to do with your cost of capital. And in a capital-intensive, commodity-price-exposed business, cost of capital is the game.

The Optionality Bet: Fighting the Pure-Play Religion

Here’s where Devon-Coterra diverges from what every activist investor with a Wharton MBA thinks they should do.

Kimmeridge Energy has been publicly pressuring Coterra to divest gas assets and become a Permian oil pure-play. Their pitch is clean. Focus creates value. Conglomerates get discounted. Simplify the story. Make it easy for generalist investors to understand. “You’re an oil company or a gas company. Pick one.”

Devon-Coterra is betting the exact opposite.

The combined entity gets oil exposure in Delaware and Williston. Gas exposure in Marcellus and Anadarko. Commodity flexibility to toggle capital allocation between oil and gas based on relative economics and macro conditions.

Both companies have successfully used Anadarko as a flexible dial. Increase gas allocation when NGL and gas spreads justify it. Treat the basin as a high-margin cash generator instead of a growth engine. When oil crashes and gas holds, you have options. When specific basins face regulatory pressure or operational issues or infrastructure constraints, you have alternatives.

The multi-basin model isn’t elegant. It’s messy. Harder to market to investors who want a clean Permian pure-play thesis. Probably commands some conglomerate discount in the multiple.

But it creates commodity optionality. And when external threats are numerous: Venezuelan supply restoration, Trump price targets, regulatory uncertainty, infrastructure bottlenecks, optionality has value. It might not maximize your multiple in bull markets. But it improves survival probability in sustained downturns.

You’re not trying to win the quarter. You’re trying not to lose the decade.

The Kalibr Read

The consensus narrative will frame this as strategic scale creation and enhanced shareholder returns through operational synergies and capital efficiency.

The contrarian reality is simpler. This merger is an acknowledgment that the organic growth phase is over, and the companies that survive the next decade will be the ones that recognized geological constraints earliest and adapted fastest.

For companies facing rock quality degrading 6% to 15% annually in core acreage, reserve life below peer averages and compressing, potential supply competition from international sources at structurally lower cost points, and investor expectations for 10% free cash flow yields with stable-to-growing production, aggregation might be the most rational path available.

Devon and Coterra would be buying time. Measured in years of inventory duration, reserve life extension, runway to generate cash before the next strategic inflection point forces another adaptation.

In a depleting resource business where the best raw material is running out, time might be the most valuable asset left to acquire.

You can’t make more Tier 1 Delaware rock. But you can combine what’s left and manage the depletion curve more efficiently than two separate entities could. You can build enough scale to survive commodity price shocks. You can create enough procurement leverage to squeeze service costs when oil prices don’t cooperate. You can cross market cap thresholds that attract passive flows and lower your cost of capital.

None of that changes the underlying geology. The wells will keep getting worse. The rock will keep depleting. The industry will keep transitioning from growth to harvest.

But if you’re going to harvest, you might as well be the largest, most efficient harvester with the longest runway and the best balance sheet.

That’s not pessimism. That’s adaptation. Every resource basin eventually transitions from discovery to development to maturity to harvest. The Permian is just transitioning faster than anyone expected in 2019. The companies that survive won’t be the ones pretending it’s still 2019. They’ll be the ones that saw the transition coming and built the right structure to manage it.