Known Unknowns | COP Q4 2025: The Machine That Refuses to Flinch

The earnings call where ConocoPhillips told Wall Street it doesn’t have a reaction function, and Wall Street spent 90 minutes trying to find one anyway.

ConocoPhillips just held its Q4 2025 earnings call and delivered the corporate equivalent of a poker player showing you their hand, then daring you to call. Capex at $12 billion. Twenty-four rigs. Eight frac crews. Zero hedges. Mid-40s breakeven. And if prices fall below the $60 planning deck? CEO Ryan Lance would like you to know they’ll lean on their $7.4 billion cash pile rather than touch the rig count, because “we don’t like to whipsaw these programs up or down.”

This is not a company managing volatility. This is a company that has decided volatility is someone else’s problem.

For anyone sitting across the table from a vendor who counts COP as a customer, that posture matters more than any line item in the 10-Q.

The Score

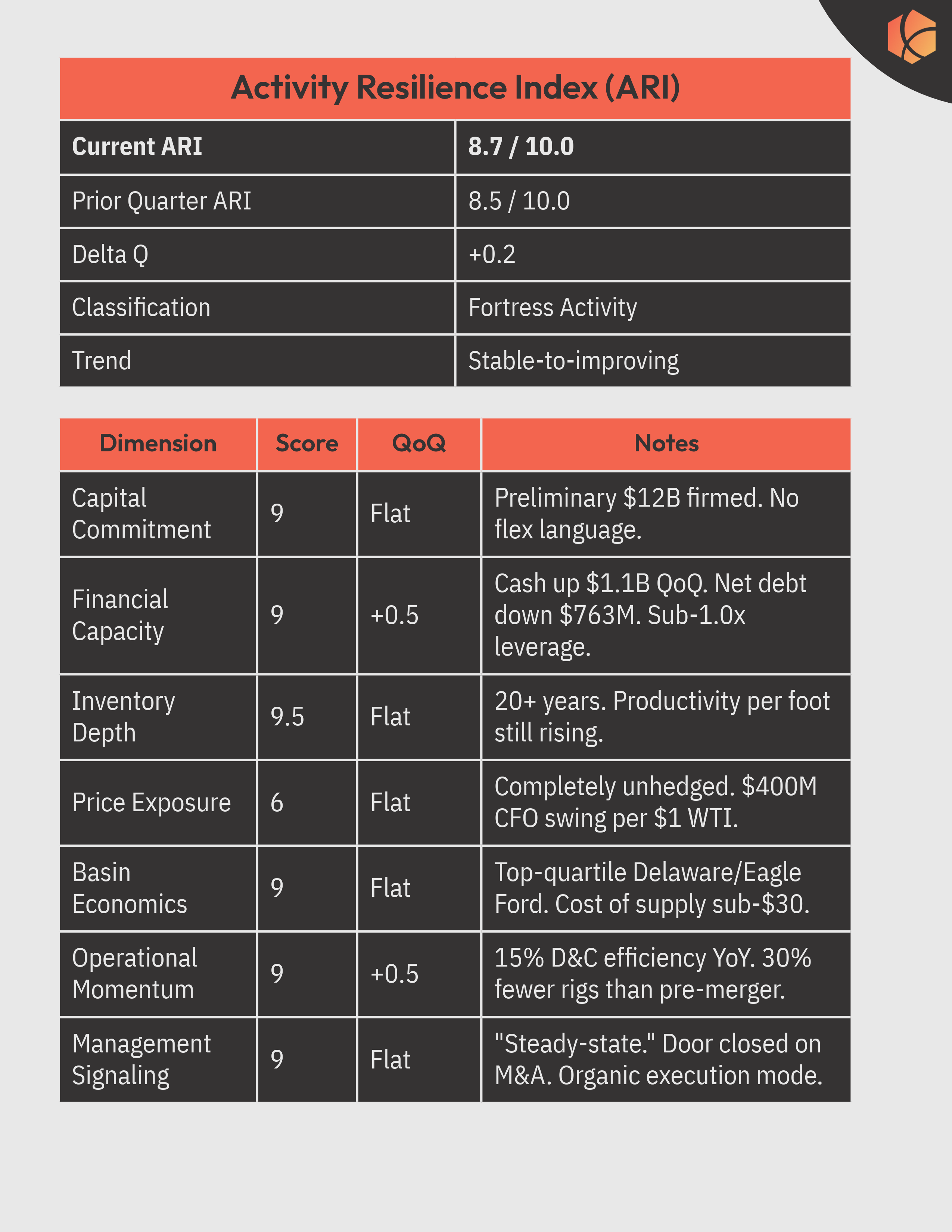

COP ticked up two-tenths of a point, which in Fortress territory is like gaining altitude at 35,000 feet. You’re already above the weather. The improvement came from two places: balance sheet strengthening (cash swelled by $1.1 billion despite buybacks, net debt dropped) and the efficiency story getting harder to argue with (15% D&C improvement, 30% fewer rigs and crews than the two pre-merger companies combined). The only thing holding the score below 9.0 is the unhedged commodity posture, which is a feature, not a bug, from management’s perspective. It does, however, mean that a sustained sub-$50 WTI environment would test the “we don’t whipsaw” commitment faster than Lance’s tone suggests.

What They Said (And What They Meant)

The Anti-Reaction Function

Every analyst on this call was fishing for the same thing: at what price does COP blink? Lloyd Byrne at Jefferies asked it directly. Lance’s answer was the most revealing sentence of the quarter: “We don’t like to whipsaw these programs up or down, and we’ll use the balance sheet in the downside case if we need to.”

Read that again. He’s not saying they won’t cut. He’s saying the balance sheet takes the hit before the rig count does. That is a fundamentally different operating philosophy than most of COP’s peers, and it has direct implications for anyone selling into their supply chain. A vendor servicing COP’s 24-rig program can model that revenue with higher confidence than a vendor servicing a peer running the same rig count but hedging 40% of production and using words like “flexible” on every earnings call.

Last quarter, the language was about “optionality” and a “highly flexible portfolio.” This quarter it shifted to “resilience” and avoiding “whipsaw.” That’s not a subtle change. Optionality implies you might do something different. Resilience implies you won’t. For anyone modeling COP’s forward activity, Q4 just gave you permission to remove the downside scenario from the base case.

The Efficiency Machine Is Real

Betty Jiang at Barclays did the smart thing and pushed on the quality of the efficiency gains. Was the $1.4 billion pro forma capex reduction real savings or just an activity cut dressed up in synergy language? The answer, honestly, was both. Nick Olds broke it down: some of it is structural (Marathon’s rigs got folded into COP’s steady-state program), some is synergy capture ($500 million), some is operational improvement (more wells per rig), and about $200 million is plain deflation.

Here’s why the composition matters for BATNA analysis. The deflation component ($200 million, driven by 30% tubular cost reductions and lower pumping rates) tells you that COP is capturing service cost reductions in real time. They’re not passing that through as margin to vendors. They’re banking it. If you’re a pressure pumping company or a tubular distributor, COP’s procurement team is quantifying the deflation you’re experiencing and adjusting their cost models accordingly. That $200 million is coming out of someone’s revenue line.

The M&A Door Is Closed (And Bolted)

Leo Mariani at Roth asked if COP was still in the market. Lance’s response was as close to “absolutely not” as a public company CEO gets: “We’ve done our heavy lifting on the M&A side over the last 4 to 5 years. We’ve been there, done that.”

This matters for two reasons. First, the $5 billion disposition target (with $3 billion already closed) means COP is a net seller of assets, not a buyer. That capital is flowing into buybacks and debt reduction, not new acreage. Second, a company in organic execution mode has a different relationship with its vendors than a company in integration mode. Integration creates disruption, which creates procurement opportunity. Execution creates cadence, which creates stickiness. COP’s vendor relationships are hardening, not loosening. If you’re already in, that’s good news for your contract duration. If you’re trying to break in, the window is narrower than it was 12 months ago.

The Delta: What Changed Quarter Over Quarter

Free cash flow compressed by 48%, from $2.5 billion to $1.3 billion, entirely driven by realized price deterioration ($42.46/BOE vs. $46.44/BOE prior quarter) and continued Waha gas basis punishment. That’s the number that makes headlines. It’s also the number that doesn’t matter for activity resilience, because COP’s cash balance still grew by $1.1 billion to $7.4 billion thanks to $1.6 billion in asset sale proceeds. Total liquidity expanded to $12.9 billion. Net debt fell $763 million. Management’s tone on capital commitment was firmer, not softer, despite the cash flow compression. The message: the balance sheet absorbed the hit so the operating machine didn’t have to.

The 2026 opex guidance dropped $400 million to $10.2 billion. Willow’s cost estimate crept up to $8.5 to $9.0 billion (from $7.0 to $7.5 billion), mostly North Slope inflation. One number went right, the other went wrong, and neither changed the rig count.

The Kalibr Take

The consensus narrative post-call is that COP is a “safe haven” in a volatile commodity environment. That’s true and it’s also not the interesting part. The interesting part is what COP’s posture does to the rest of the game board. When the largest independent E&P tells the market it will not cut activity in a downturn, it creates an asymmetric information problem for every vendor in the Permian and Eagle Ford. COP’s 24-rig program is “priced in” to every service company’s revenue forecast. That makes COP’s volume reliable but also makes it non-negotiable. The vendors know COP won’t leave. Which means the real leverage for COP isn’t the threat of cutting. It’s the efficiency: they’ll keep drilling, but they’ll keep squeezing unit costs every quarter, and they’ve got the data to prove the deflation is real. COP doesn’t negotiate with a gun. They negotiate with a spreadsheet. That’s harder to defend against.

Kalibr BATNA Translation

COP scores an 8.7 ARI, Fortress classification. For vendors, this is the most durable demand signal in the Lower 48. That sounds like good news for the service company, and it is, right up until the procurement meeting. COP’s activity resilience means they’re not going anywhere. It also means they know they’re not going anywhere, and they know you know it too. The leverage here isn’t about volume risk. It’s about price. COP captured $200 million in service cost deflation this quarter and guided to another $400 million in opex reductions for 2026. Someone is funding that.

If COP is your vendor’s largest customer, their order book is secure but their margins are under pressure. If COP is your peer and you share vendors, understand that those vendors are benchmarking your efficiency against COP’s 15% D&C improvement. The standard just moved.

Act accordingly.

Known Unknowns is Kalibr’s earnings intelligence series. Each post takes a single earnings call, layers it against our Kalibr Pulse activity data, and scores the company through our Activity Resilience Index (ARI): a 7-dimension, 1-to-10 framework that quantifies how likely a company is to sustain its spending on oilfield goods and services over the next 24 months. Most earnings analysis is written for equity investors. This is written for the people negotiating contracts. If you’re an E&P, the ARI tells you how your vendor’s other customers are trending and what that means for your leverage. If you’re a vendor, it tells you which revenue in your book is durable and which is one bad quarter from disappearing. We track the delta because direction matters as much as level.