Kalibr Sweep | Thoughts on SM / CIVI Merger

When scarcity starts writing the M&A playbook

The Civitas–SM Energy merger says a lot about where the shale sector finds itself in late 2025. A few years ago, the consolidation trend had a clear logic: focus on a couple of core basins, simplify the story, and let Wall Street buy you like an ETF. Permian exposure? FANG. Bakken? CHRD. The market rewarded specialization and penalized diversification.

This deal goes the other direction. There’s very little operational overlap and Civitas is stepping into a new basin just as SM did last year. That’s a sharp turn from the indexation logic of 2023 and, to me, a signal that geology is quietly setting the agenda. The highest quality inventory is getting scarce, and operators are finding creative ways to restock even if it means entering regions with more muted multiples or regulatory complexity.

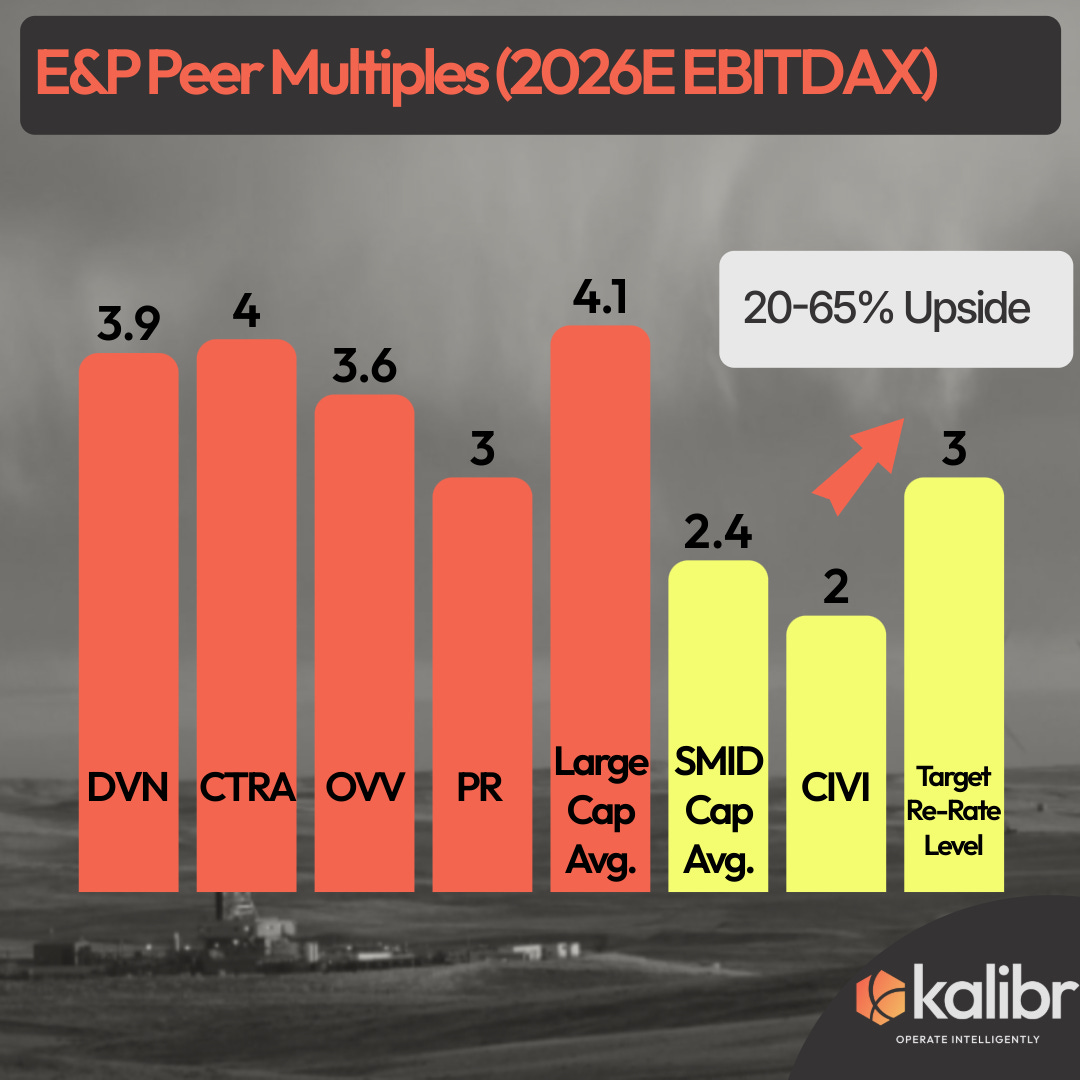

Still, the financial logic is clear. Two SMIDs trading at roughly 2.8× FY26E EBITDA can combine into a platform large enough to compete for capital at closer to 3×, or even 4.8× if the market grants a large-cap re-rate. Even a modest move to 3× implies 65 percent upside before counting operational improvements. Free cash flow yields are projected to expand 15 percent in 2026 and 20 percent in 2027, giving the combined entity more flexibility to manage leverage and dividends.

Synergies are estimated at five percent of transaction value, or about $200 million, which is consistent with recent E&P combinations. Most of that will come from general and administrative savings rather than field operations, helped by the overlapping Denver footprint. Our base case assumes around 310 FTEs consolidated across engineering, land, geology, and accounting. Efficiency gains are real, but the point isn’t just cost savings—it’s balance sheet optimization and capital access.

What makes the transaction interesting is not whether it is “transformational,” but how it reflects a new playbook. With Tier 1 rock harder to find, firms are building value through portfolio construction and index eligibility rather than purely through drilling returns. Civitas and SM are both strong operators with disciplined capital frameworks; together, they buy optionality and scale that could command a better cost of capital.

The industry spent the last few years simplifying. It now seems to be entering a phase where complexity, done well, may be rewarded again.