Nominally Hedged | Cheap Talk

A £60 fuel surcharge, a 1982 paper that explains your vendor's last price increase, and the model that turns a good story back into arithmetic.

Nominally Hedged is Kalibr Partners’ briefing on what oil and gas actually costs: every category, CAPEX to OPEX, proprietary data systems interpreted through a commercial lens (market intelligence data, customized market intelligence reporting, consulting). Whichever side of the negotiating table you sit on, you are the intended reader.

In August 2004, British Airways added a fuel surcharge to its long-haul tickets. It was £5 per round trip, which is to say it was nothing, which is the correct size for a brand-new line item: small enough that nobody calls, large enough to exist. And it was hard to argue with. Oil prices were climbing, jet fuel is refined from oil, airlines buy oceans of jet fuel. This was not a price increase, went the framing. It was a pass-through. A regrettable, temporary, externally imposed pass-through.

By early 2006 the pass-through was £60.

Now, oil really did get more expensive over those eighteen months. That part was true, publicly visible, and repeated on every evening news broadcast in Britain, which was precisely the point. The headline did the persuasive work. A passenger could see that oil was up. What the passenger could not see was how much oil actually flows into the cost of one seat on one 747 to New York, which meant the size of the surcharge was, from the customer’s side of the counter, unverifiable. £5 felt plausible. So did £20. So, apparently, did £60. The number was tethered to nothing except what the story would bear, and the story, it turned out, would bear a 12x increase.

Also, the two airlines were on the phone with each other. I should mention that.

Between August 2004 and January 2006, on at least six occasions, British Airways and Virgin Atlantic informed each other about planned surcharge changes instead of setting them independently. You are not supposed to do that. It is, in fact, extremely illegal. And the scheme ended the way these schemes always end, which is not because customers got smarter. Customers couldn’t get smarter; they had no verification technology, and you cannot out-read a number that means whatever its author says it means. It ended because Virgin walked into the UK Office of Fair Trading in 2006 and confessed, in exchange for full immunity. In August 2007 BA was fined £121.5 million by the OFT (a record at the time, later reduced to £58.5 million on appeal in 2012, which is the kind of detail that matters to BA and to nobody else) and pleaded guilty in the United States to a criminal price-fixing charge carrying a $300 million fine. In 2008, BA and Virgin agreed to refund roughly $210 million to about 7.2 million passengers. One third of the surcharges they had paid. The other two thirds had, presumably, gone to fuel.

I want to be careful about what the crime was, because the careful version is the useful one. Charging more for fuel when fuel is expensive is legal, ordinary, and arguably honest. The fuel surcharge was never the crime. The crime was coordination: the two carriers removed the one mechanism (a competitor willing to undercut an inflated number) that could have checked the number. BA’s chief executive said afterward that passengers “had not been overcharged.”

Sit with that sentence. It is a perfect sentence. If a surcharge means whatever the airline says it means, then no passenger can ever be overcharged, by construction. The defense is the business model.

There is a name for all of this. In 1982, two economists, Vincent Crawford and Joel Sobel, published a paper in Econometrica called “Strategic Information Transmission,” and it became the founding document of what game theorists call cheap talk: communication that is costless, non-binding, and unverifiable. Here is the game. One player knows the true state of the world, say, what its costs actually did. The other player cannot observe the state, hears a message, and writes a check. The catch is a single parameter called bias: the informed player’s preferred outcome sits a little above the truth, in its own favor, always. The vendor does not want you to pay what costs justify. It wants you to pay that, plus something.

You can probably already see the problem, and Crawford and Sobel proved you cannot see your way out of it. Two of their results are worth carrying around for the rest of your career. First: when the sender benefits from your response, there is no equilibrium in which precise claims can be believed. None. Not because salespeople are liars, but because if exact numbers were believed, exact numbers would be inflated, and a rational listener prices the inflation in before the meeting starts. This is the part people miss: it is not a theory of lying. It is worse than that. It is a proof that even a buyer who knows the game cold cannot extract truth from words, because the words are the only thing being offered and the words are free. Second: the bigger the sender’s stake in your overreaction, the less its messages can carry. Communication degrades from numbers into vibes (”costs are up a lot”), and at high enough bias into nothing at all, a state economists call the babbling equilibrium, and your grandmother called the boy who cried wolf, and you may recognize as certain quarterly business reviews.

So: one way to read the BA story is as an antitrust case. Another way to read it is as a 30,000-foot experimental confirmation of a 1982 theorem, in which an unverifiable cost claim, bolted to a true and visible headline, drifted from £5 to £60 because nothing tethered the message to the state. The most expensive thing on the ticket was not fuel. It was the story about fuel.

As part of my job, clients often call with decks they receive that carry a very good story.

Before I tell it, the punchline, because withholding it would be its own kind of cheap talk: we have now run the sequence that follows for a string of clients, against a string of vendors, conflict decks and tariff decks alike, and the surcharge it is built to answer almost always ends at the same number, which is zero. The cumulative figure we have taken off these decks has a couple of commas in it. What follows is how, and why it keeps working.

The Market Designed to Feel Unwinnable

Before the deck, the envelope. I am going to tell you how much money is in it, and then I am going to tell you why almost nobody you employ can verify the number on a single tote of it.

Let’s start with every Production Engineers favorite cost center; chemicals.

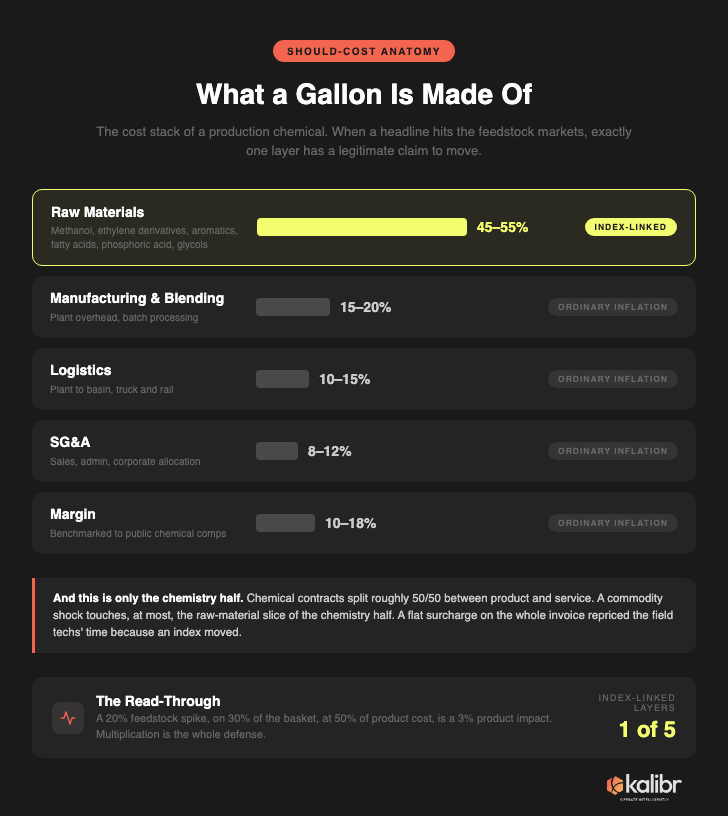

North American E&P operators spend roughly $11.5 billion a year on oilfield chemicals. Call it $2.0 to $2.3 billion of production chemicals (the corrosion inhibitors, scale inhibitors, biocides, H2S scavengers, demulsifiers, and paraffin treatments dripping into your wells right now), with the rest in drilling fluids and stimulation chemistry. This is not an abstraction that lives in a market study. Kalibr benchmarking for a public mid-market Permian operator runs about $0.71 per BOE in chemicals and treating, roughly 6.5% of its LOE. Frac chemistry runs 5 to 10% of horizontal well D&C, in a world where the completion is 54% of the well. Corrosion and scale inhibitors are typically 15 to 20% of total chemical spend. Each.

A real line item, then. Here is the uncomfortable part: it is the worst-audited real line item you have, and it is built that way.

Chemical contracts split roughly 50/50 between the chemistry and the service wrapped around it, the field techs and the monitoring and the formulation knowledge, which means the thing on your invoice is not a commodity with a price. It is a bundle with a narrative. Two suppliers control roughly 40 to 50% of US land production chemistry. Sole-sourcing is the norm, because trialing a new chemistry on producing wells feels like performing surgery to save on bandages. And the slack is not hypothetical: simply auditing an active chemical program yields 5 to 10% in direct savings for the average operator, and automated dosing routinely cuts consumption 15 to 25% by adjusting injection rates more often than a human with a route schedule can. Do the Feynman check on that pair of numbers. If an audit alone finds 5 to 10%, the program was never within a percent or two of right. It was loose by double digits, for years, and the money was simply going. Quietly. With excellent service.

Why does nobody look? Because production chemicals are psychologically miserable to own. You are paying to prevent failures that have not happened, which means the program’s success is indistinguishable from its excess. The internal dialogue runs something like:

Year one: Nothing failed. Are we overtreating? Cut the program.

Year two: An ESP died of scale. Why did we cut the program? Double the program.

Both of those are emotions. Neither is a model. Add switching costs (field trials, residual chemistry risk, a vendor tech who knows your wells better than your own foreman does) and you get a buyer who cannot verify, cannot easily leave, and negotiates from whichever failure is freshest.

Now run the Crawford and Sobel checklist. Every trait above does one of two things: raises the seller’s bias, or lowers the buyer’s ability to verify. Production chemicals are not a market where cheap talk occasionally happens. They are the natural habitat. The only missing ingredient is a headline.

The Part Where the Headline Shows Up on an Invoice

Every few quarters, the world provides one. A tariff schedule. A hurricane in the Gulf. A canal blockage, a port strike, a regional war. The genre is durable because the ingredients are always in stock: a disruption that is real, visible, and quantified daily in the press, attached to a cost claim that is none of those things. You have seen the catalog. The pandemic logistics rider. The tariff adder. The force majeure letter that somehow never arrives when prices fall.

The one that landed on our client’s desk cited a geopolitical conflict, and the supporting evidence was genuinely strong, the way rising oil prices in 2004 were genuinely strong. Feedstock markets convulsed. Chemical majors announced double-digit increases. A global petrochemical index posted its steepest one-month move in decades. None of that was in dispute. Headlines rarely are. That is what makes them load-bearing.

Days into the news cycle, a major service company sent our client a deck. It was a good deck. I want to be fair to it, because it was genuinely professional work: clean charts of crude against its 30-day rolling average, freight indices by trade lane (you know a deck is serious when the freight indices come out), a tidy stack-up of cost categories building to a total impact. And then the proposal: a 12% surcharge on every invoice line item, effective in two weeks, tiered to the 30-day rolling average of a benchmark crude index, with the reassurance that there would be no changes to the price book.

One way to read no changes to the price book is as restraint: we are not repricing you, we are merely surviving the news together. Another way to read it is that a surcharge that never enters the price book never has to leave it, compounds with every gallon of volume growth, and appears in no benchmark anyone will ever compile. The crude tie reads as objectivity, and it is actually an anchor swap: production chemicals are not made of crude oil, but crude is the one index the customer already watches every day and cannot argue with. And the ratchet was asymmetric: up with the index immediately, down on an evaluation schedule, and below the baseline tier the operator does not receive a credit, the surcharge simply rests. Heads, pass-through. Tails, also pass-through.

It is, structurally, a fuel surcharge. The headline is visible. The exposure is not. The number means whatever its author says it means.

Unless you build the thing BA’s passengers never had.

We (Kalibr) have built it. The principle is not exotic: a production chemical is a recipe, and recipes can be costed. Decompose each product family into its feedstock families, weight each feedstock by what the formulation actually contains, price each against a public index, and let only the layer of cost that is actually made of molecules move with the molecule markets. Then perform the one operation the vendor’s deck conspicuously declined to perform, which is multiplication.

Here is the whole trick, with round numbers you can check on a napkin. One feedstock spikes 20%. It is 30% of the raw material basket. Raw materials are half the cost of the finished product. The product impact is 0.20 × 0.30 × 0.50, which is 3%. Not 20%. The deck quoted the 20% and applied it to products as if they were made of nothing but the headline, which is the compositional sleight of hand the entire genre depends on, and it dissolves on contact with three multiplications a junior analyst can do in the margin of the deck itself.

And even the napkin is generous, because it assumes everyone is paying spot. You probably are not, and your supplier almost certainly is not. The large formulators buy their feedstocks the way you wish you bought theirs: forecast far in advance, contracted long, buffered with bulk pre-buys. Innospec, a publicly traded oilfield chemical specialist with the same feedstock exposure, says it plainly in its 10-K:

“We use long-term contracts (generally with fixed or formula-based costs) and advance bulk purchases to help ensure availability and continuity of supply, and to manage the risk of cost increases.”

That is a supplier explaining, in a federal filing, that its input costs are built not to move when the headline does. So when the surcharge letter cites the spot market, the right question is not whether spot spiked. It did; you can read. The right question is how much of the seller’s actual cost basis touches spot at all, and the honest answer is usually: a sliver, with a lag measured in quarters.

I can hear the objection forming. What about force majeure? What if the supplier’s own contracts broke? This is the lovely thing about negotiating with publicly traded counterparties: disclosure is not optional for them. A disruption that materially threatens a supplier’s cost structure or supply chain has to show up in its filings. I will give you the honest calibration, though, because the risk-factor section alone will not settle it (those pages are written by lawyers to be maximally broad, and they warn about everything, always). Read where the numbers live instead. Segment margins. Management’s commentary on cost trends, which must be current. Inventory on the 10-Q, because a supplier sitting on raw materials bought before the spike is delivering you product made at the old cost basis, whatever the cover letter says. An afternoon of financial due diligence parses a force majeure story with reasonable conviction, and a vendor whose own filings show expanding margins and fat pre-bought inventory is telling a story that does not survive its own paperwork.

One more thing, because the worst version of this deserves its own paragraph: the surcharge that arrives mid-term, on a contract with agreed pricing. Allow me a brief soapbox. Term is one of the most valuable things you can give a vendor. It is revenue certainty in a spot-leaning industry, and the market pays handsomely for revenue certainty (listen to any compression company earnings call and count the minutes management spends advertising contract duration to the street). So when you granted term, you were not receiving a discount as a favor. You bought cost certainty and you paid for it with revenue certainty. That was the trade. A surcharge in the middle of it is not a price adjustment; it is a re-trade, and ours, of all industries, should recognize one on sight. We are professional makers of probabilistic, risk-based decisions. We do not drill a well, watch it come in under type curve, and send the service companies a letter requesting a retroactive discount because our risk assessment aged poorly. The vendor’s procurement bet aging poorly is the same event, wearing their jacket. Holding the line on a term contract is not hardball. It is the contract.

Back to our deck. Run that arithmetic across the client’s actual portfolio and the event’s defensible impact came out to roughly 7% weighting product families equally, closer to 6% weighted by spend. Against a flat 12% claim, call it a 2x overstatement on the typical family. And the texture underneath is what made it unanswerable. The crystal-modifier polymers dominating one family’s cost had not moved at all (the claim there was overstated roughly 3x). And one family, hydrate inhibitors, which are essentially bulk methanol in a branded tote, justified *more* than the surcharge asked for, because the disruption had taken a real slice of global methanol capacity offline. We led with that one. When your model occasionally argues for the other side, people start believing your model. (This is also a reasonable test of a consultant, but that is a different newsletter.)

This is the regime change, and the game theory language is worth the thirty seconds because it tells you the model is not a tactic. Crawford and Sobel proved you cannot fix cheap talk by listening harder. A parallel literature (Grossman and Milgrom, 1981) proved what happens when claims become provable: the equilibrium flips. Exaggeration becomes detectable, detection becomes expensive for the exaggerator, and silence itself becomes informative, because a vendor with a genuine cost case will sprint to show you receipts. A should-cost model does not improve your position in the old game. It deletes the old game and replaces it with one where “our costs went up” stops being a price and starts being a hypothesis.

The minimum viable version, for anyone who owns chemical LOE, is honestly not much: a one-page decomposition of your top product families against four or five public indices, refreshed quarterly. The full version is contracts indexed to feedstocks at margins both sides accept with symmetric movement, and an auto-RFP that quietly re-shops your program when the indices fall and your contract does not. (A vendor who objects to symmetric indexing is telling you, with admirable economy, what the last surcharge was for.) That is the layer Kalibr built under compression, now running under chemical spend. The verification technology, permanently on.

Chemicals is not special. It is simply the category I was standing in when the deck arrived, and, if anything, the easy one. It is the only line we track that is a pure commodity, which is why it decomposes as cleanly as it just did. A chemical is a recipe; there are no performance trends riding on top of the molecules, no KPI story to pull out of the price. The others are harder. Frac, OCTG, and compression each carry a service-and-performance layer, a supply-and-demand layer that moves price independent of cost, and a financial decoupling you have to run before “should-cost” means anything at all. We build that for each of them, because the discipline does not change even when the anatomy does: separate the part of the price that is a real, indexable commodity from the part that is a story, tie the first to a public number, hold the second to ordinary inflation, and write symmetric movement into the contract. The surcharge genre is not a chemical phenomenon. It is what happens to any line item with a motivated seller and a buyer who cannot check the math, which is to say most of them. The headline changes. The arithmetic does not.

The chemical version of it is a report. Every quarter, a should-cost decomposition of the major product families against the public indices they ride: the model in this piece, kept current, waiting in a drawer for the morning a deck lands on your desk. For anyone who wants it live instead of quarterly, the same model sits on a platform wired straight to the feeds.

Paid subscribers get the quarterly report starting in Q3 2026. the live platform is for people who hate waiting.

What the Model Knows (and What I Won’t Tell You)

I am now going to be coy about the model’s internals, and the coyness is load-bearing. Part of what the model is worth is that the vendor knows we can see the cost structure without knowing exactly how finely we can see it. Ambiguity is usually the seller’s asset. This is the rare place it works for you.

What I will tell you is the shape. Every product family reduces to a handful of feedstock families: methanol, ethylene derivatives, aromatic solvents, fatty acids, phosphoric acid, glycols. Corrosion inhibitors lean on fatty acids and aromatics. Demulsifiers are ethylene oxide chemistry. Hydrate inhibitors are methanol wearing a jacket. Each family maps to an index you can pull without anyone’s permission: Methanex posts its North American methanol price monthly, CME lists ethylene futures, Platts assesses the aromatics, and crude is a workable proxy for the petroleum-derived solvents. Above the molecules sit four more layers (blending, logistics, SG&A, margin), and the entire model rests on one observation: a headline touches the first layer and merely waves at the others, which move with ordinary inflation no matter what the news is doing.

The 50/50 fact makes it sharper. Half a chemical contract is not chemistry at all; it is service and knowledge, the tech and the lab. A commodity shock touches, at most, the raw-material slice of the chemistry half. A flat surcharge on the whole invoice therefore repriced the field techs’ time because a commodity index moved, which is a sentence nobody would say out loud, which is why it was a percentage on an invoice instead of a sentence.

Vendor: our costs went up.

You: which of them?

Vendor: ...costs.

That exchange, with a model behind it, is most of the job.

What I will not tell you: the weights, the per-family formulas, the full input lists. But you do not have to take the decomposition on my authority. The same Innospec 10-K that told you how the suppliers buy also tells you what they buy: oleochemicals, ethylene, solvents, amines, alcohols, polyacrylamides. The same families. The suppliers already index their inputs. The surcharge proposes that you, alone in the entire chain, pay spot. Someone has to, I suppose.

The Alternative Market That Isn’t

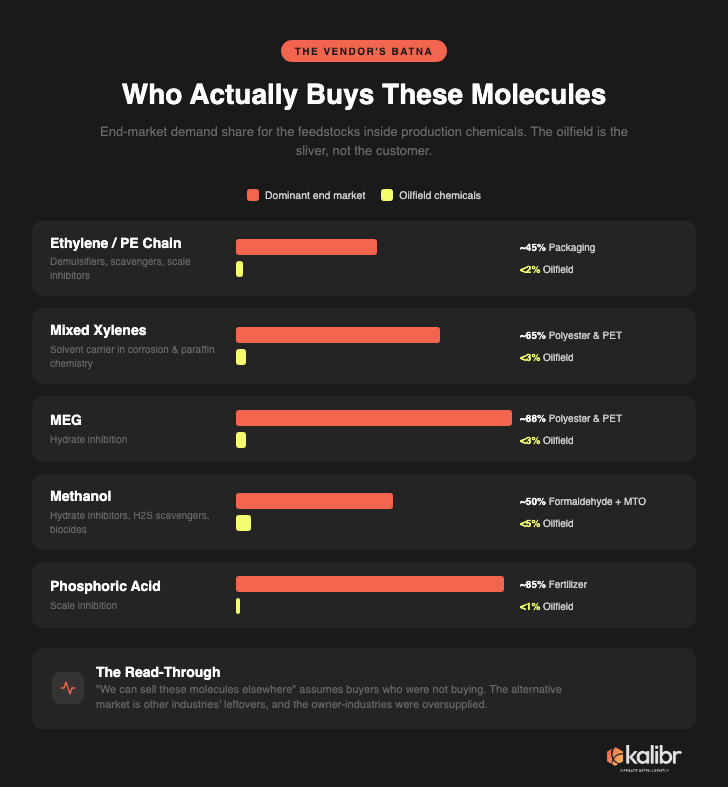

There is a quieter claim inside every surcharge conversation, usually unspoken, occasionally said out loud when things get tense: we have other places to sell this. That is the vendor’s BATNA, and it deserved a look, so we looked.

The look was unkind. The feedstocks in production chemicals are not oilfield molecules; they are everyone else’s molecules that the oilfield borrows. Packaging consumes roughly 45% of the world’s polyethylene; oilfield demand does not register in ethylene end-use breakdowns. Polyester and PET own about 65% of xylene chemistry and nearly 90% of MEG. Methanol belongs to formaldehyde, construction resins, and Chinese methanol-to-olefins plants. Phosphoric acid is 85% fertilizer. You are not the customer in these markets. You are barely a rounding adjustment on the customer. And the actual owners were, at the moment of the surcharge, mostly not buying: global ethylene operating rates are headed toward 79% against a historical 88%, after the industry added 40 million tonnes of capacity from 2020 to 2025 against 27 million tonnes of demand, and Chinese MTO units were running at 60% utilization. The spikes in the vendor’s deck were supply-shock premiums on structurally oversupplied markets. That is the kind of price that corrects, and the kind of alternative demand that is not standing in line for anyone’s diverted totes.

Two honest exceptions, because the model gets to be honest or it gets to be useless. Phosphoric acid is genuinely tight, and tightening for reasons that have nothing to do with any headline: LFP batteries are pulling purified phosphoric acid toward automakers, who may be 24% of demand by 2030. Tall oil fatty acids are structurally tightening because renewable diesel mandates outbid everyone for the feedstock. Both are real. Both predate the conflict. Both belong in contract repricing at renewal, not in an emergency surcharge wearing the headline’s jacket.

You Can’t Negate Alone

The model won the argument. The model could not end the negotiation, because arguments are not the thing negotiations are made of. There was a person on the other side of the table who now had a problem: he had sent a corporate deck demanding 12%, the customer had just proven 7%, and somewhere above him sat a spreadsheet with his name on it and a surcharge-revenue column that was no longer going to fill itself. If you make his refusal humiliating, you win a quarter and poison a decade. This is a repeated game. Same vendors, same basins, same kids’ soccer sidelines, for the next twenty years.

So you give. Not on price. On things that are cheap to you and look like trophies to him. Term is the classic: a contract extension at current pricing converts your price integrity into his retention story, and retention is what his corporate actually tracks. (The extension costs you nothing if you were staying anyway, and, be honest, you were.) The other is a trial of a higher-strategic product line: pilot the technology he is under pressure to commercialize, at cost, in exchange for the performance data and the reference rights his sales deck is starving for. The field team books a win it can report upward that is worth more internally than the surcharge ever was.

And the choice itself is a diagnostic, which is the mechanism design part, and my favorite part. A vendor in a genuine cost emergency takes cash in any form cash arrives. A vendor that cheerfully trades a 12% surcharge for a contract extension and a case study has told you, in the language of revealed preference, what the surcharge actually was. It was margin expansion with a headline on the cover page. You did not extract that confession. You designed a menu, and he ordered it.

Stepping Over Nickels

There is one more move, and it is the one that closed ours: stop arguing about the size of the nickel and show them the dollar they are stepping over.

Run the materiality math from the vendor’s side. A 12% surcharge on a mid-market chemical program is a couple hundred thousand dollars a year. Against the revenue base of a major service company, that is not a number. It is roughly what the company distributes to its shareholders in the time it takes to schedule the meeting about the surcharge. And the operator on the other side of the table is the growth story. Field people already have an idiom for this exact error, pointed the other direction: one executive described cutting frac chemistry to save a few thousand dollars a day, against a completion burning hundreds of thousands a day, as tripping over dollars to pick up pennies. Turn the idiom around and hand it back across the table. In this negotiation, the vendor is the one stepping over dollars.

What the dollar looks like depends on the operator, and every operator has a version of this story; most never think to tell it. I will not walk through every situation here (mapping yours precisely is what the custom market intelligence reports are for), but a few general ones illustrate the point.

The non-Permian oil operator with deep inventory. While the Permian fights Tier 1 exhaustion and consolidation eats the customer list one acquisition at a time, an operator with decades of undrilled locations in an unconsolidated basin, adding rigs while the public companies hold maintenance-mode flat, is one of the only organic growth stories left in the vendor’s North American book. (The major suppliers need North American growth stories right now considerably more than they need surcharge revenue.) The supplier embedded there today rides the basin’s growth without ever re-competing for it.

The vertically integrated gas producer. Owns its molecules from wellhead toward market, which makes its revenue, and therefore its chemical program, annuity-grade. In a business where production chemicals are prized precisely because they are insulated from rig-count cycles, the steadiest book of business in the building is not the account you reprice with a rider. It is the account you protect from your own corporate.

The ABS-backed operator. Securitized PDP, hedged production, a strict cash waterfall in which LOE sits senior to the noteholders. Chemical cost stability there is not a preference; it is approximately a covenant. And every new financing the operator closes is acreage and production the embedded vendor inherits without a single sales call. A surcharge dispute is a strange way to treat a customer whose corporate structure legally obligates it to be boring and pay you forever.

In each case the message to the supplier is the same, and it is not a threat. It is an invitation to do arithmetic: you can have the surcharge, or you can have the option on everything we are about to become. The vendor that prices the relationship like a line item gets treated like one.

Ours did the arithmetic. The surcharge went to zero. The vendor left with a package of things worth considerably more to it than the surcharge ever was, and everyone reported a win, which is the defining feature of a deal that was never really about costs.

And, as I said at the top, “ours” is not singular. The sequence keeps ending at zero because none of it is magic. It is a model, a market report, and a negotiation sequence, applied before the surcharge’s effective date instead of grieved after it.

British Airways’ customers eventually got their verification technology. It was called the Office of Fair Trading. It required a whistleblower to switch it on, and it arrived four years and $550 million late, refunding one third of the surcharge to people who had long since flown home.

You do not need a regulator. You do not need a whistleblower. You need the model before the deck arrives, because the deck is already written; it is sitting in a drafts folder waiting for the next headline (a tariff schedule, a strait, a storm, a strike), and there will always be a next headline. Cheap talk drifts toward whatever the story will bear. Verifiable claims do not drift. They reconcile.

Talk is cheap. Make them prove it.